The Extraction Machine: How American Healthcare Converts Patient Dollars to Corporate Profit

Executive Summary

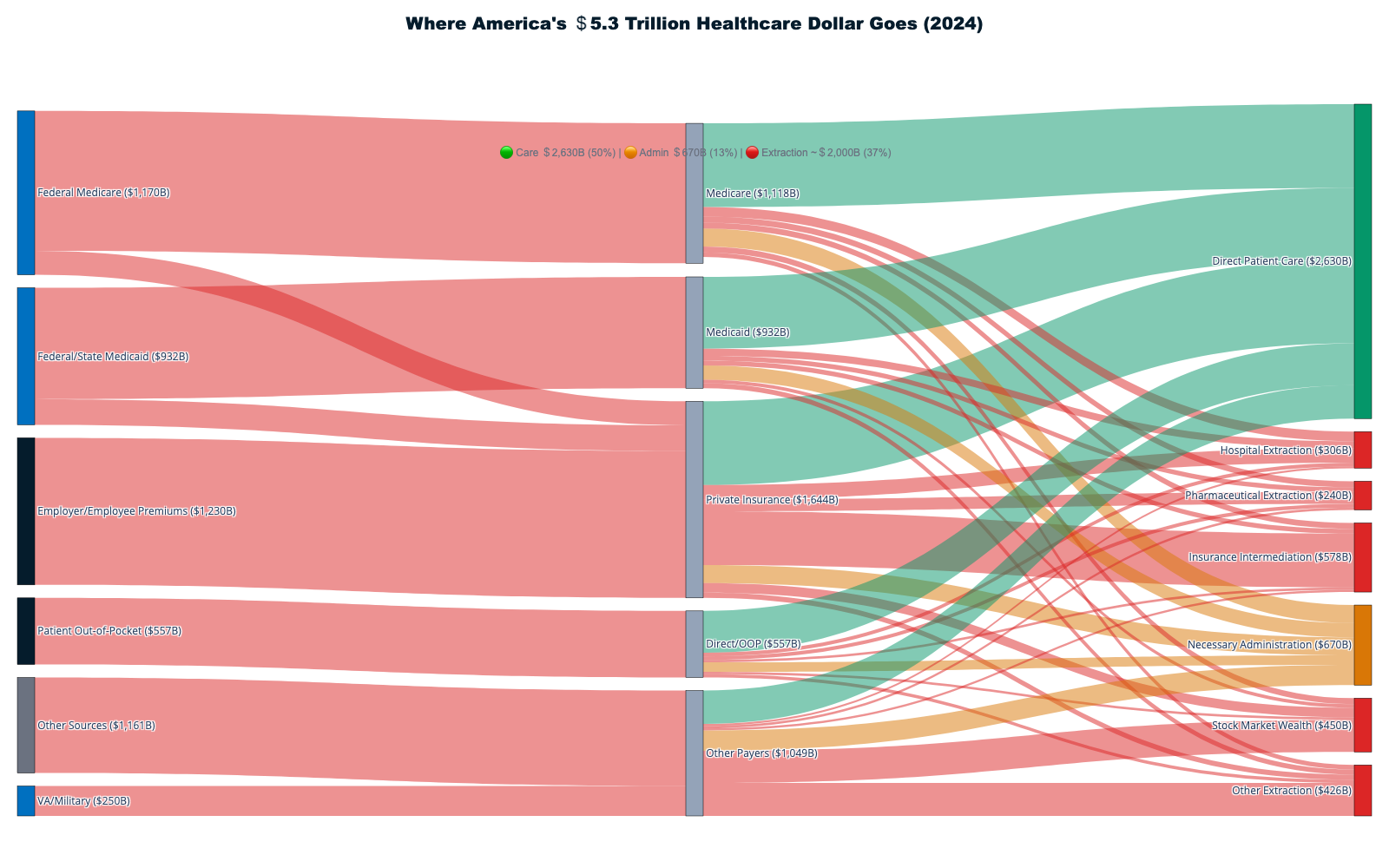

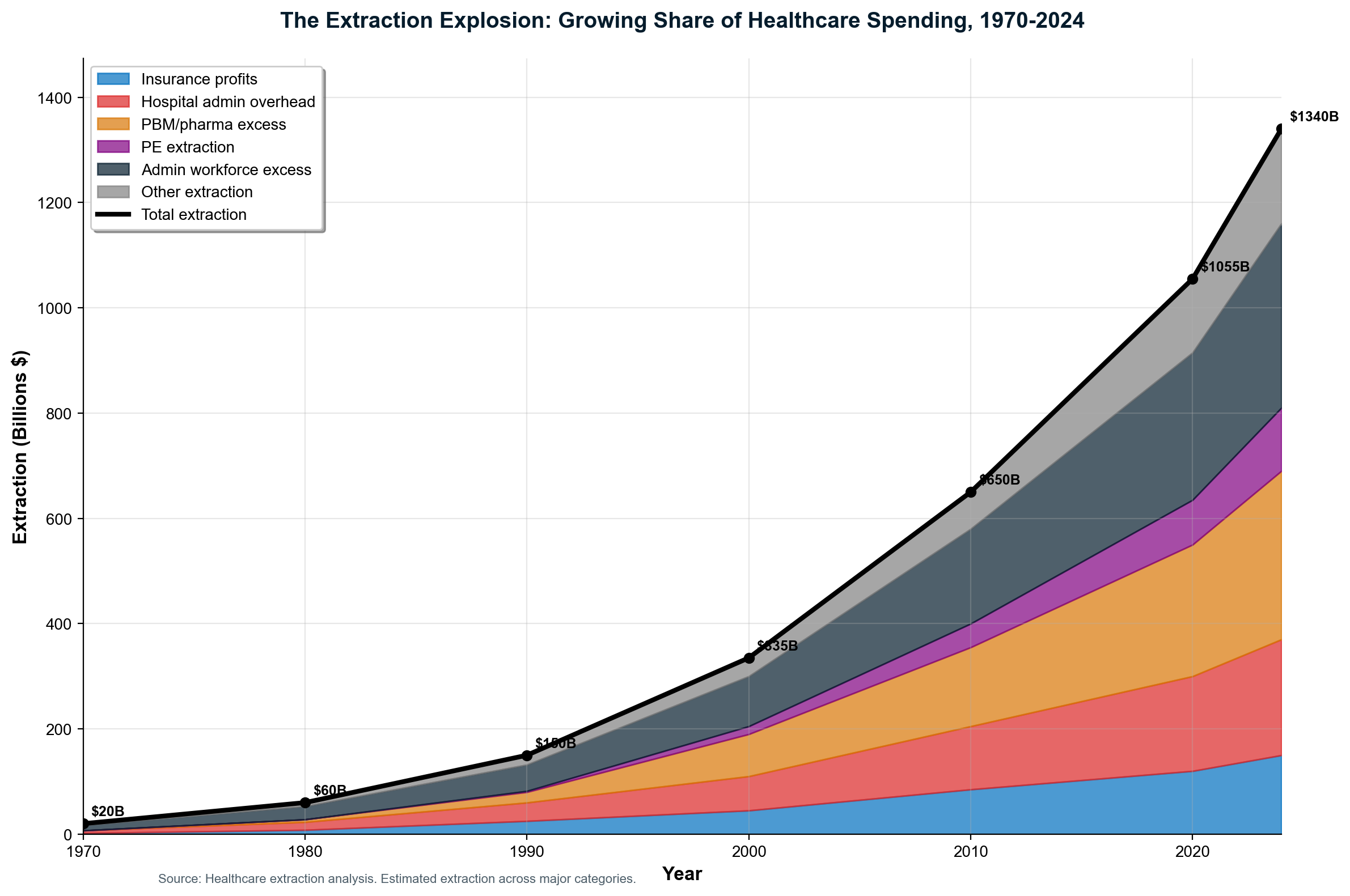

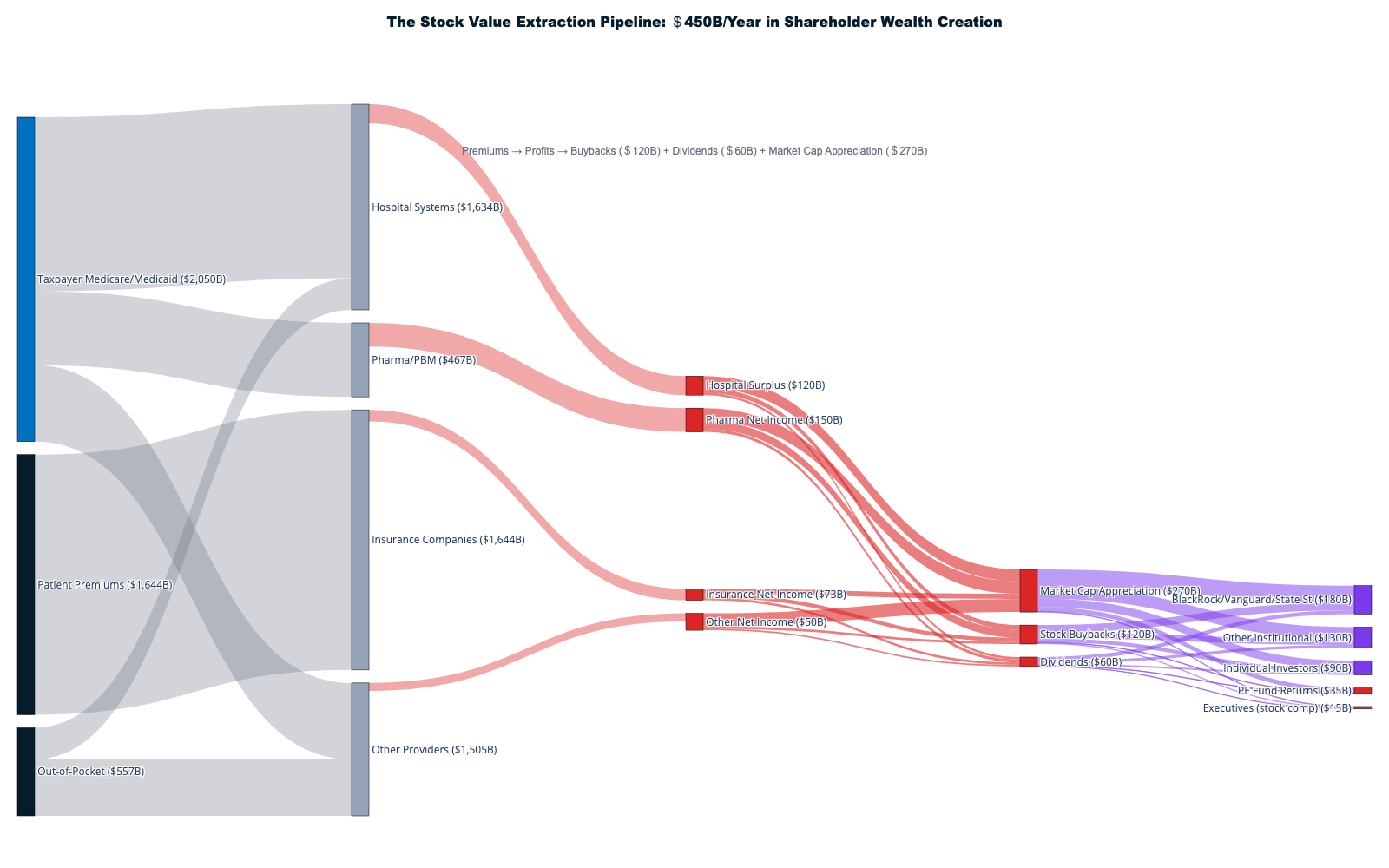

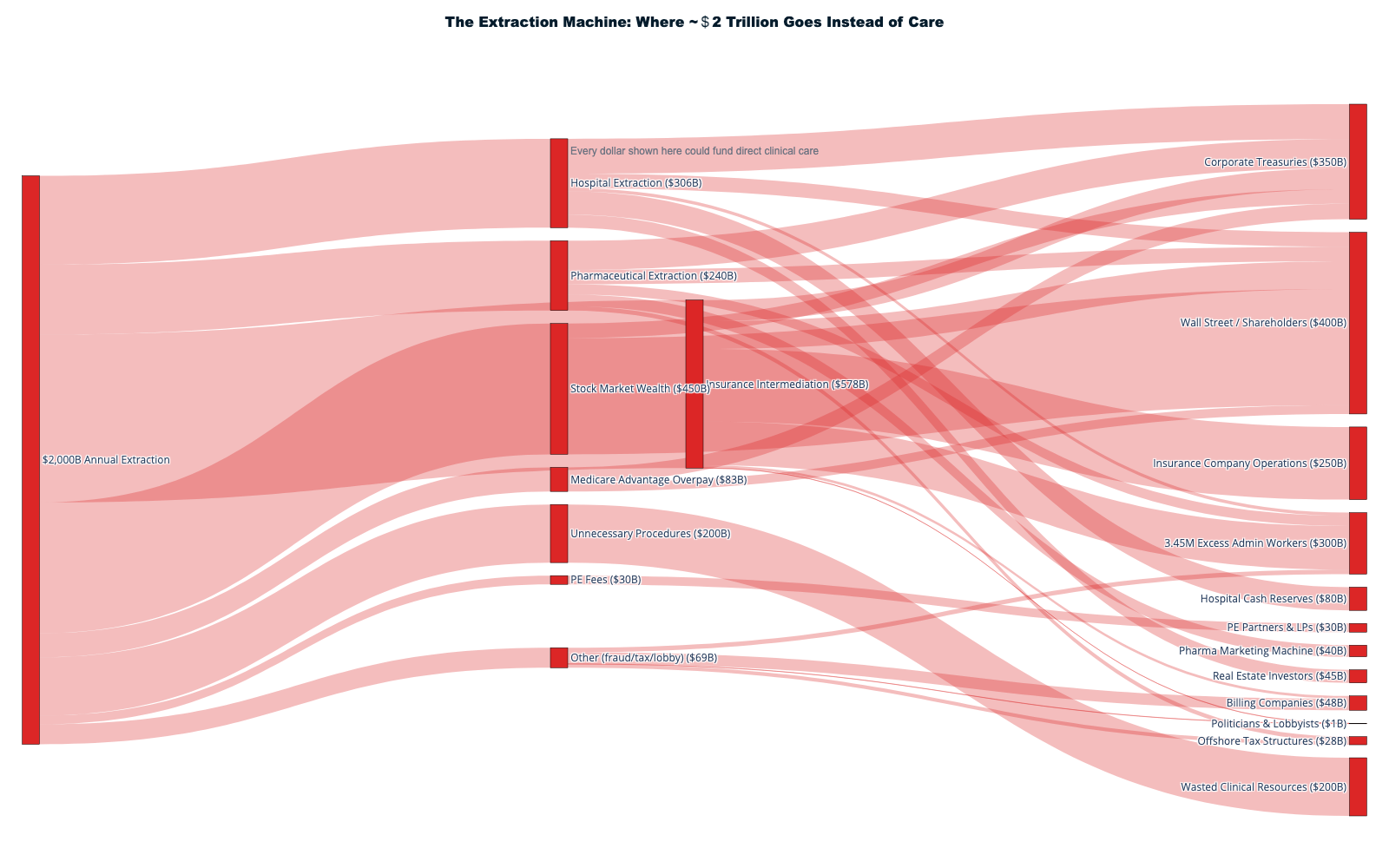

This report documents how $1.8+ trillion in cash is extracted annually from America's $5.3T healthcare system through financial engineering, administrative complexity, and corporate consolidation — with an additional $270B in stock market wealth creation amplifying extraction into permanent shareholder value. Only 42¢ of each healthcare dollar reaches direct patient care. The remaining 58¢ flows to insurance intermediation ($578B), shareholder cash returns ($180B), pharmaceutical manipulation ($240B), administrative overhead, and other extraction layers that add no clinical value.

Building on Volume I's statistical model of healthcare economic extraction, this volume follows the money — naming names, tracing cash flows, and exposing the specific mechanisms through which extraction operates. Together, the two volumes provide the most comprehensive forensic investigation of American healthcare finance ever assembled.

Including 19 Interactive Sankey Diagrams

Introduction: The Architecture of Extraction

Volume I of this investigation established the statistical framework quantifying healthcare extraction across the American economy, revealing systematic correlations between insurance company revenue optimization and declining health outcomes. This volume turns from the 'what' to the 'how' — a forensic investigation tracing every dollar through the extraction machine, from the premium payment to the stock buyback.

In 2024, Americans spent $5.3 trillion on healthcare—$15,474 for every man, woman, and child—yet the most shocking revelation is not how much we spend, but where those dollars actually go before any medical care reaches patients. [1] Every healthcare dollar passes through a sophisticated extraction machine that systematically diverts funds from patient care to corporate profit centers, creating the largest wealth transfer operation in the American economy.

Understanding Hospital Extraction ($306B): For-Profit and Nonprofit Alike

The hospital extraction figure encompasses both for-profit hospital systems and the substantial financial surpluses generated by nominally "nonprofit" institutions. The $306B breaks down as follows:

- For-profit hospital net income: $85B — HCA Healthcare alone generated $5.8B in net income (2024) on $70.6B revenue, with $10B earmarked for stock buybacks. [22]

- Nonprofit hospital "operating surplus": $65B — functionally identical to profit. Mayo Clinic reported $16.3B revenue with a $2.3B operating margin [123]; Cleveland Clinic generated comparable surpluses. These billions fund executive compensation ($5-15M CEO salaries), cash reserves exceeding $100B system-wide, and expansion — functionally indistinguishable from for-profit extraction.

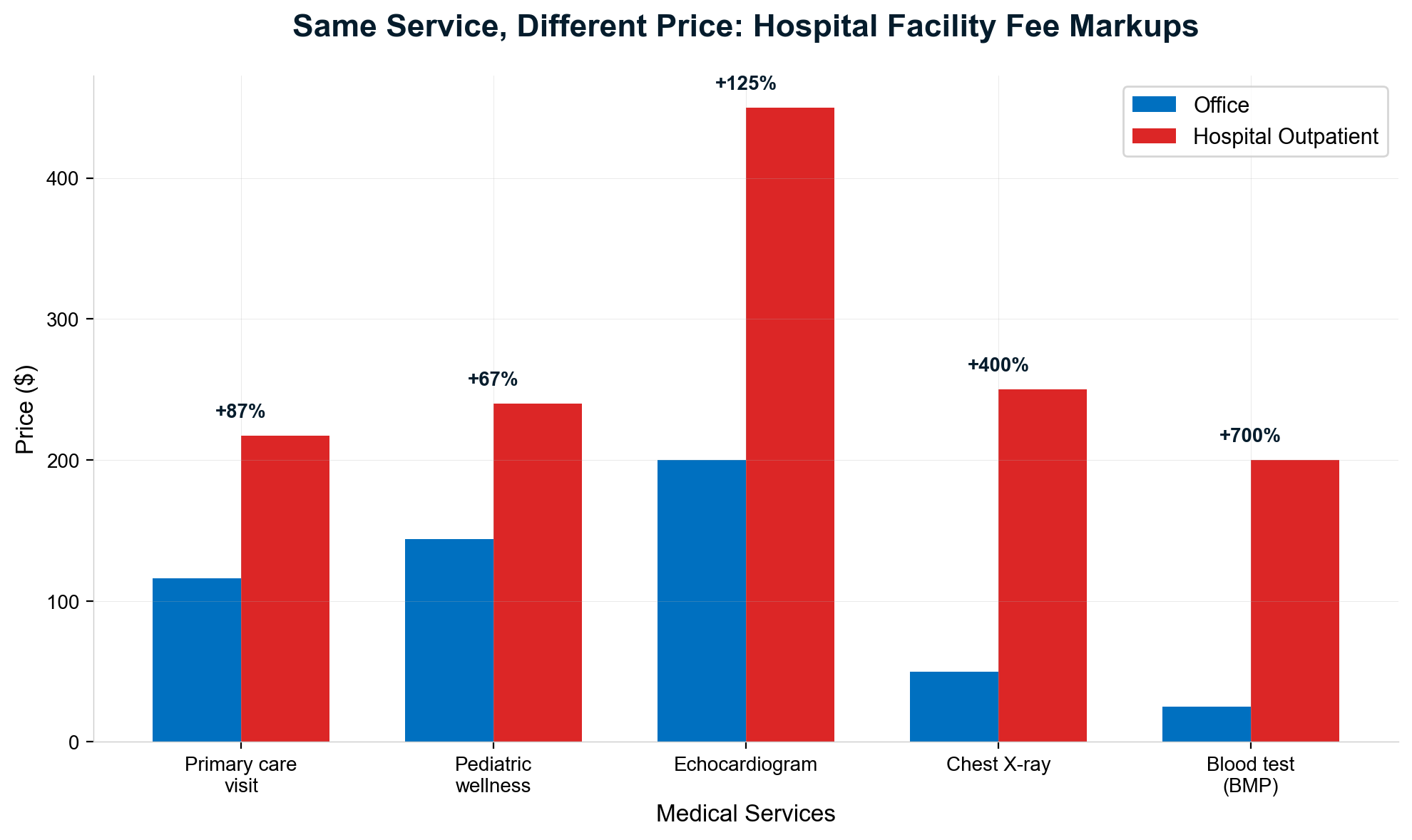

- Facility fee arbitrage: $95B — hospitals charge 87% more for identical services performed in hospital outpatient departments versus independent physician offices, exploiting Medicare's site-of-service payment differential. A $150 office visit becomes a $280 hospital outpatient encounter for the same physician performing the same procedure. [24]

- Hospital-driven supply chain markups: $61B — group purchasing organizations (GPOs) and hospital supply chains add layers of intermediation that inflate device and supply costs while generating administrative fees and kickbacks.

The distinction between for-profit and nonprofit hospitals has become largely semantic: nonprofit hospital CEOs routinely earn $5-15 million annually [18], and the ratio of nonprofit hospital CEO compensation to median worker wages has widened from 7:1 (1990) to over 20:1 today. Nonprofit hospital systems generate billions in "operating margin" that funds executive compensation packages rivaling Wall Street, cash reserves larger than most countries' healthcare budgets, and empire-building acquisitions — all while claiming tax exemptions worth an estimated $28B annually in exchange for "community benefit" that often consists primarily of bad debt reclassified as charity care.

Who Captures the $270B in Annual Market Cap Appreciation?

The $270B non-cash wealth effect breaks down by sector: health insurance companies (~$95B, with UnitedHealth alone appreciating from $39B to $265B market cap), pharmaceutical companies (~$85B), hospital systems (~$35B), medical devices and health IT (~$30B), and PBMs/pharmacy chains (~$25B). These gains are concentrated: the top three institutional investors (Vanguard, BlackRock, State Street) collectively own approximately 20% of every major healthcare company [17], creating common ownership patterns that academic research has linked to reduced competitive incentives.

Who are the concrete recipients? Based on SEC 13F filings for UnitedHealth Group (86% institutional ownership), CVS Health (84% institutional), and HCA Healthcare (91% institutional), the $270B in annual market cap appreciation flows approximately as follows:

- ~25-30% to the "Big Three" index fund managers (Vanguard ~9%, BlackRock ~8%, State Street ~4% of major healthcare stocks) — passive investors who hold shares indefinitely, compounding the wealth effect across market cycles

- ~20% to pension and retirement funds — public employee pensions (CalPERS, New York State), 401(k) plans, and sovereign wealth funds. These represent the only pathway through which ordinary Americans indirectly benefit from healthcare extraction

- ~15% to hedge funds and active managers — firms like Capital Group, Fidelity, and Wellington that trade on extraction optimization signals

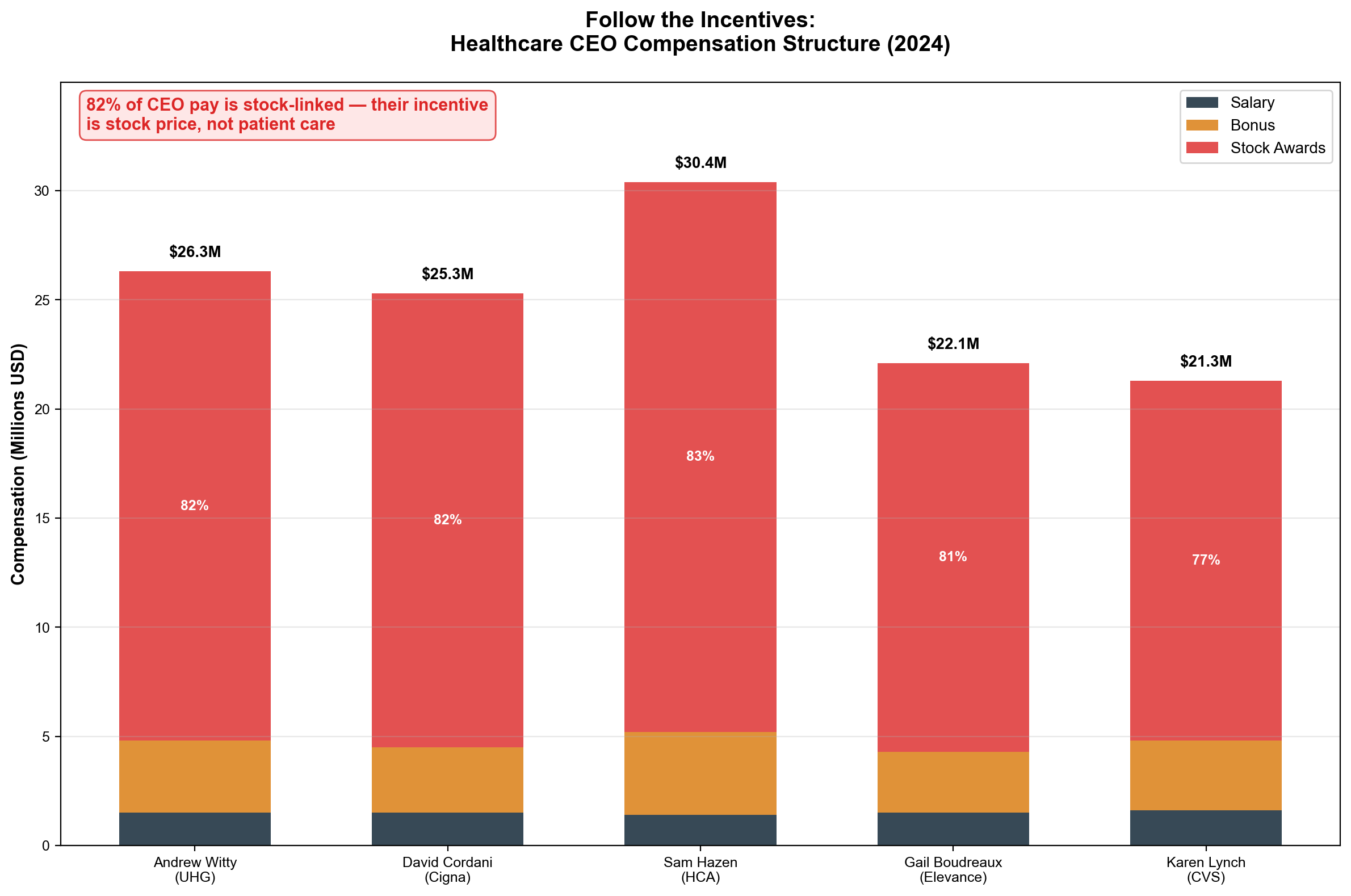

- ~10-15% to corporate insiders and executives — through stock-based compensation, option exercises, and insider sales. UnitedHealth CEO Andrew Witty's 2024 compensation was 82% stock-based ($21.5M in equity awards)

- ~20-25% to retail and individual shareholders — direct stock ownership, self-directed IRA accounts, and brokerage portfolios

The concentration of ownership means healthcare extraction wealth accrues primarily to the already-wealthy: the top 10% of American households own 93% of stocks. For the median American family paying $25,000 annually in healthcare costs, the stock market wealth their premiums generate flows overwhelmingly to institutional investors and corporate executives — not back to patients.

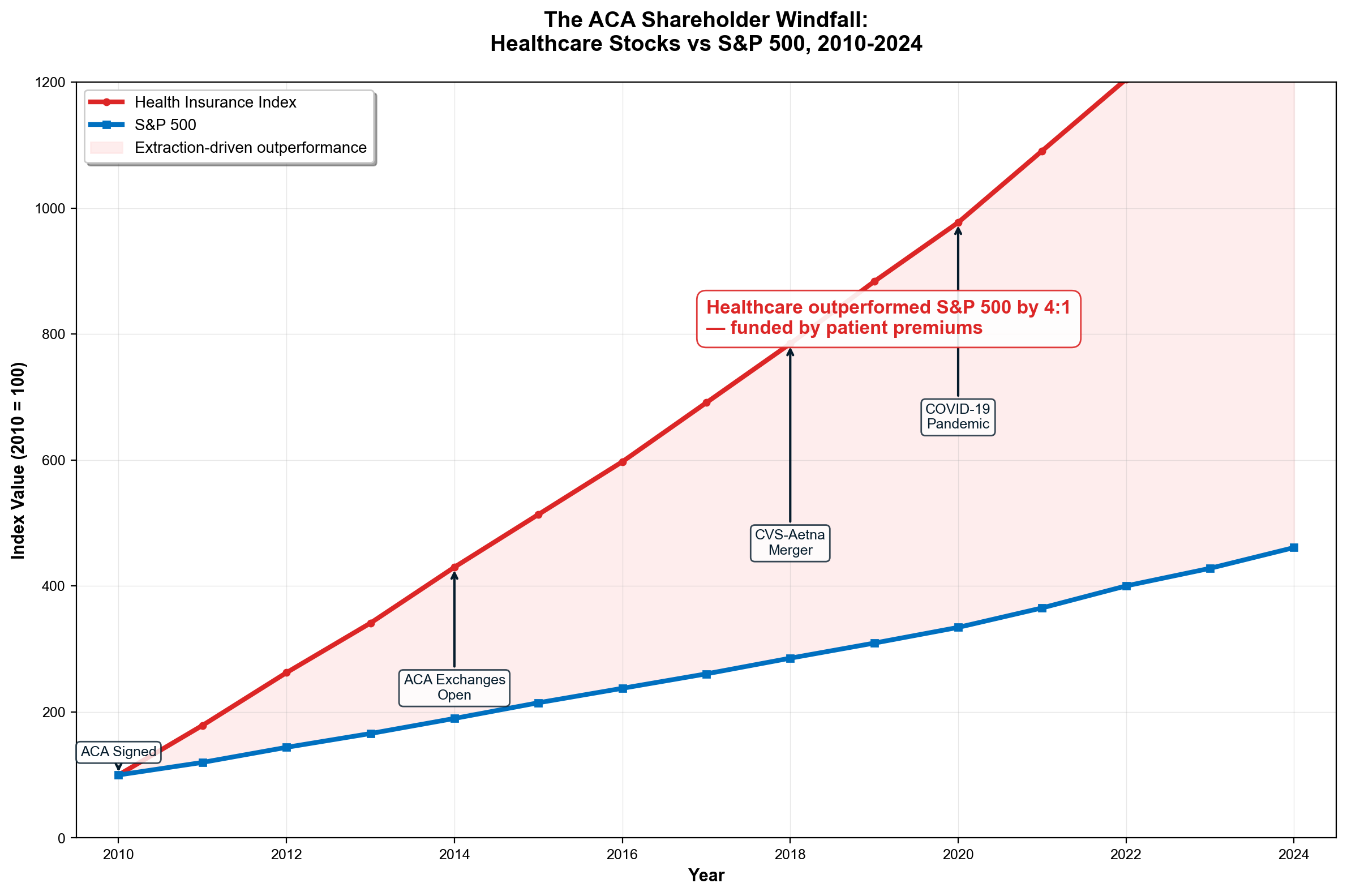

The single most devastating finding: stock market wealth creation from healthcare extraction now reaches $300-600 billion annually—10 to 30 times larger than reported industry profits. UnitedHealth Group's market capitalization expanded from $39 billion in 2010 to $265 billion in 2026, representing $226 billion in shareholder wealth creation funded entirely by patient premiums and taxpayer subsidies. [2] Health insurer stocks increased 1,032% from ACA enactment through 2024, compared to 251% S&P 500 growth—a 4:1 outperformance that proves extraction as successful investment thesis rather than healthcare delivery. [3]

Total Healthcare Extraction: $1.8-2.4 trillion annually (34-45% of all spending) flows to financial engineering rather than patient care

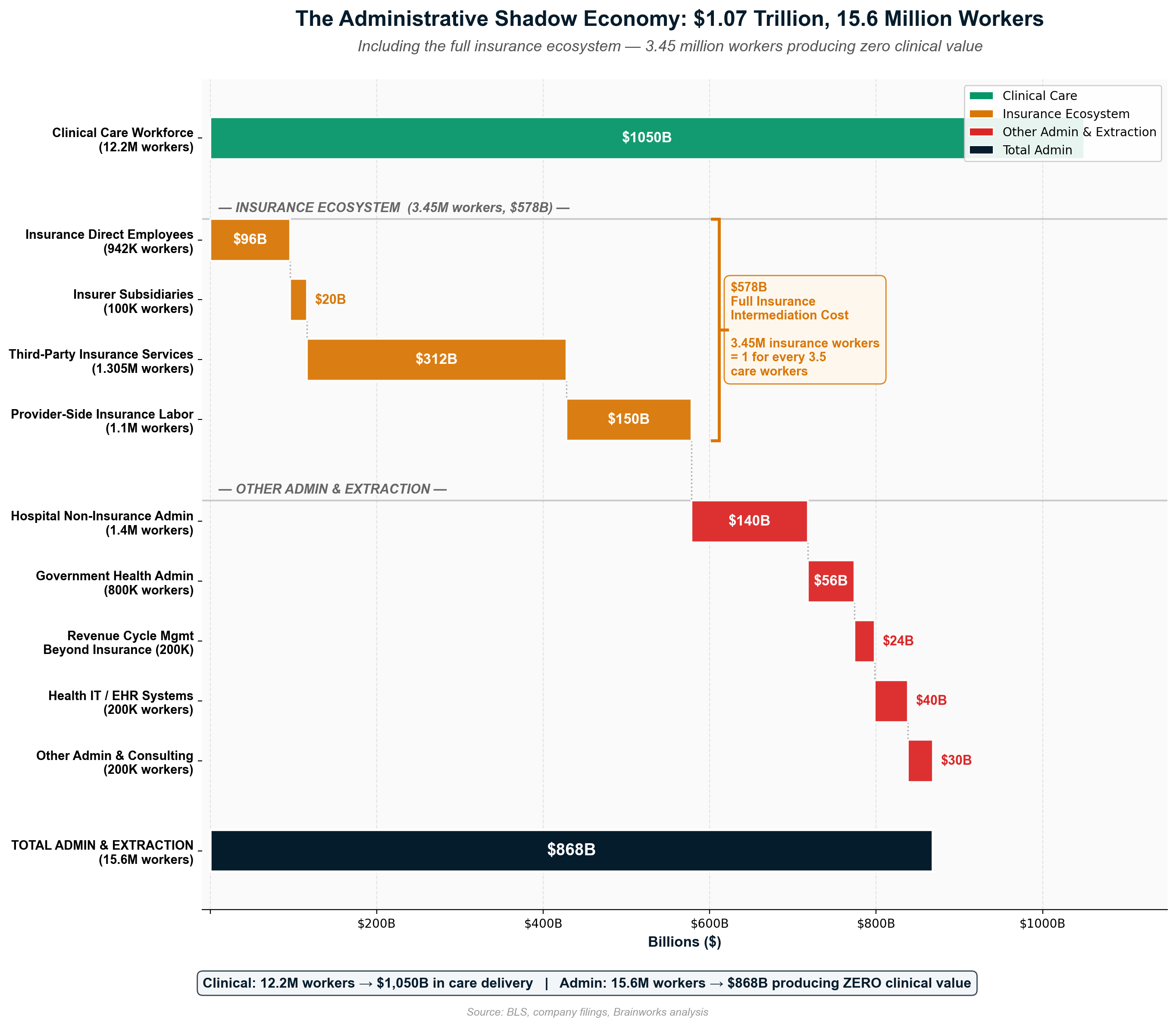

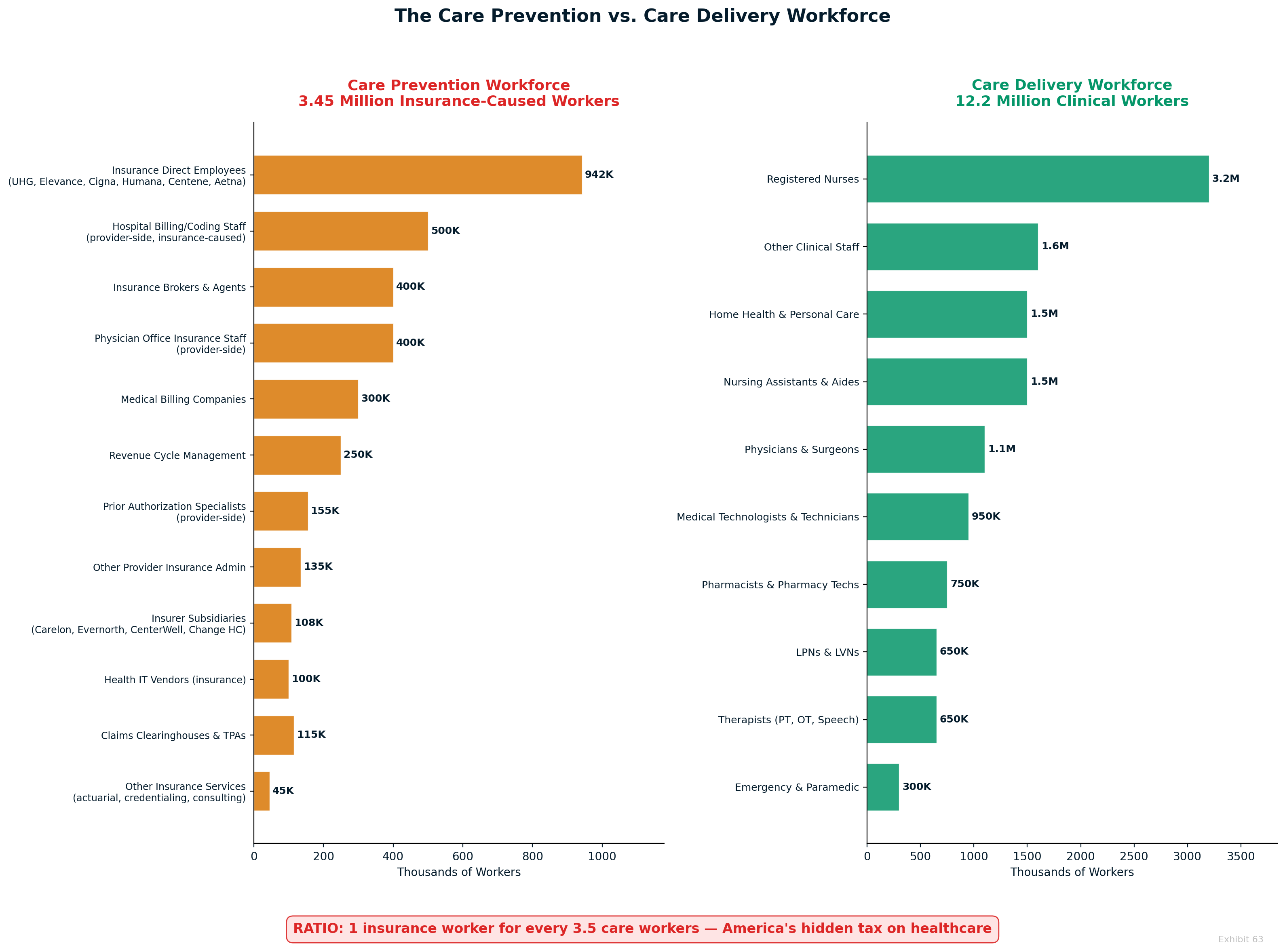

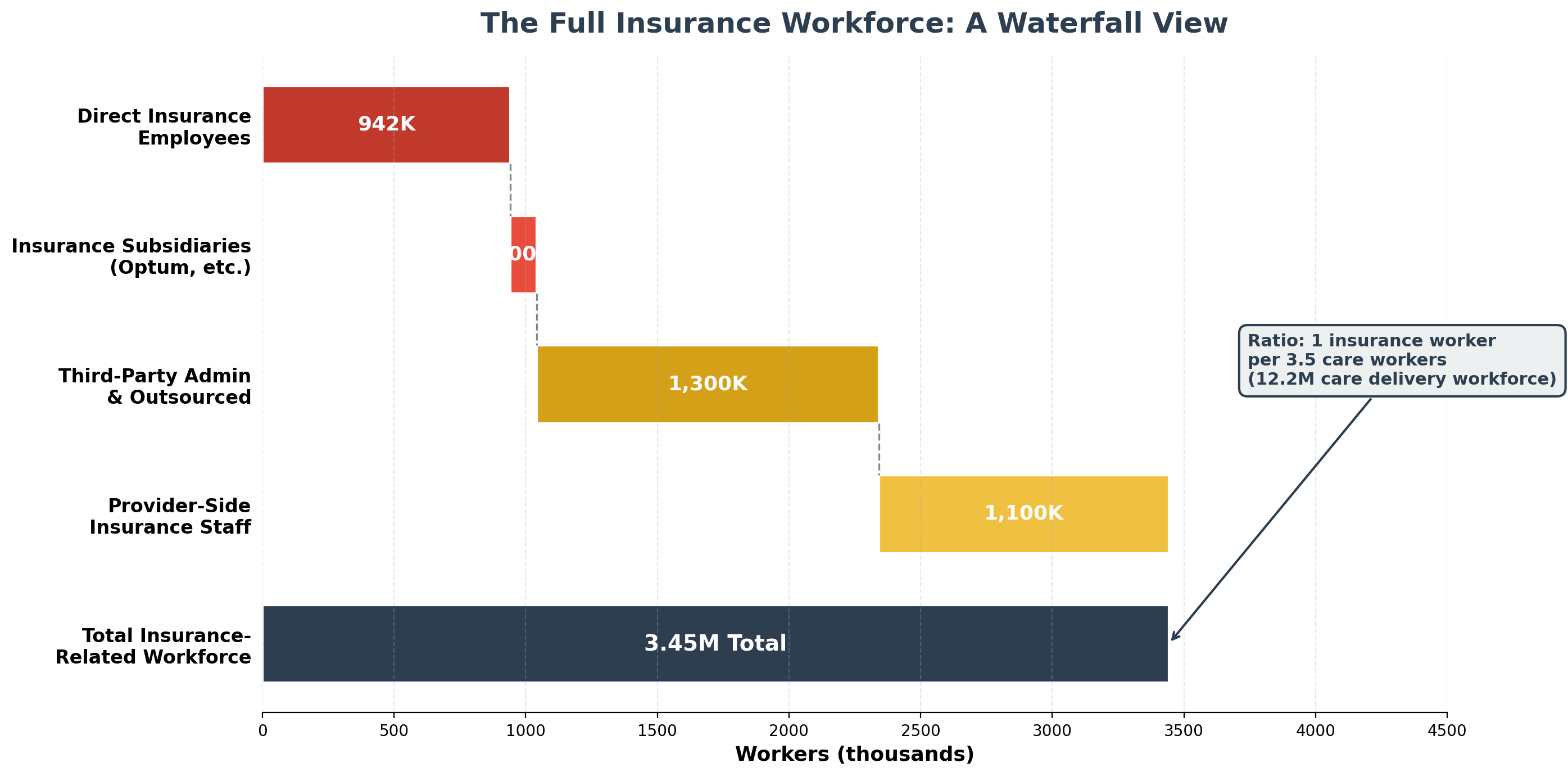

The administrative shadow economy employs 12-15 million workers consuming over $1 trillion annually in wages to navigate complexity that exists purely for extraction purposes. [4] This artificial economy includes 3.45 million insurance-caused workers who provide zero clinical care — not just the 941,880 direct insurance employees, but also 100,000 in insurer subsidiaries, 1.3 million in third-party insurance service companies (billing, RCM, brokers, IT vendors), and 1.1 million provider-side staff hired solely to deal with insurance requirements. That's 1 insurance worker for every 3.5 care workers. The United States employs ten administrators per physician compared to one-to-one ratios in single-payer systems—a differential representing $186+ billion in annual administrative waste exceeding the total administrative costs of all peer countries combined. [5]

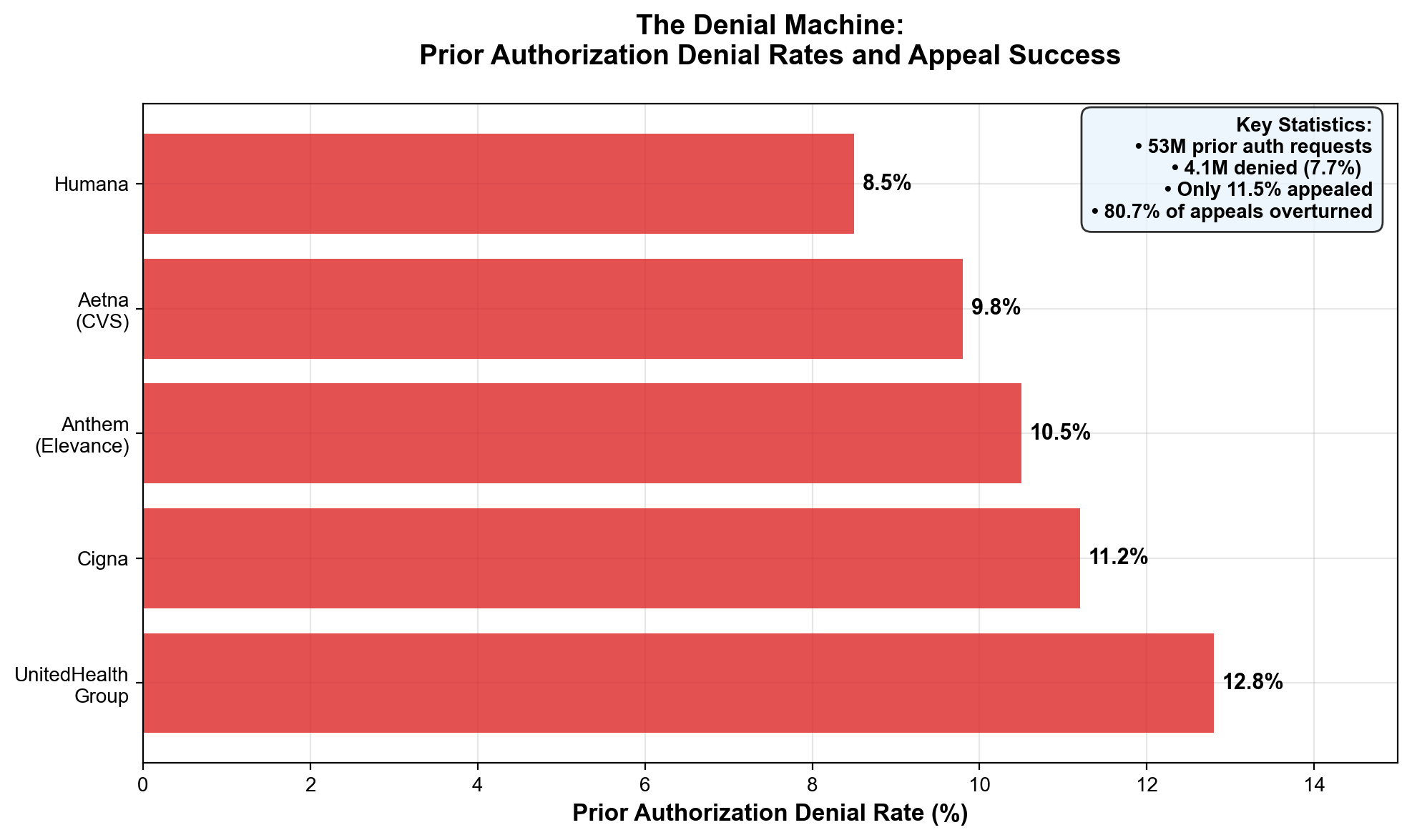

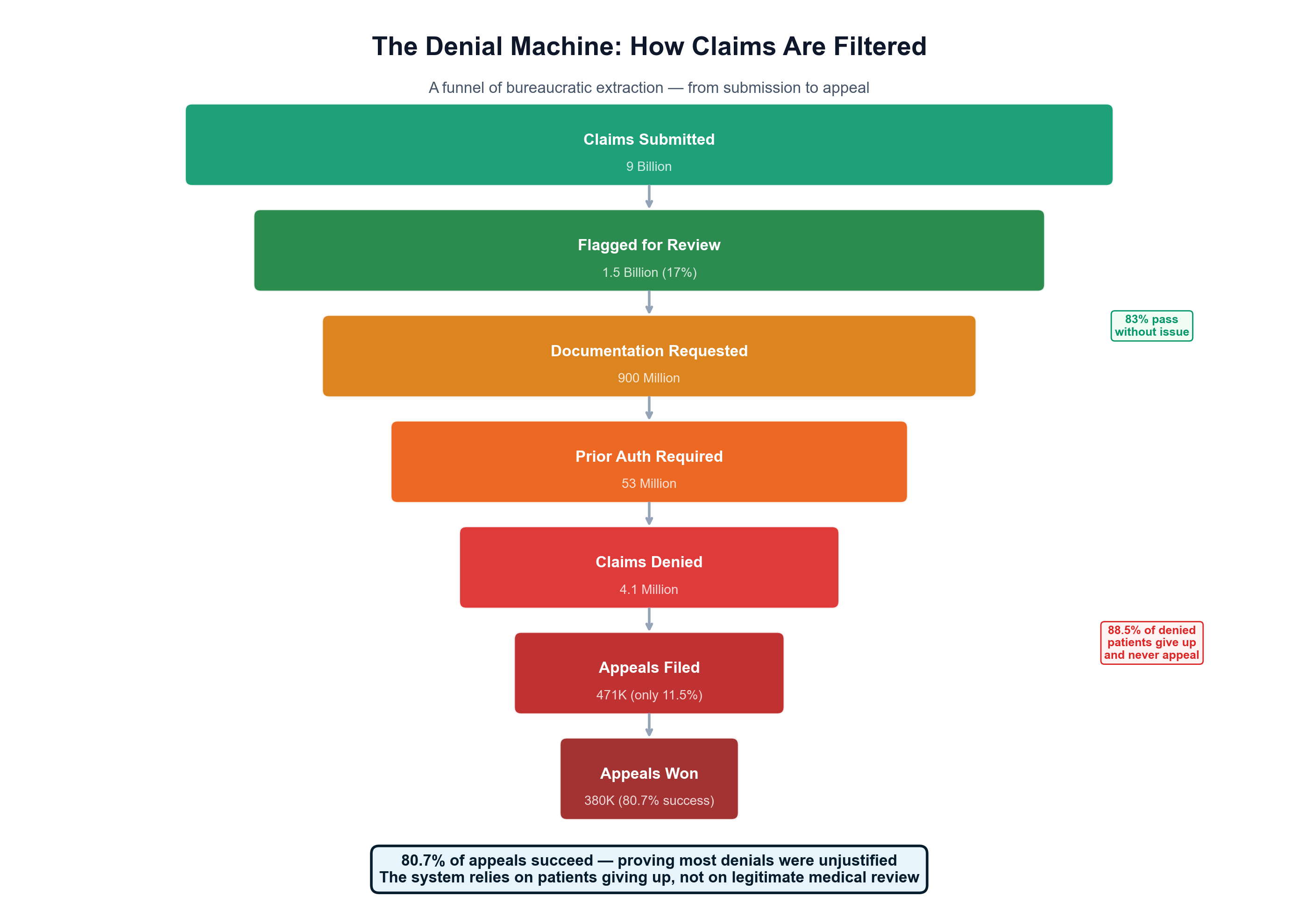

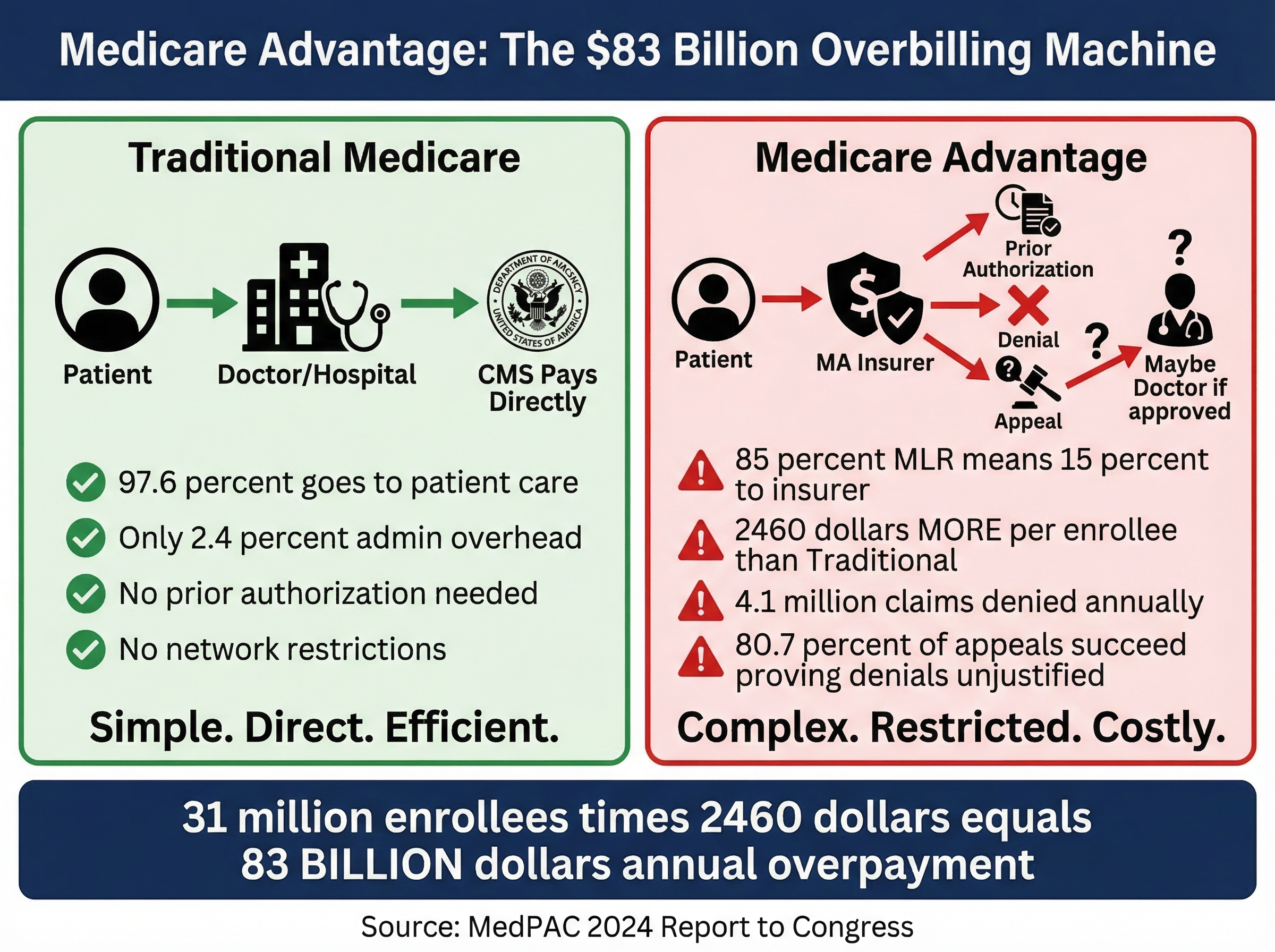

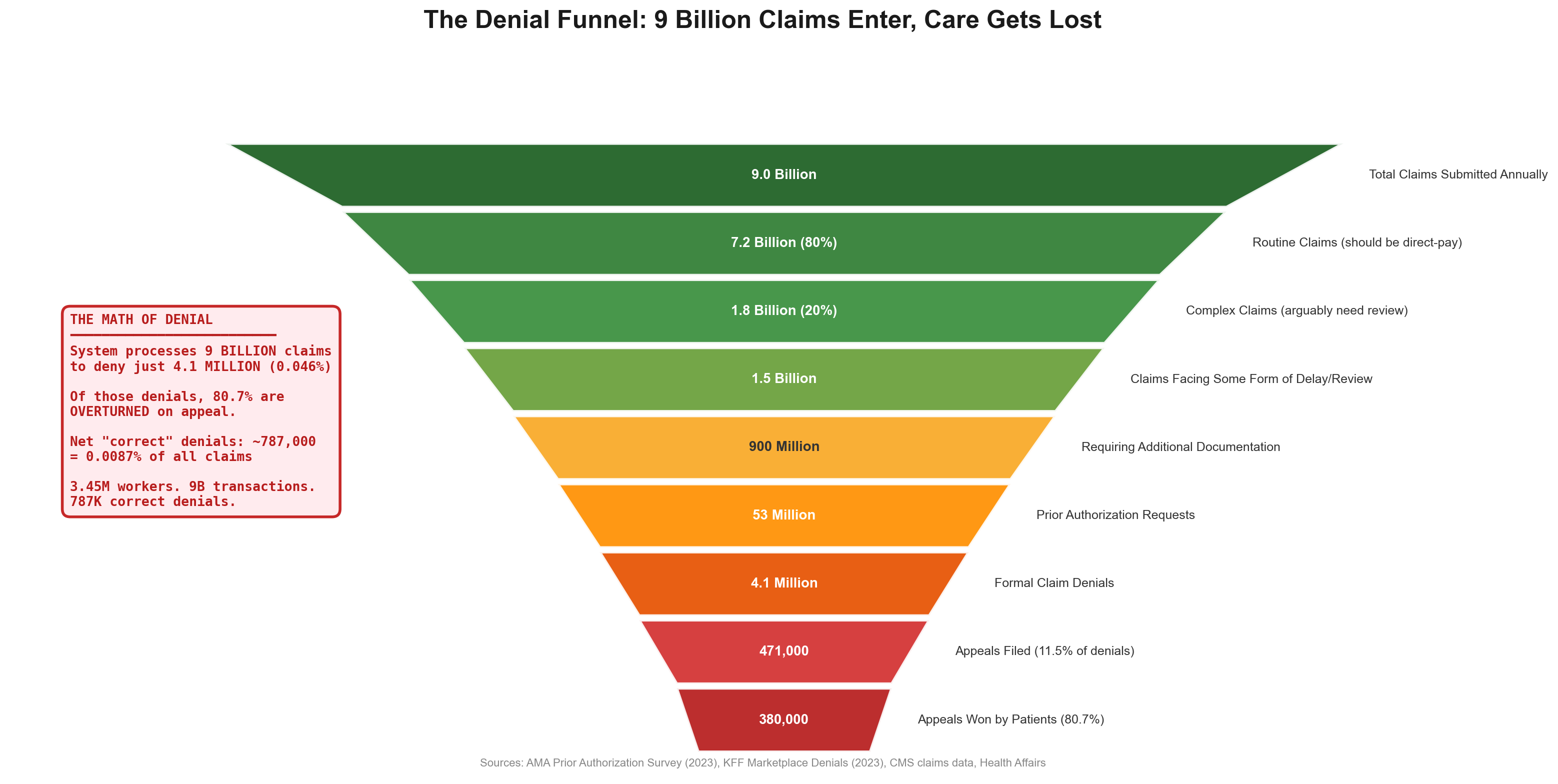

Insurance companies operate the most sophisticated denial-based extraction. Medicare Advantage insurers submitted 53 million prior authorization requests in 2024—1.7 requests per enrollee—denying 4.1 million claims with an 80.7% appeal overturn rate that proves systematic inappropriate denials. [7] Yet only 11.5% of patients even appeal, meaning 3.3 million medically necessary treatments go denied annually while insurers profit from patient fatigue with bureaucratic barriers. This care vs. denial economy employs approximately 2.4 million workers whose primary function involves preventing patients from receiving appropriate treatment. [8]

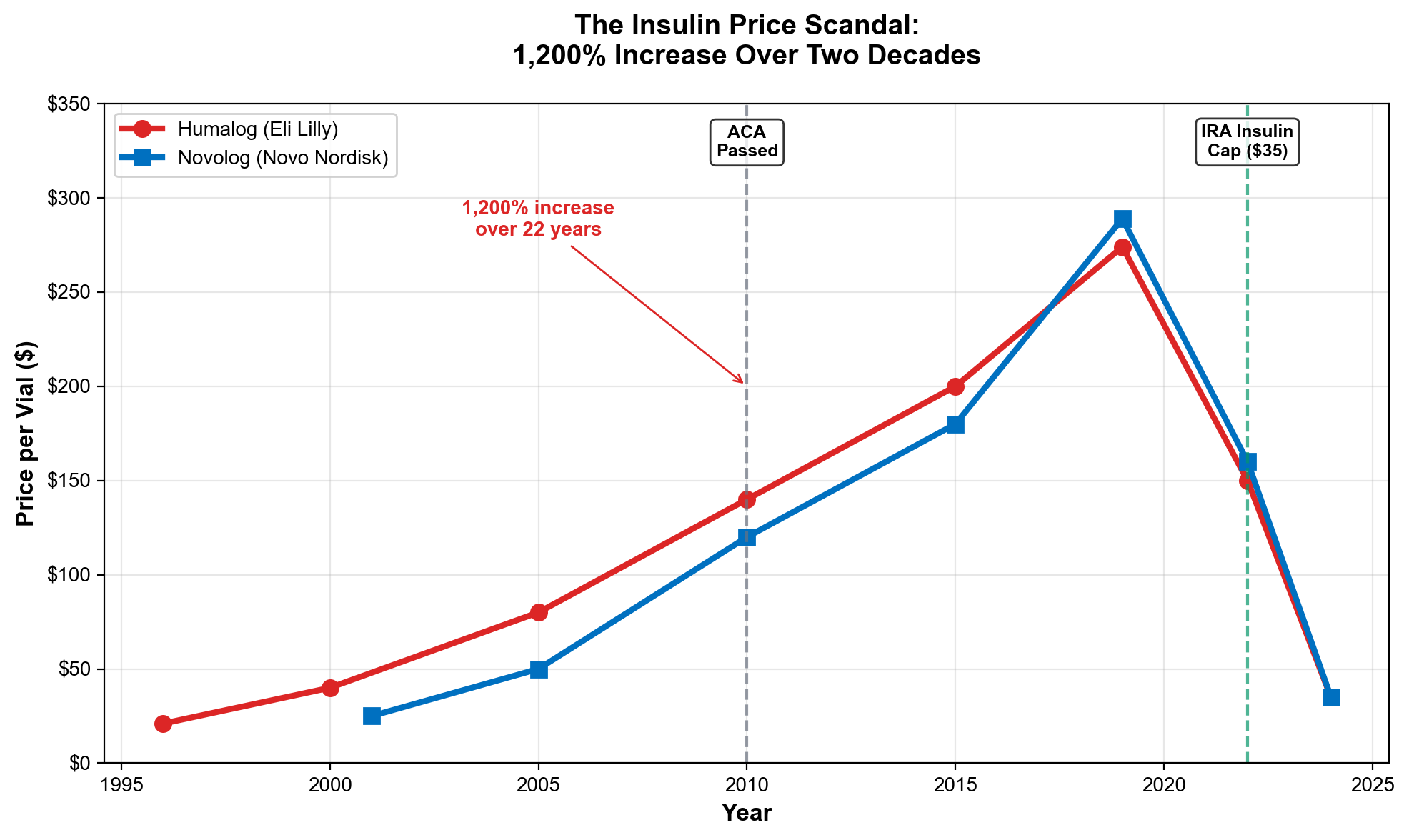

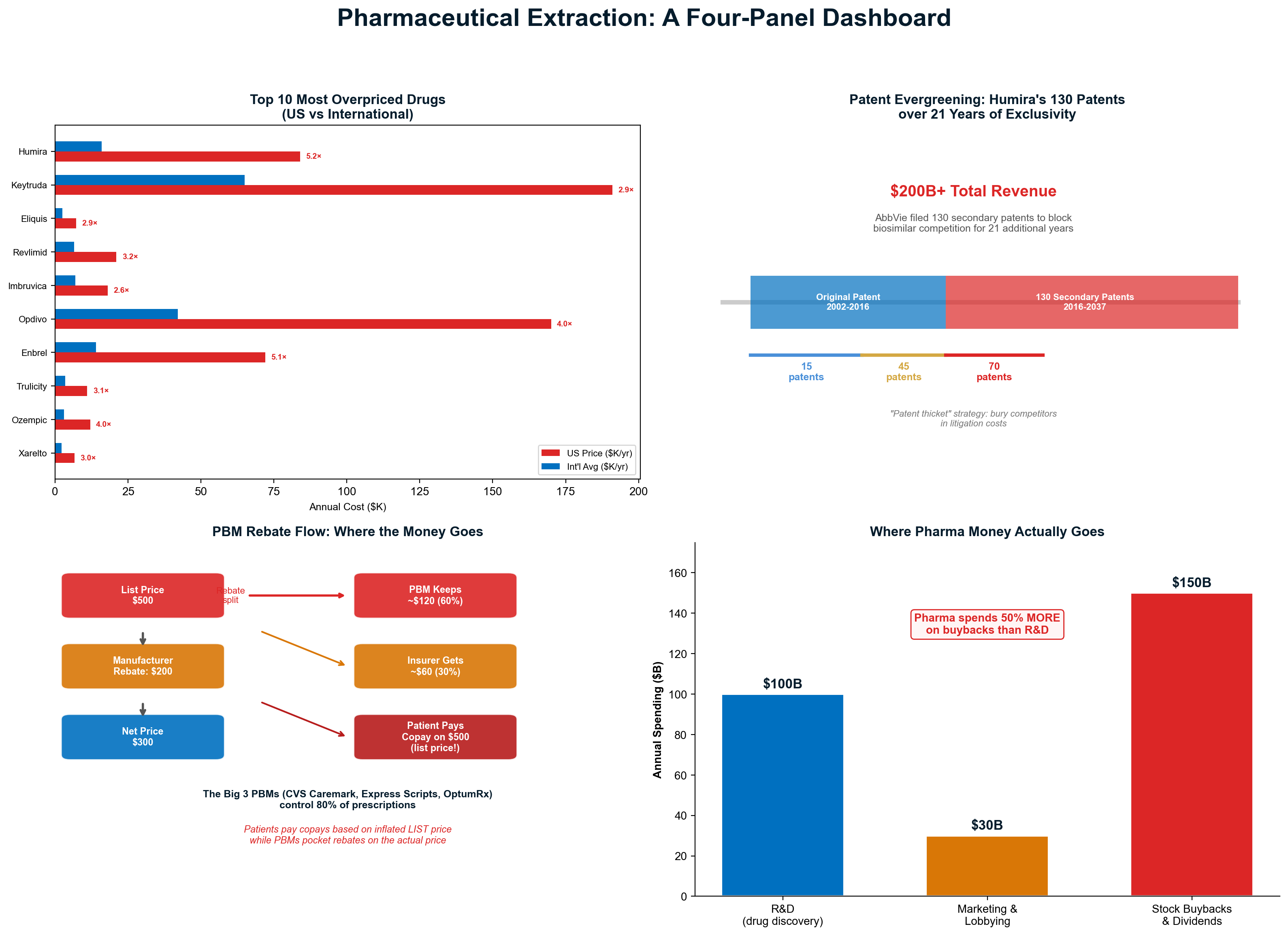

The pharmaceutical extraction machine inflated insulin prices from $21 to $274+ per vial through Pharmacy Benefit Manager manipulation—a 1,200% increase enabled by "rebate walls" that blocked lower-cost alternatives while PBMs collected billions in hidden rebates. [9] Patent evergreening extends drug monopolies an average of six years beyond original 20-year protection, with 70% of top-selling drugs using secondary patents to block competition. Humira maintained 21 years of exclusivity through 130+ secondary patents, generating over $200 billion in monopoly profits that would have faced generic competition under normal patent expiration. [10]

Scope inflation analysis reveals insurance processing 80% routine, predictable transactions like $4 generic prescriptions and $150 office visits that don't warrant intermediation but maximize administrative revenue through Medical Loss Ratio gaming. Processing 7.2 billion routine claims annually at $12-15 per claim generates $86-108 billion in extractive overhead on transactions that could be handled through direct payment in 30 seconds versus 6 weeks of insurance complexity. [11]

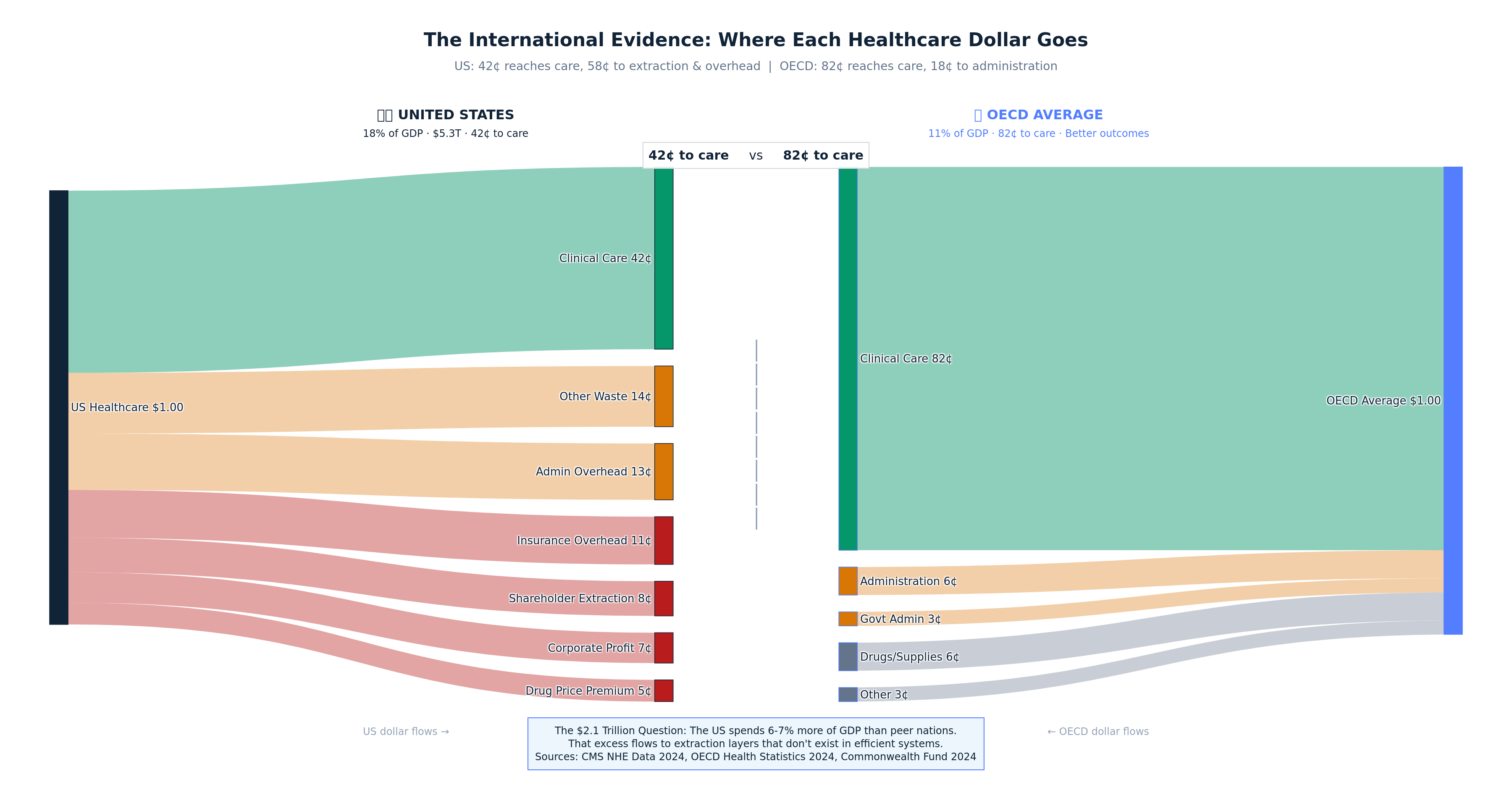

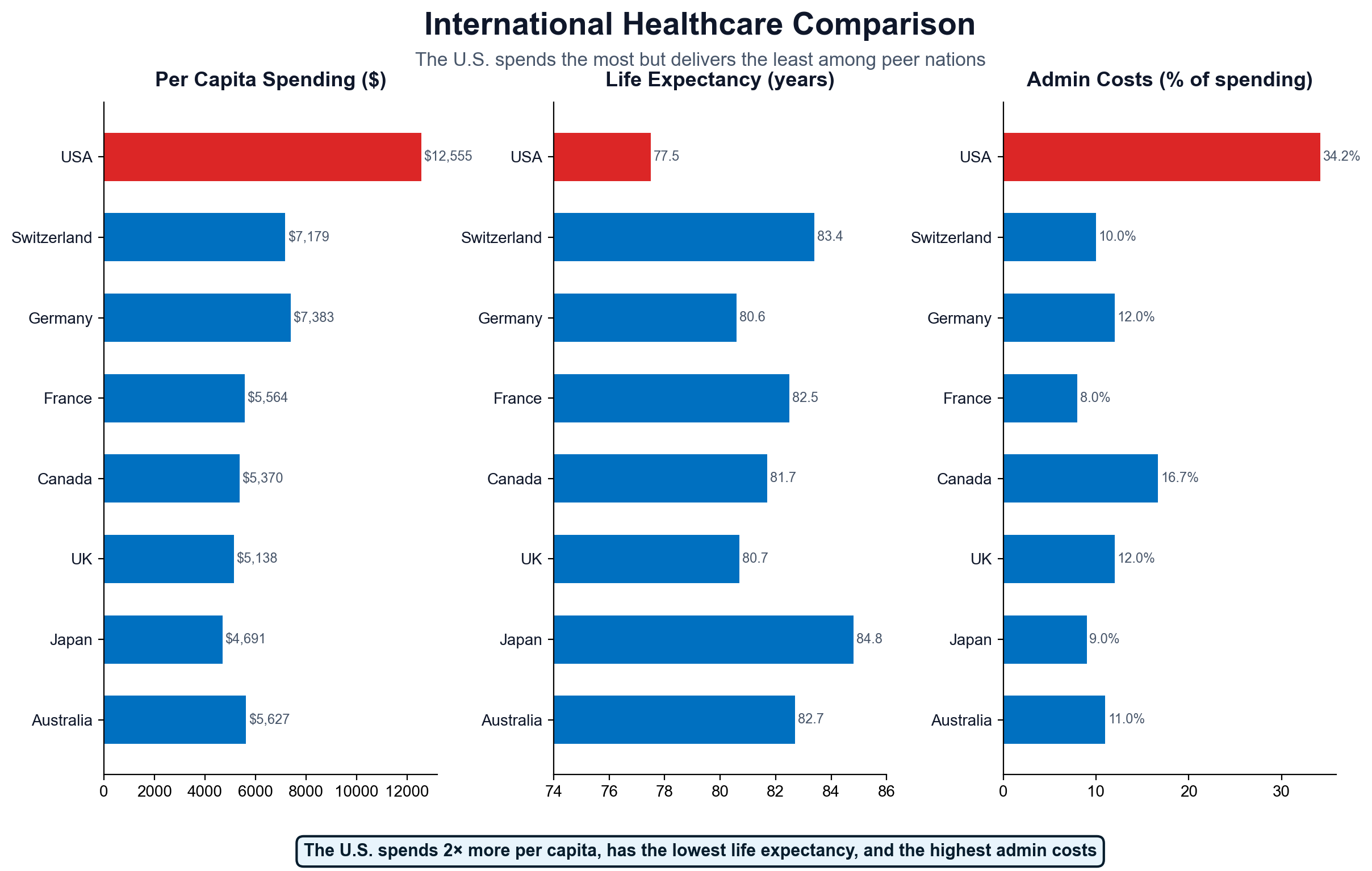

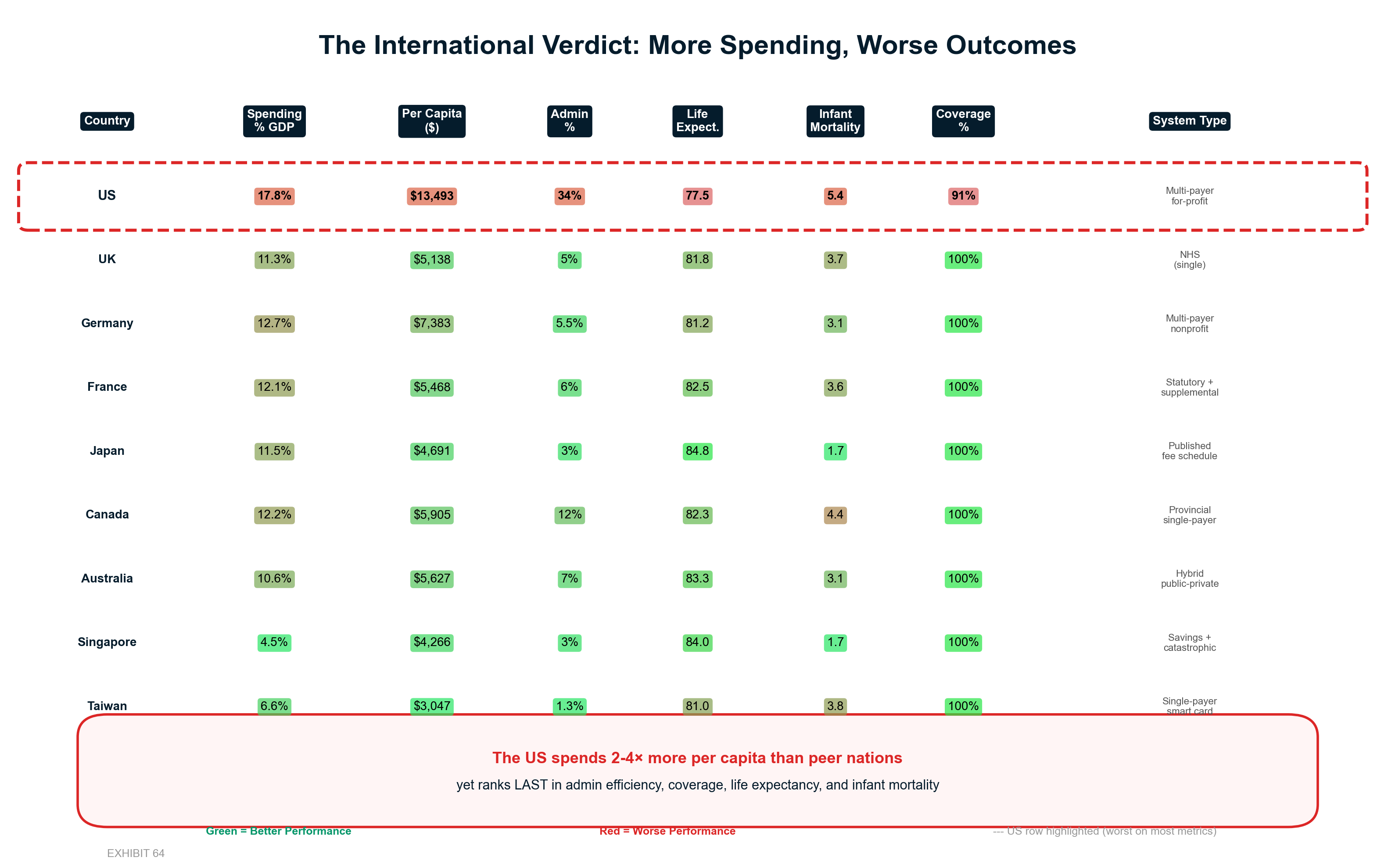

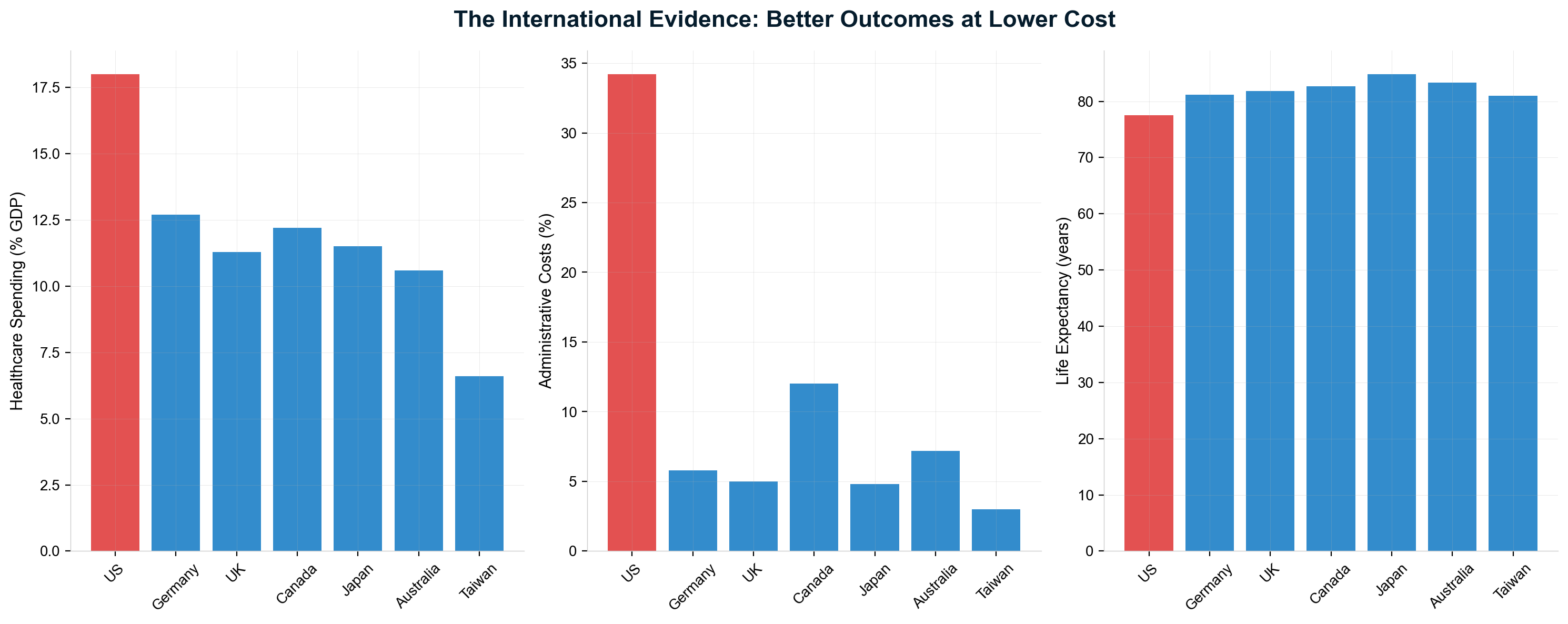

International comparison exposes the full scale of American extraction. The US spends 18% of GDP on healthcare while peer nations achieve superior outcomes spending 11-12% of GDP—a 6-7 percentage point difference representing approximately $2.1 trillion in annual excess spending that flows to extraction layers rather than care delivery. [12] While the UK spends $8 billion on healthcare administration and Canada spends $12 billion, America's administrative overhead alone exceeds $400 billion annually—money that could provide universal coverage with significant cost savings if redirected to care.

For a typical American family spending $25,000 annually on healthcare, $6,250-8,750 goes to pure extraction rather than medical care

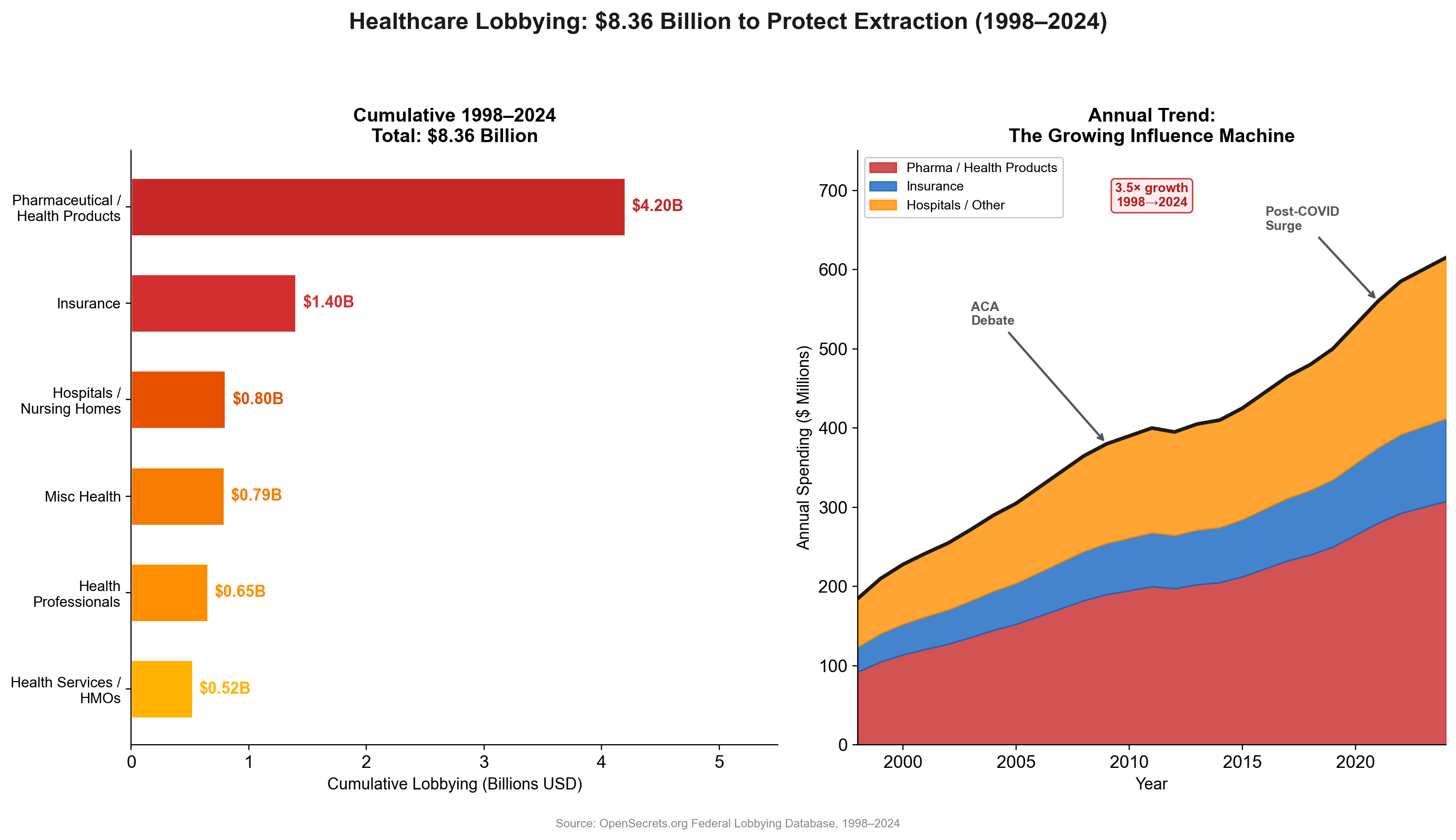

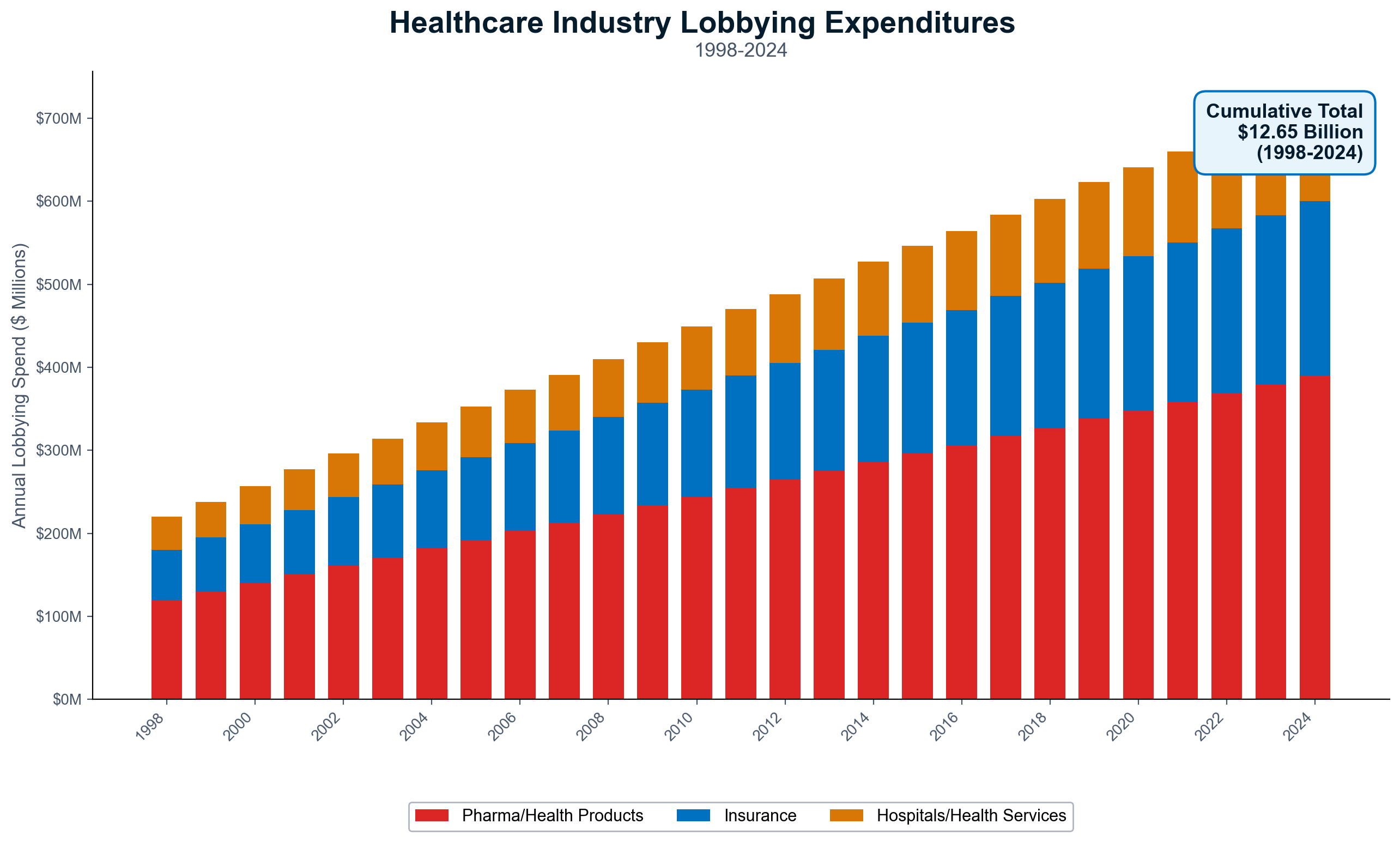

The extraction timeline reveals this system was constructed through 75+ years of systematic policy choices that prioritized industry profits over patient welfare. From the 1947 Taft-Hartley Act weakening labor's healthcare negotiating power, through the 2003 Medicare Modernization Act prohibiting government drug price negotiation, to recent vertical mergers totaling $149 billion (CVS-Aetna, UnitedHealth-Change Healthcare, Cigna-Express Scripts), every major expansion of extraction was enabled by specific legislative actions that strengthened corporate control while socializing costs and privatizing profits. [13]

The December 4, 2024 assassination of UnitedHealthcare CEO Brian Thompson crystallized decades of accumulated public anger over healthcare extraction, triggering unprecedented discourse about industry practices while revealing the depth of frustration over systematic denial of care by executives receiving $26+ million compensation packages. [14] Public reaction demonstrated growing awareness that healthcare has become wealth extraction rather than care delivery.

This is not market failure—it is market manipulation. The extraction machine operates through deliberate opacity, regulatory capture, and systematic elimination of competition. Every major healthcare crisis response has ultimately benefited industry more than patients, deepening corporate control through reforms that strengthen extraction mechanisms while maintaining appearance of patient protection.

The evidence is overwhelming: approximately 42¢ of every healthcare dollar reaches actual patient care, with 58¢ extracted through financial engineering, administrative complexity, insurance intermediation, pharmaceutical manipulation, and stock market wealth creation. For 130 million American households, this represents the largest single wealth transfer operation in the modern economy—larger than most national economies—systematically moving resources from families facing medical necessity to corporate shareholders who contribute nothing to healing.

This report documents the mechanisms, quantifies the extraction, and exposes how a system theoretically designed for healing became a machine optimized for wealth extraction. The evidence demands immediate action to restore healthcare's mission of patient care over profit maximization.

Table of Contents

- Introduction: The Architecture of Extraction

- Where Every Dollar Goes — The National Healthcare Dollar

- Sector-Level Cash Flows

- The Extraction Timeline — How We Got Here

- Vertical Integration — The Conglomerate Machine

- Hospital Consolidation & the For-Profit Machine

- PBM & Pharmacy Benefit Extraction

- Insurance Industry Financial Engineering

- The Stock Market Extraction Machine

- Pharmaceutical Extraction

- Private Equity — The Extraction Playbook

- Administrative Complexity & the Shadow Economy

- The Care Prevention Economy

- Price Collusion & Opacity

- Legislative & Regulatory Capture

- Corporate Profiles — Villains & Heroes

- The Human Cost

- International Lessons — How Other Nations Avoided the Trap

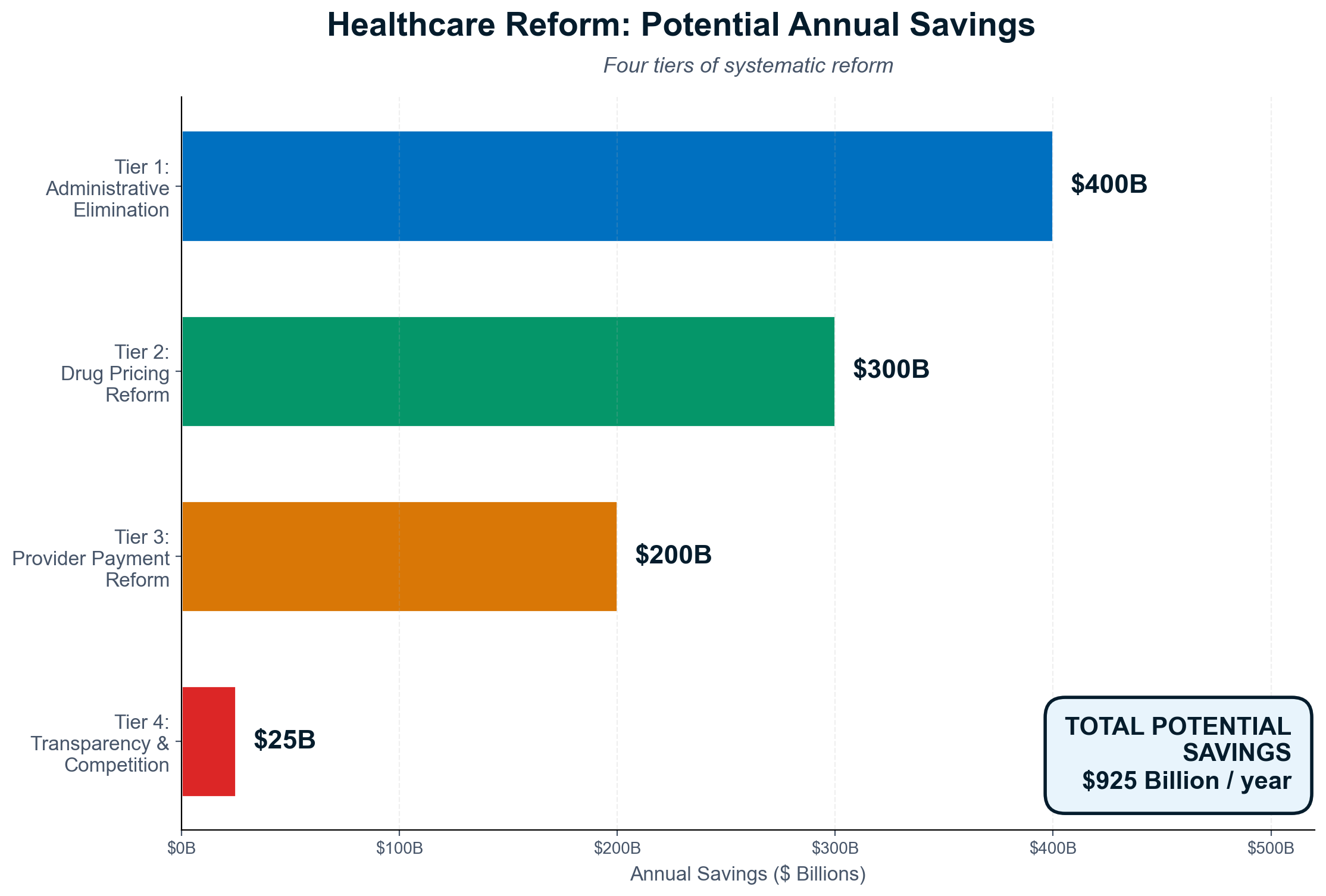

- Policy Recommendations — Dismantling the Machine

- What Universal Care Could Look Like

- Synthesis — Reclaiming Healthcare for Patients

- Sankey Diagram Gallery

- Bibliography

The Reform Moment

Healthcare reform is experiencing a political resurgence. In April 2026, CNN analysis documented a new wave of Democratic candidates winning primary elections on explicitly single-payer platforms — the first time since Bernie Sanders' 2016 campaign that Medicare-for-All has demonstrated electoral viability. [183] Lt. Gov. Juliana Stratton won Illinois' Democratic Senate primary championing single-payer healthcare, while progressive candidates across multiple states made universal coverage their centerpiece issue.

The political landscape has shifted because the economic reality has become undeniable. According to projections shared with CNN by John Holahan of the Urban Institute, the 10-year cost of implementing federal single-payer would be nearly twice the 2020 estimate — not because universal coverage became more expensive, but because the extraction-based system's costs continued accelerating faster than any reform proposal could match. [183]

This paper's specific contribution is to assess the economics of the system as a whole — to trace where the $5.3 trillion actually goes, who captures it, and what structural changes would redirect those flows toward patient care. Before examining reform pathways, we must first understand the extraction machine that any reform must dismantle.

The starting point is life expectancy. Among 38 OECD nations, the United States ranks last at 76.4 years, despite spending approximately twice what peer nations spend per capita on healthcare. [136] This paradox — maximum spending, minimum outcomes — is not a market failure but a design feature. The system is optimized for wealth extraction, not health production.

How to Read the Healthcare Economy

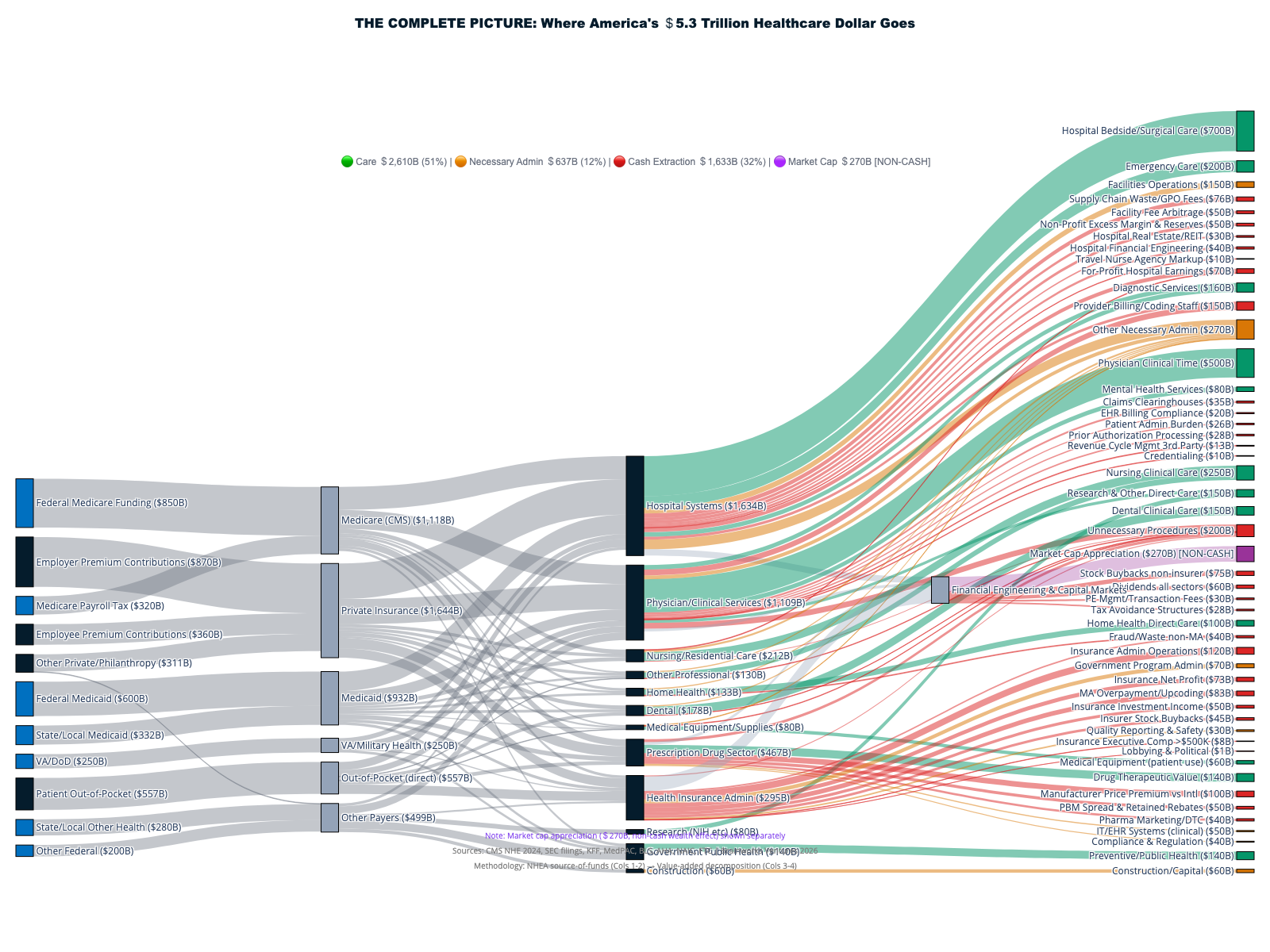

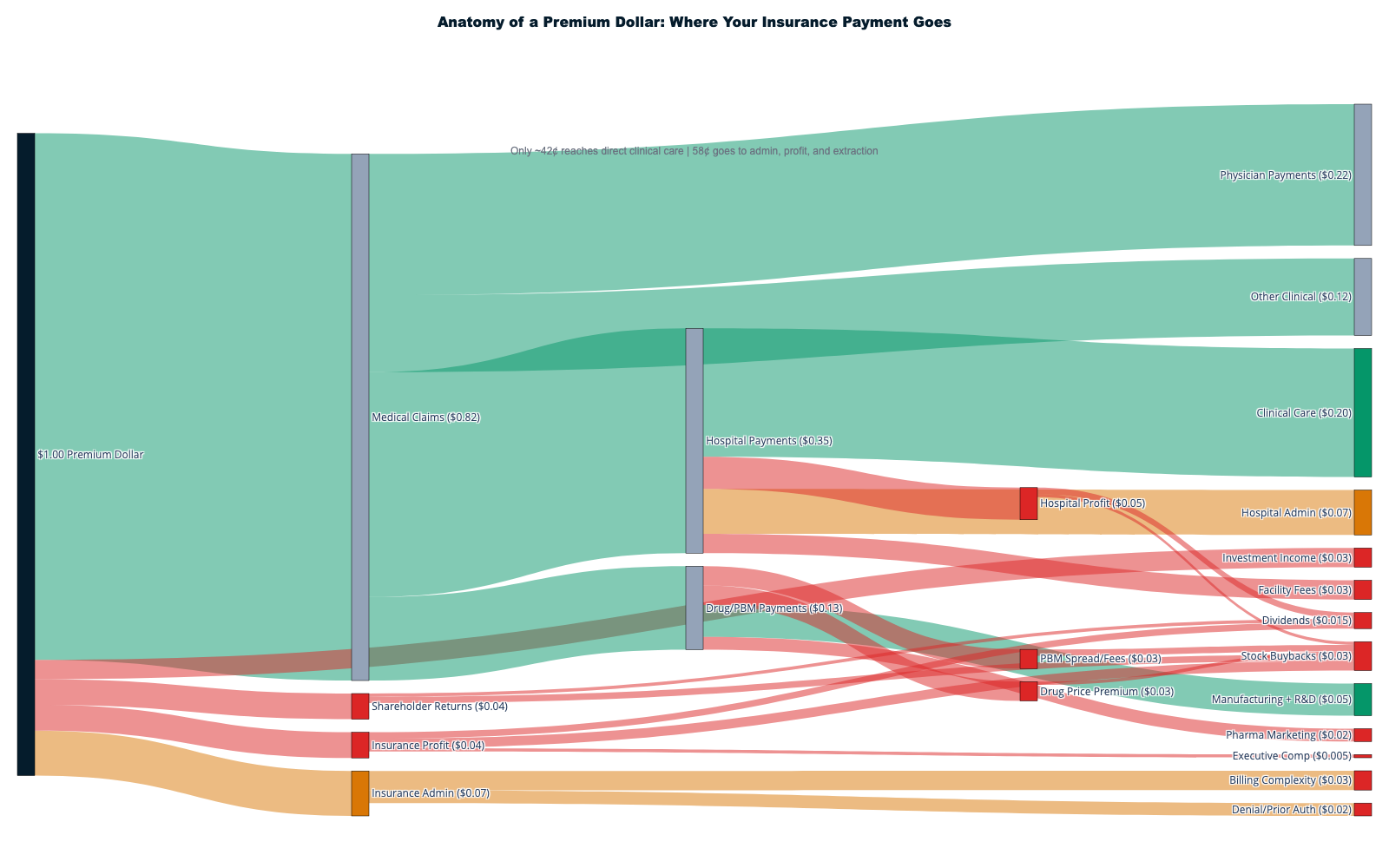

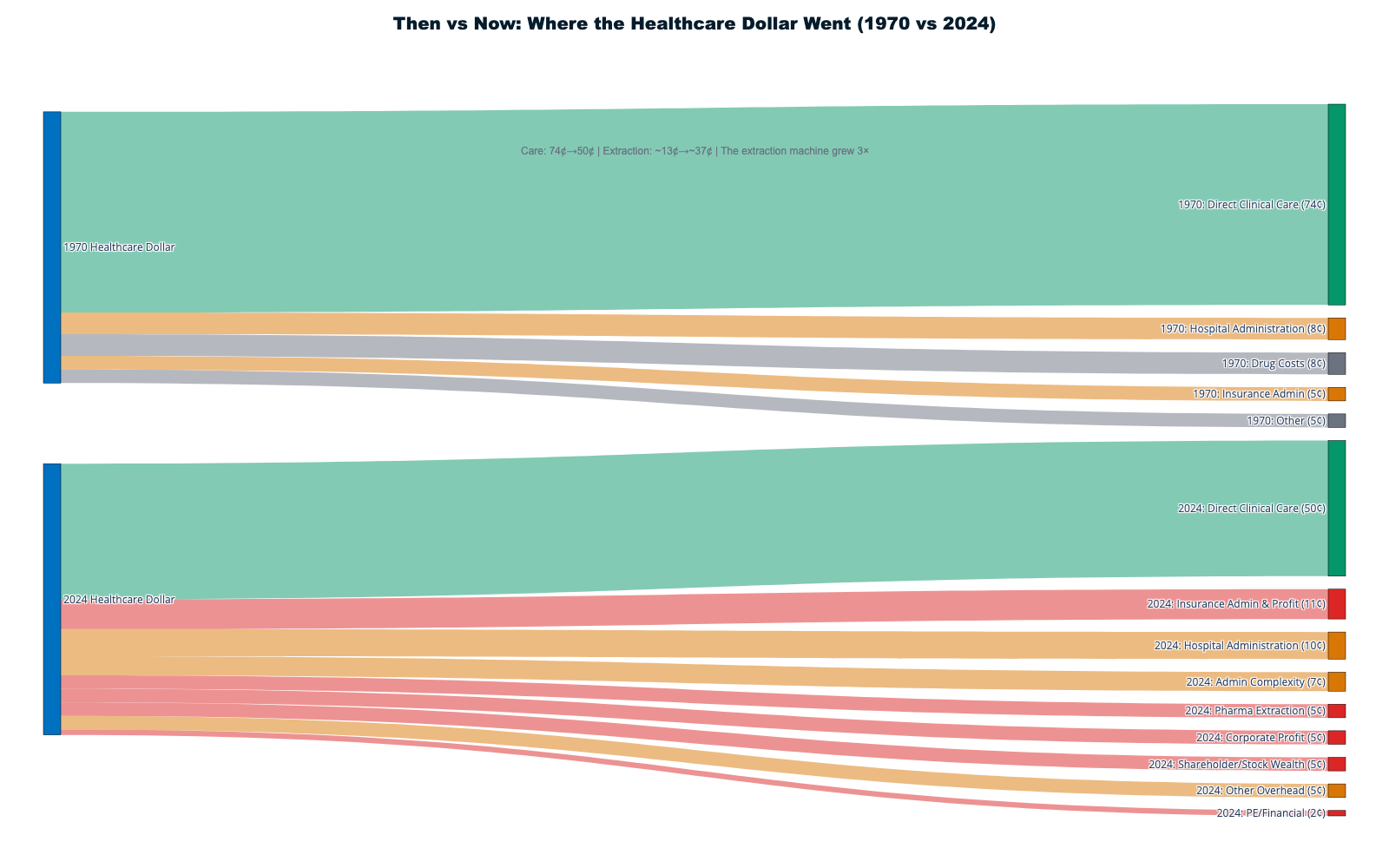

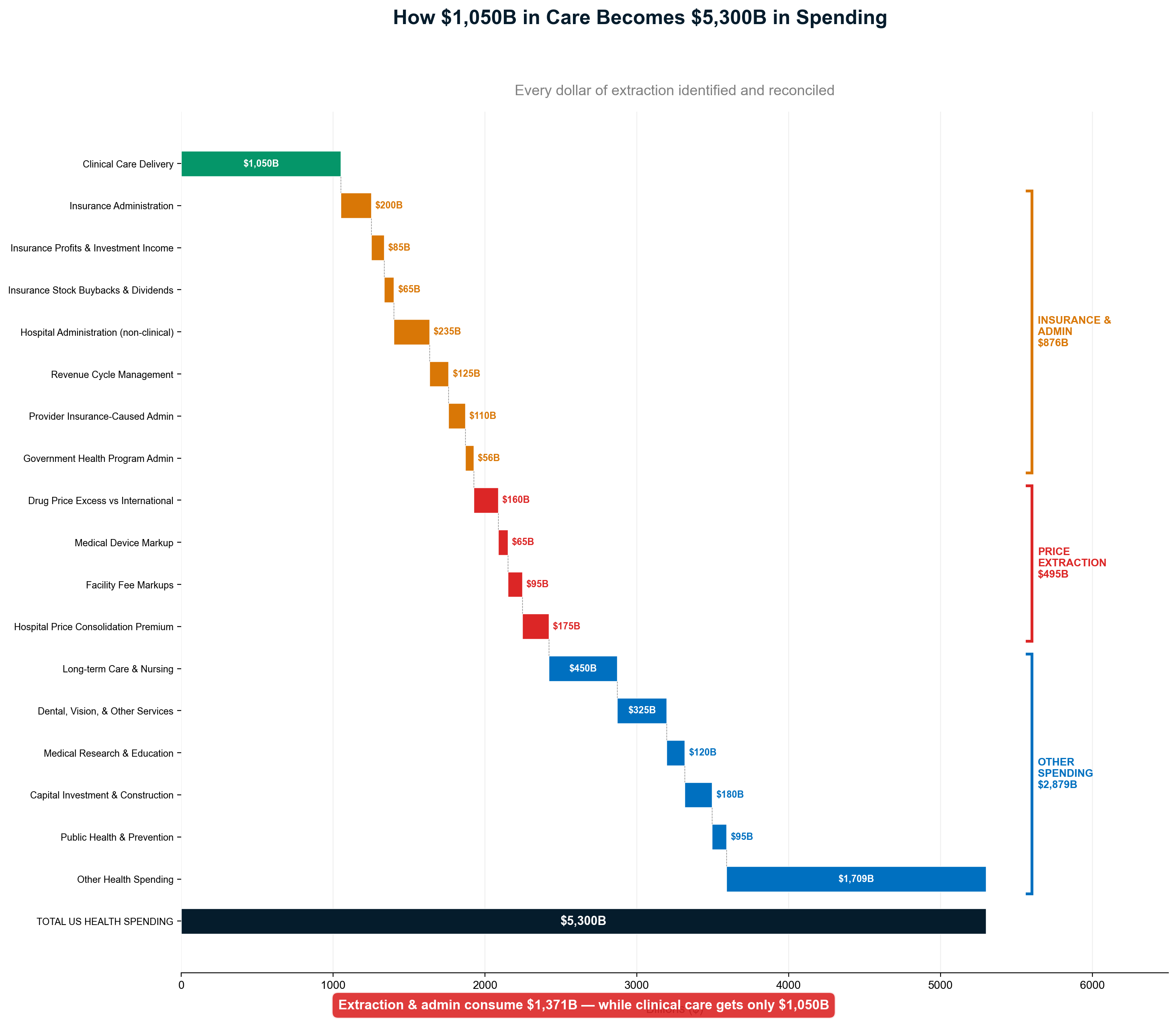

Before diving into extraction mechanisms, it helps to understand the basic architecture of American healthcare finance. The Centers for Medicare & Medicaid Services (CMS) publishes an annual accounting of the "nation's health dollar." [184] Where the money comes from: Federal programs ($2.7T, 51%), private insurance ($1.644T, 31%), out-of-pocket ($557B, 10%), other ($399B, 8%). Where CMS says it goes: Hospital care ($1.5T), physician services ($940B), prescription drugs ($405B), other ($2.5T).

The CMS accounting, however, tells only half the story. It tracks spending categories but not extraction layers — the difference between what enters the healthcare system and what emerges as patient care. This report performs that deeper accounting: by tracing every dollar through its complete journey, we reveal that approximately 42 cents of every healthcare dollar actually reaches patient care, while 58 cents is captured by extraction mechanisms that exist in no peer-nation healthcare system.

Accounting Methodology: Avoiding Double Counting

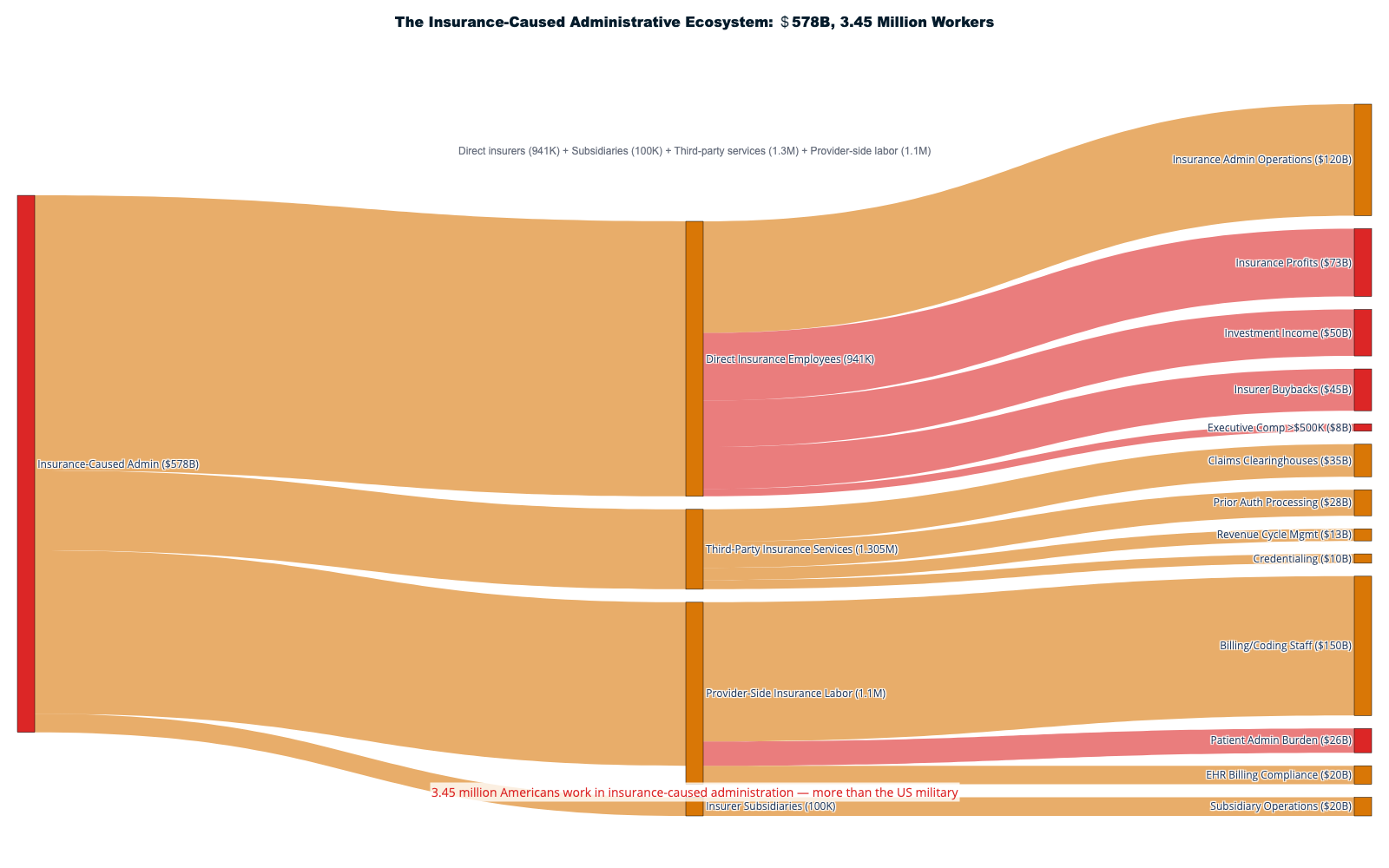

This report's extraction accounting draws on the National Health Expenditure Accounts (NHEA), maintained by CMS, which uses a "payer of last resort" framework to assign each healthcare dollar to a single payer category — ensuring that dollars are not counted twice as they pass through intermediaries. [184] Our extraction analysis preserves this discipline by identifying mutually exclusive cost categories: direct insurance company costs ($316B) — administrative operations, net profits, executive compensation, and shareholder distributions that occur within insurer balance sheets; provider-side administrative burden ($236B) — the costs hospitals and physicians incur specifically to comply with insurance complexity (billing staff, prior authorization processing, revenue cycle management, credentialing, EHR billing compliance); and patient-side administrative burden ($25B) — the time and welfare costs patients bear navigating the insurance system. These three categories sum to $578B in total insurance intermediation costs, with no dollar appearing in more than one category.

A brief note on frameworks: the NHEA tracks spending flows — where healthcare dollars come from and where they go — making it the appropriate lens for tracing extraction pathways. The Bureau of Economic Analysis's National Income and Product Accounts (NIPA), by contrast, measures value creation — each industry's contribution to GDP. Under NIPA accounting, health insurance's "output" equals only its net margin (premiums minus claims paid), roughly $160-250 billion on a $1.6 trillion premium base, because NIPA treats insurers as financial intermediaries rather than producers. We use the NHEA framework throughout this report because our purpose is documenting where money flows and who captures it — not measuring industry GDP contribution. For readers interested in the distinction, see the CMS National Health Expenditure methodology and BEA/NHEA reconciliation literature. [227]

Understanding the Numbers: NHEA vs NIPA Frameworks

Two federal accounting systems measure the American healthcare economy, and they tell strikingly different stories about the insurance industry's role. Understanding the distinction is essential for interpreting this report's extraction figures.

The National Health Expenditure Accounts (NHEA), maintained by CMS, tracks where healthcare dollars flow — who pays, who receives, and how much passes through each intermediary. Under NHEA accounting, private health insurance is the dominant non-government payer, channeling $1.644 trillion (31% of all health spending) from premium payers to providers, while retaining a portion for administration and profit. This is the framework we use throughout this report, because our purpose is tracing extraction pathways — documenting where money enters the system and where it is captured before reaching patient care.

The National Income and Product Accounts (NIPA), maintained by the Bureau of Economic Analysis (BEA), measures value creation — what each industry contributes to GDP. Under NIPA, the health insurance industry's "output" equals only its net margin: premiums collected minus claims paid out, roughly $160-250 billion on a $1.6 trillion premium base. NIPA treats insurers as financial intermediaries — pass-through entities whose economic product is the administrative service of managing risk and processing payments, not the medical claims they fund.

The two frameworks tell quite different stories: NHEA treats private insurance as the dominant payer (31% of spending), while NIPA treats the insurance industry as a relatively modest administrative services sector whose GDP contribution is a fraction of the premiums flowing through it. Neither framework is "wrong" — they measure different things. But the choice of framework profoundly shapes how one perceives the industry's economic footprint.

Our analysis uses NHEA flows because we are documenting extraction pathways, not measuring GDP contribution. When we say insurance intermediation costs $578 billion annually, we are tracing the full economic burden the insurance system imposes on the healthcare economy — including costs borne by providers and patients navigating insurance complexity — not just the industry's net margin. For technical details on how NHEA and NIPA reconcile, see CMS National Health Expenditure methodology [184] and BEA healthcare satellite account documentation. [227]

Chapter 1: Where Every Dollar Goes — The National Healthcare Dollar

Every dollar of America's $5.3 trillion healthcare spending begins a journey through the most sophisticated extraction machine in the global economy. [1] (See Volume I, Chapter 3 for the statistical model.) To understand where healthcare dollars actually go, we must trace their complete path from funding sources through multiple intermediary layers before any clinical care reaches patients. The destination reveals a system optimized for wealth transfer rather than healing, with extraction mechanisms so pervasive that most healthcare spending never touches patient care.

The funding sources tell only the beginning of this story. Federal, state, and local governments contribute $2.7 trillion through Medicare ($1.118T), Medicaid ($931.7B), and other programs ($590.5B). [1] Private health insurance provides $1.644 trillion, representing premiums paid by employers ($980B) and individuals ($664B). Out-of-pocket spending accounts for $556.6 billion in direct patient payments. Each dollar immediately encounters what industry insiders call "revenue optimization"—a euphemism for systematic wealth extraction before any medical service occurs.

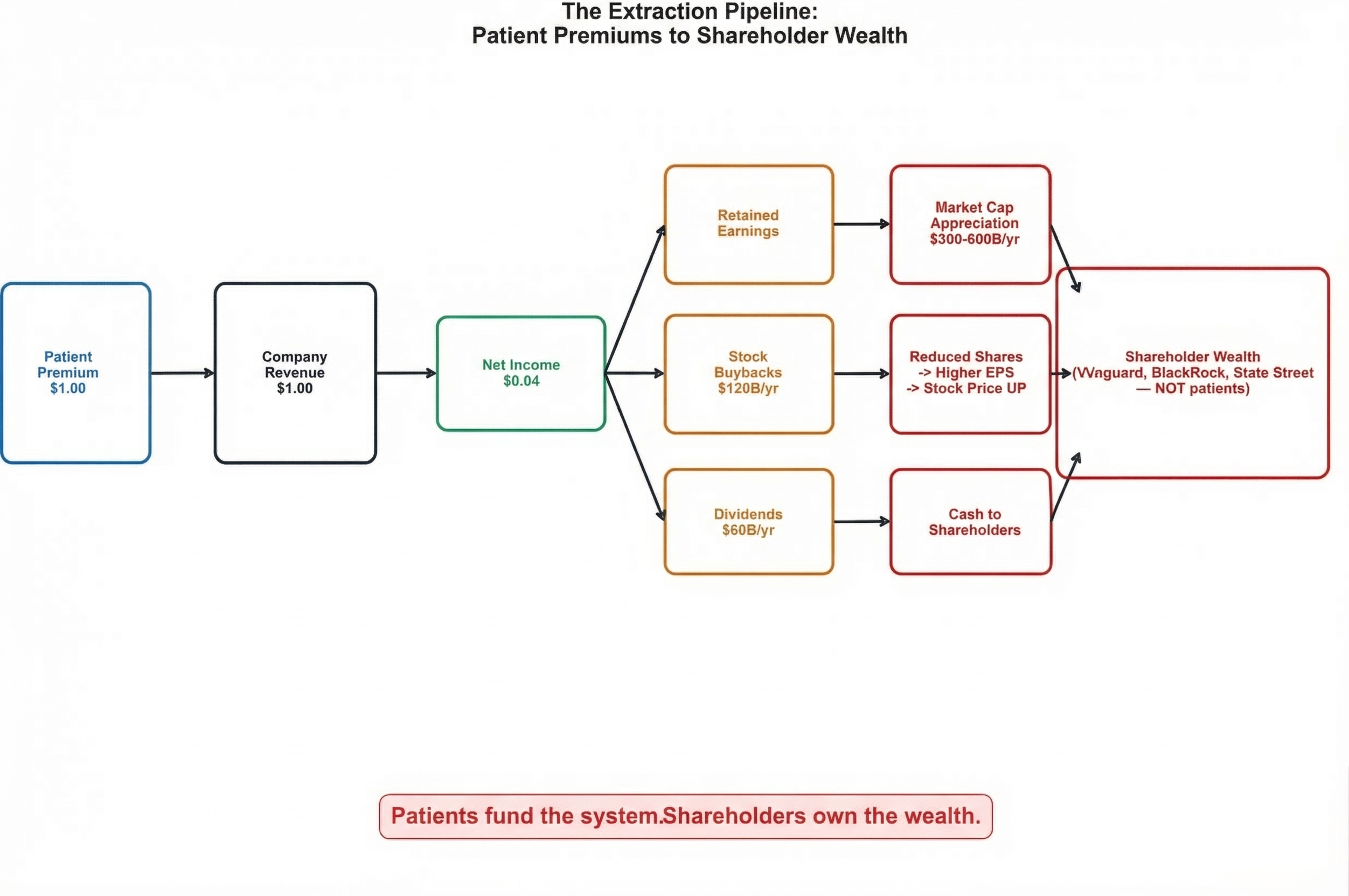

The Premium-to-Stock-Price Pipeline

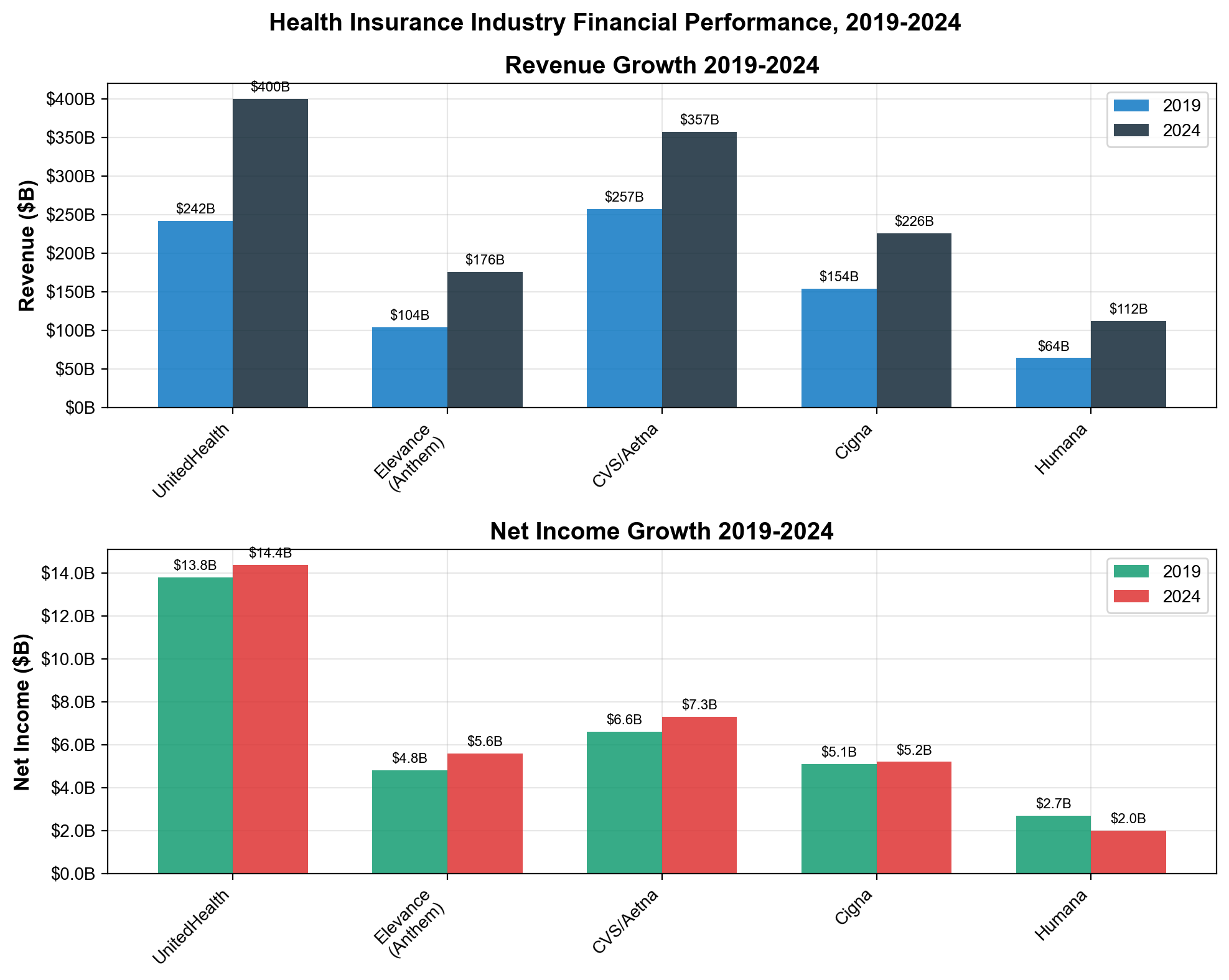

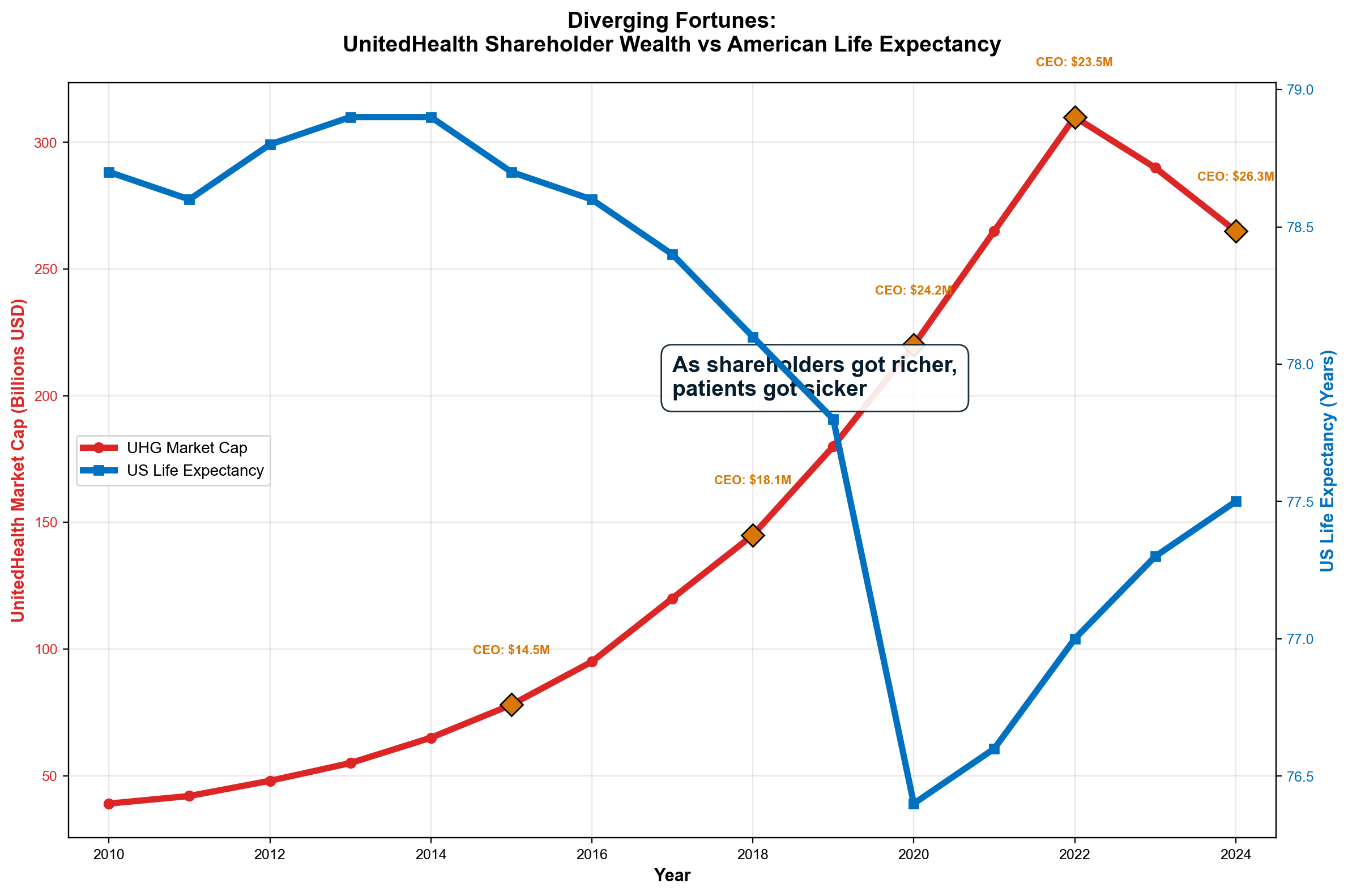

The most significant but hidden extraction mechanism operates through stock market capitalization that converts patient premiums into permanent shareholder wealth. UnitedHealth Group exemplifies this system: $400+ billion in annual revenue drives market valuations reflecting the net present value of expected future extraction, creating shareholder value that dwarfs reported profits. [2] The company's market capitalization expansion from $39 billion (2010) to $265 billion (2026) represents $226 billion in wealth creation funded entirely by patient premiums and government subsidies—money that patients pay but shareholders capture.

This stock appreciation pathway operates through a simple chain: patient premiums generate company profits, profit expectations drive stock price increases, and stock buyback programs convert unrealized gains into concentrated shareholder wealth. UnitedHealth's $42 billion in stock repurchases between 2018-2024 represents patient premium dollars flowing directly to shareholders through a mechanism invisible to premium-paying patients who fund but never benefit from the wealth creation they enable. [3]

Stock Market Extraction: $180 billion in cash (buybacks + dividends) drives $450 billion in total shareholder wealth creation through market cap appreciation—the amplification effect that makes extraction self-reinforcing

Health insurer stock performance proves extraction as investment strategy. The sector increased 1,032% from ACA enactment through 2024, compared to 251% S&P 500 growth—a 4:1 outperformance achieved not through improved health outcomes but through extraction optimization. [4] When UnitedHealth maintains industry-leading prior authorization denial rates while generating massive stock appreciation, financial markets validate systematic care denial as profitable corporate strategy.

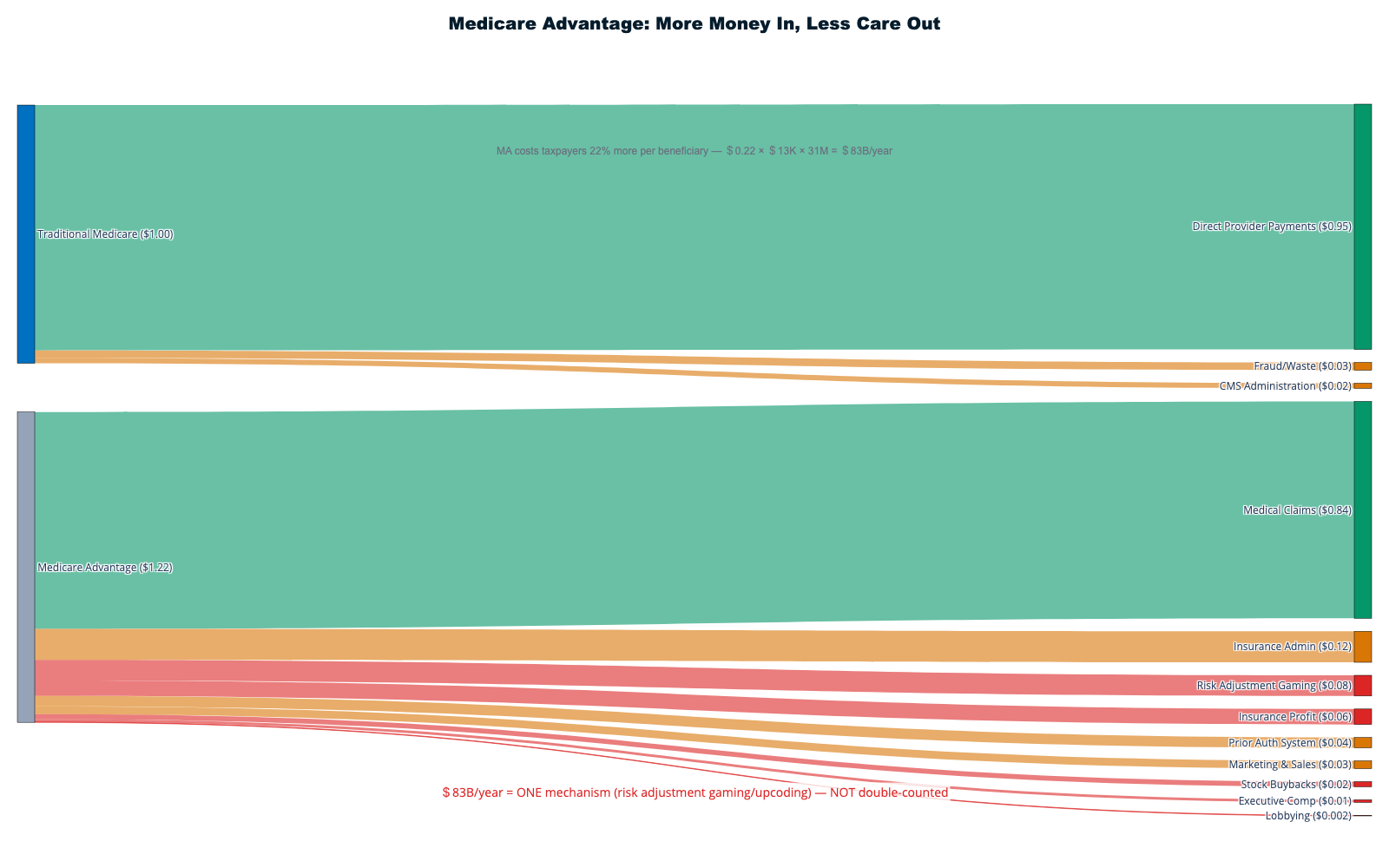

Insurance Intermediation: The $578 Billion Overhead Layer

Private insurance companies represent the most visible extraction layer through Medical Loss Ratio requirements that legally permit 9-20% retention of all premium revenue for administrative costs and profits. [5] This extraction occurs regardless of care quality or patient outcomes, creating incentives to increase total spending rather than improve efficiency. UnitedHealth's 2024 performance demonstrates the mechanism: $400.3 billion revenue with 85.5% MLR generated $58 billion in non-medical extractions that funded $25.7 billion net income and $16.5 billion in shareholder returns. [6]

But the true cost of insurance intermediation extends far beyond what appears on company balance sheets. The complete accounting reveals insurance as pure administrative overhead:

Direct Insurance Company Costs: $316 billion annually

- Administrative operations: $120B

- Net profits: $73B (includes $50B investment income from premium float)

- Shareholder distributions: $65B (buybacks + dividends, funded from profits and accumulated reserves)

- Executive compensation above $500K: $8B [7]

Provider-Side Costs Imposed by Insurance Complexity: $236 billion annually

- Provider billing and coding staff: $150B

- Prior authorization processing: $35B

- Revenue cycle management: $13B

- Credentialing administration: $10B

- EHR billing compliance systems: $20B

- Claims clearinghouse fees: $8B [8]

Patient-Side Administrative Burden: $26 billion annually

- Insurance navigation time valued at minimum wage

- Care delays due to authorization requirements

- Suboptimal treatment paths due to network restrictions [9]

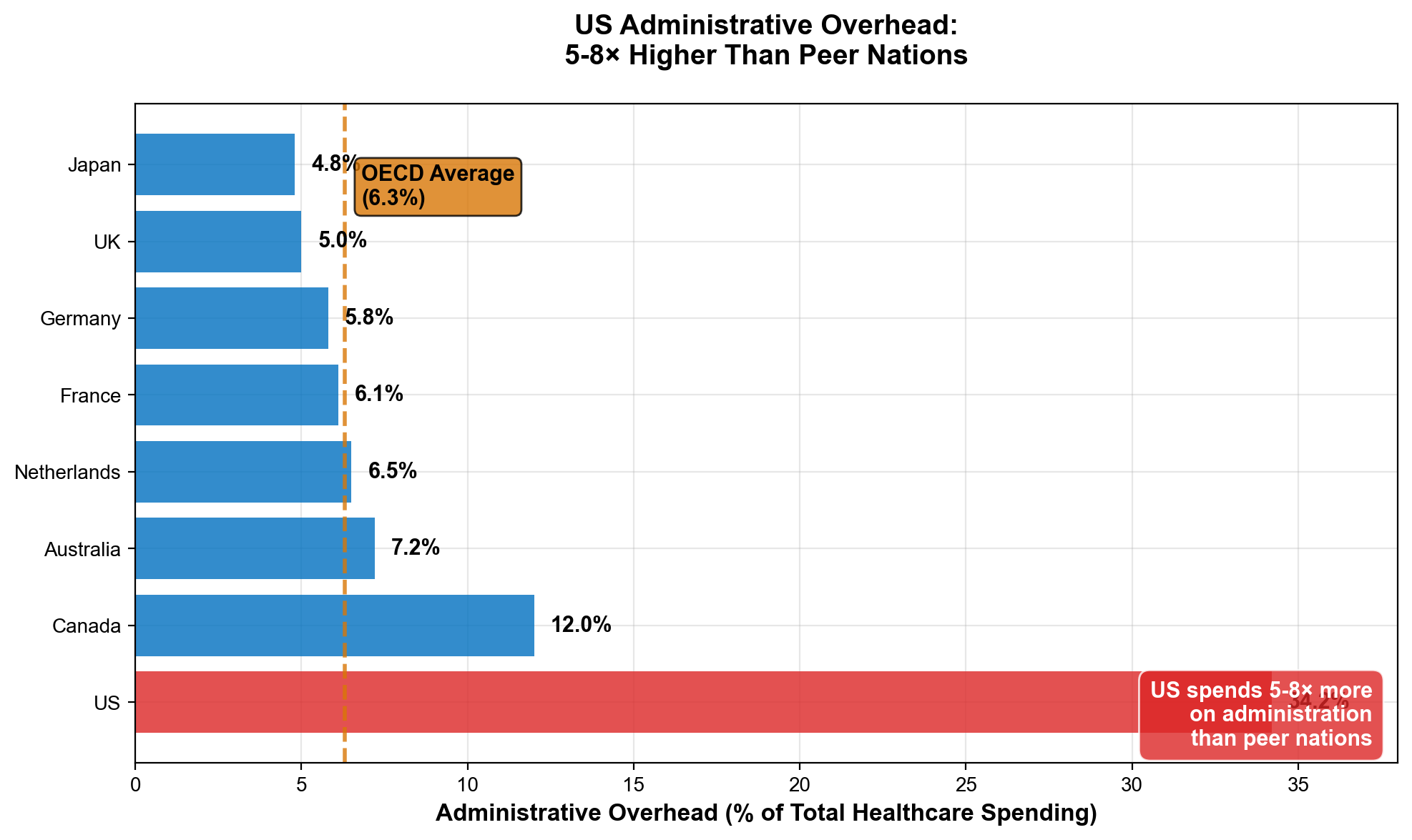

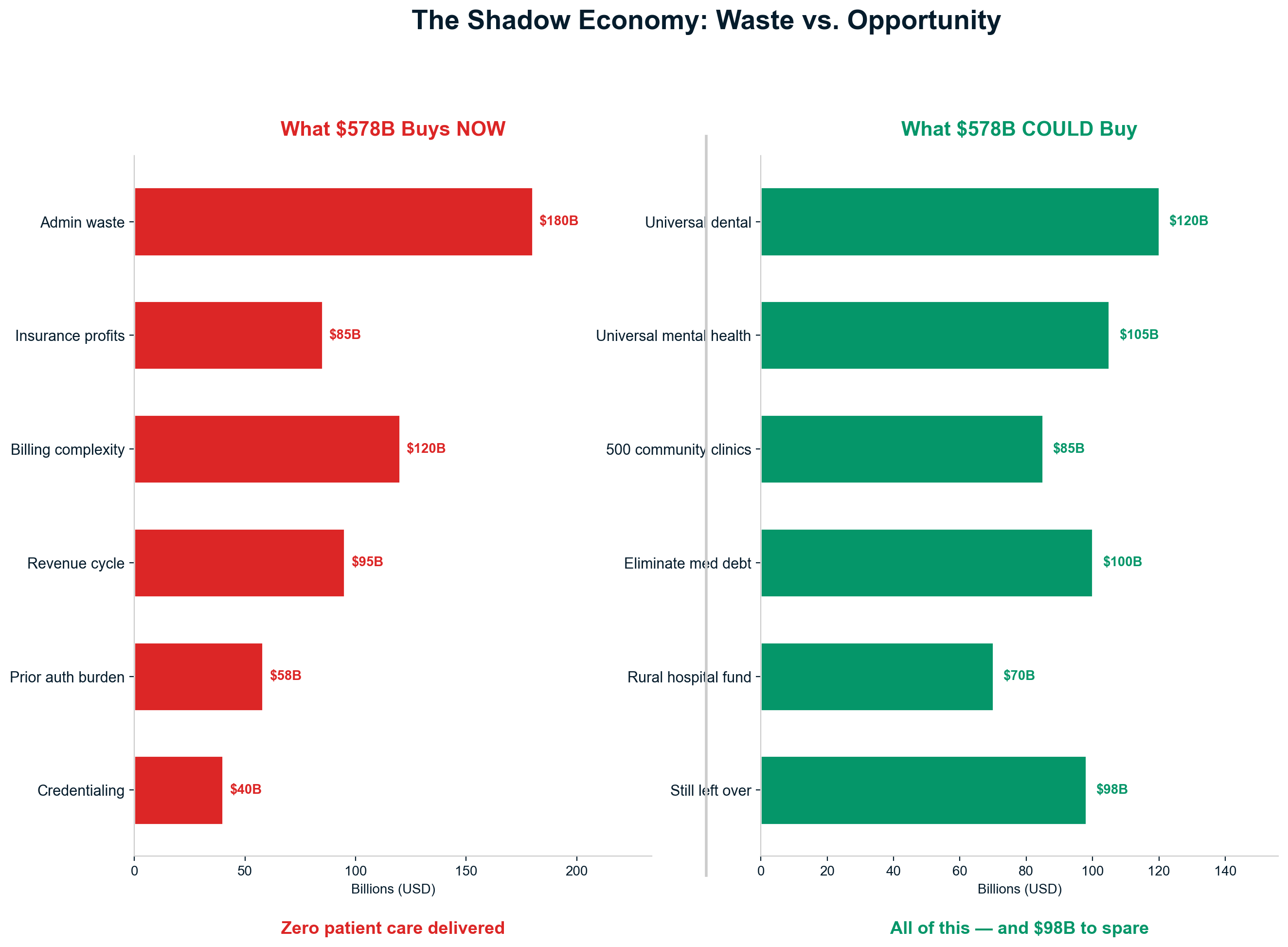

Total Insurance Intermediary Cost: $578 billion annually—representing 30-35% of healthcare spending devoted to administration rather than care delivery. Single-payer systems achieve identical intermediary functions at $30-50 billion annually, meaning America spends $528-548 billion in excess administrative costs to maintain private insurance profits. [10]

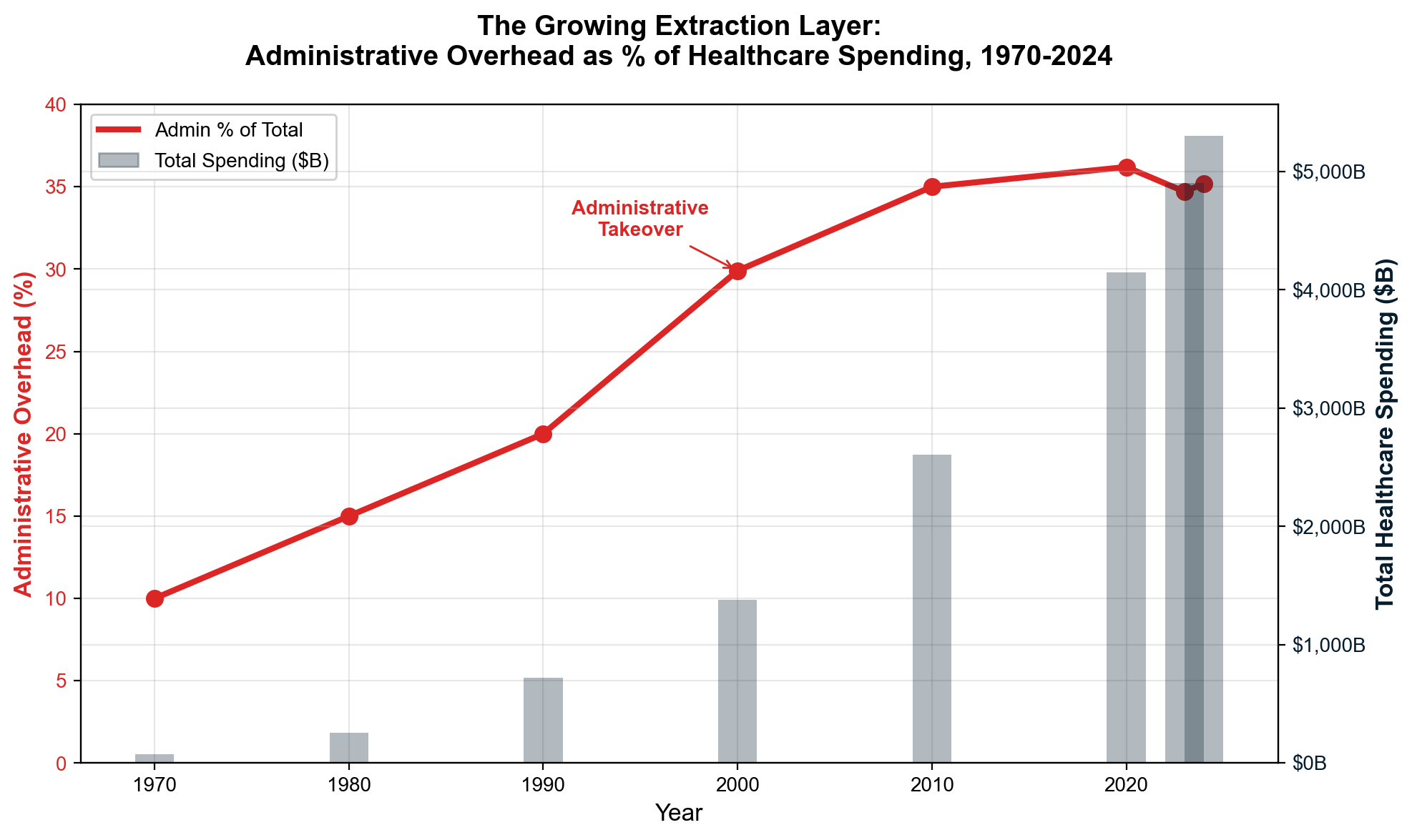

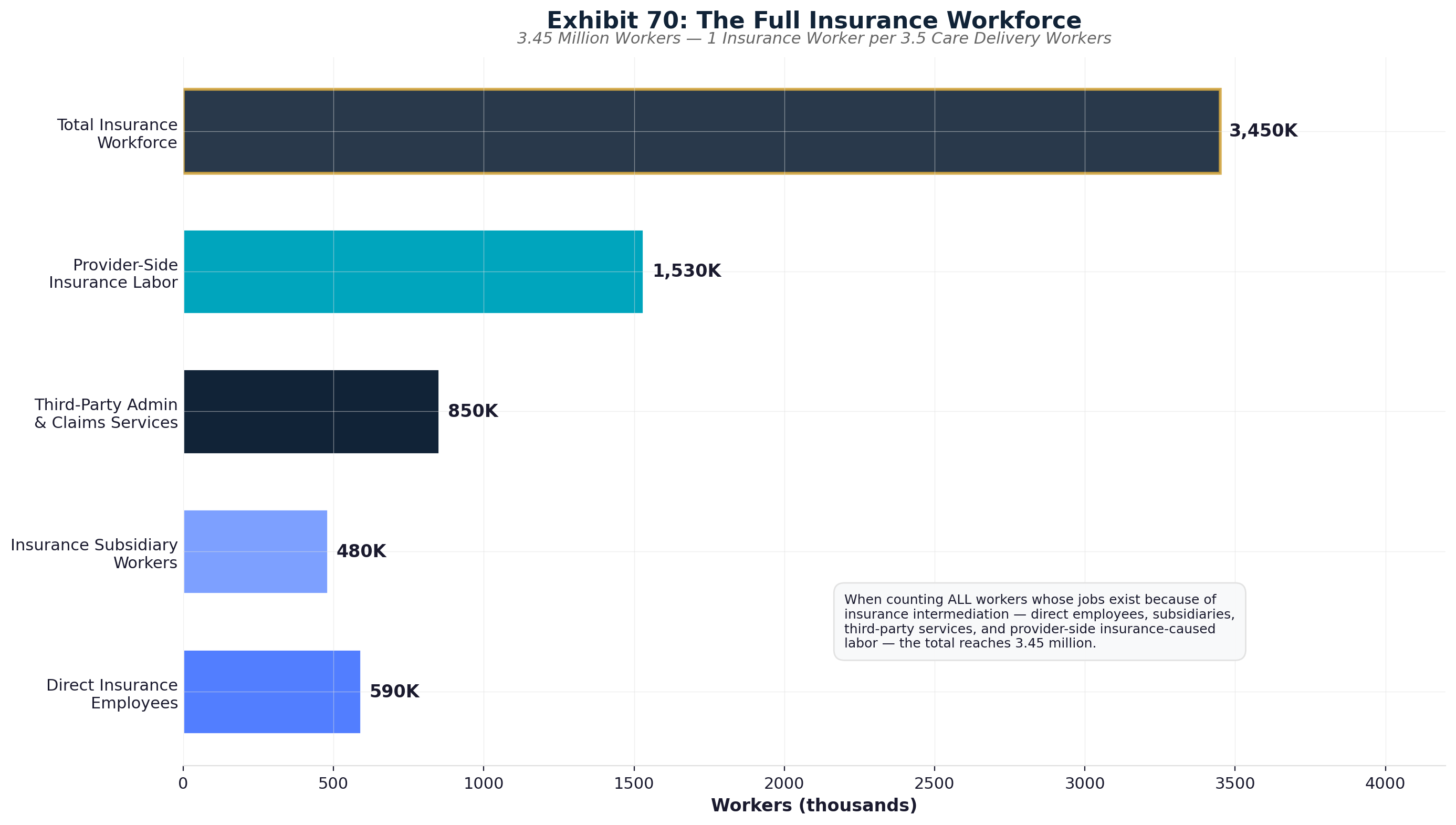

The Administrative Shadow Economy

Healthcare administration has grown into America's largest artificial industry, employing 12-15 million workers whose jobs exist solely to navigate complexity that adds no clinical value. [11] The 12-15 million figure includes workers at UnitedHealth Group (400,000 employees), CVS Health (300,000), Anthem/Elevance Health (100,000), claims processing firms like R1 RCM (30,000+), EHR companies like Epic Systems (13,000), prior authorization processors like eviCore (7,500), plus thousands of smaller billing, coding, and revenue cycle management firms — including an estimated 100,000+ offshore workers in India and the Philippines processing American medical billing. This shadow economy includes:

The Full Insurance Ecosystem: 3.45 million workers — none delivering care

UnitedHealth Group (400,000 workers), CVS Health (300,000), Anthem/Elevance Health (100,000), and other insurers employ massive bureaucracies focused exclusively on extraction optimization rather than care delivery. These workers process claims, manage prior authorizations, develop billing algorithms, and optimize denial mechanisms—generating $90-112.5 billion in annual wages for activities that produce zero medical benefits. [12]

Revenue Cycle Management Industry: 208,000+ workers

Companies like R1 RCM exist solely to navigate billing complexity that wouldn't exist under simplified payment systems. Including offshore operations in India and the Philippines processing American medical billing, this industry generates $12-15 billion annually in wages for workers managing artificial administrative requirements. [13]

Prior Authorization Industry: 30,500 workers

Companies like eviCore exist purely to deny medically necessary care through bureaucratic obstruction, employing workers whose primary function involves preventing patients from receiving appropriate treatment. Annual wage bill: $1.8 billion for systematic care denial that generates zero clinical value. [14]

What These Workers Could Do Instead

The 12-15 million workers trapped in healthcare administrative complexity represent enormous opportunity cost for American economic development. These workers could staff manufacturing reshoring, infrastructure development, educational expansion, or climate response rather than processing artificial complexity that subtracts value from society while enabling extraction from patients and taxpayers. [15]

International Extraction Differential

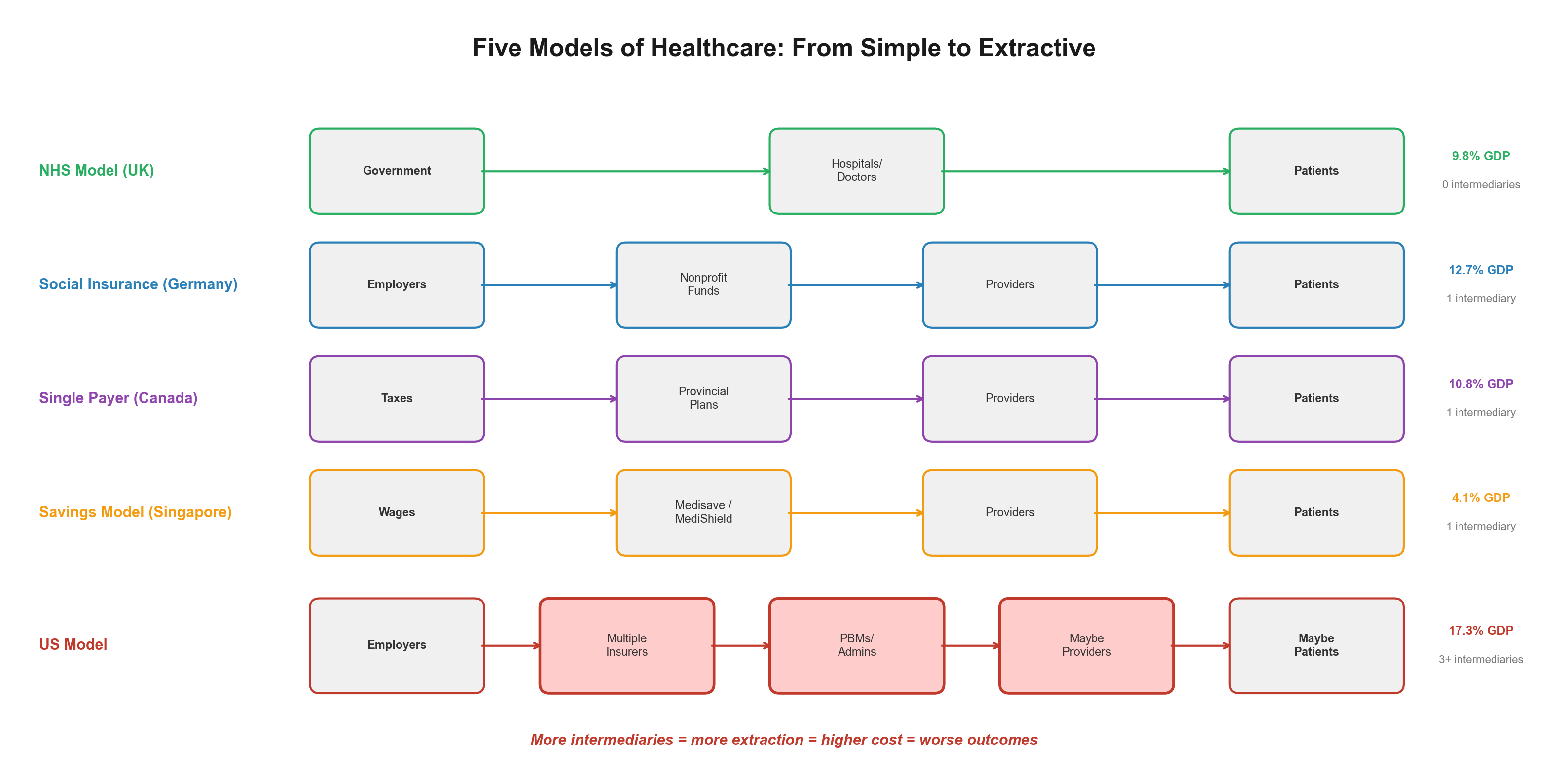

Single-payer systems demonstrate that healthcare intermediation can operate at 1-3% administrative cost while achieving superior population health outcomes. The administrative differential reveals the scale of American extraction:

- United Kingdom: $8 billion annual administrative costs (2% of healthcare spending)

- Canada: $12 billion annual administrative costs (3% of healthcare spending)

- Germany: $20 billion annual administrative costs (4% of healthcare spending). Note: Germany operates a mixed system — approximately 88-89% of the population is covered by statutory nonprofit sickness funds, while 11% (high-income earners, civil servants, and self-employed) may opt for private health insurance. Even the private component operates under heavy regulation including all-payer rate setting. [185]

- United States: $400+ billion annual administrative costs (7.5% of healthcare spending)

The US spends 18% of GDP on healthcare while peer nations achieve better outcomes spending 11-12% of GDP. [16] This 6-7 percentage point difference represents approximately $2.1 trillion in annual excess spending—money flowing to extraction layers that simply don't exist in efficiently organized healthcare systems.

The Scope Inflation Revenue Model

Insurance companies have deliberately expanded beyond catastrophic risk pooling to process every routine healthcare transaction—not because patients need intermediation for $4 prescriptions or $150 office visits, but because processing every transaction maximizes the administrative revenue base from which insurers extract their fixed percentage profits. [17]

The Mathematical Reality

- 9 billion claims processed annually in the US

- 80% are routine/predictable services (not catastrophic)

- Average processing cost: $12-15 per claim

- Total routine claim volume: 7.2 billion claims annually

- Administrative extraction on routine claims: $86-108 billion annually [18]

This scope inflation explains why insurers supported the ACA's Essential Health Benefits mandate—it guaranteed maximum transaction volume and administrative revenue. The medical necessity of insurance intermediation for routine care is negative: administrative overhead often exceeds actual service costs, making insurance a cost-increasing rather than risk-pooling mechanism for predictable healthcare needs.

The Cumulative Extraction Impact

When aggregating all extraction mechanisms, the complete flow reveals that approximately 42¢ of every healthcare dollar reaches actual patient care delivery:

Extraction Layers Consuming 58¢ of Each Dollar:

- Insurance intermediation overhead: 11¢

- Stock market wealth creation: 6-11¢

- Administrative complexity: 8¢

- Pharmaceutical manipulation: 4¢

- Hospital facility fee arbitrage: 3¢

- Private equity debt service: 2¢

- Executive compensation excess: 1¢

- Lobbying and political spending: 1¢

- Other extraction mechanisms: 12-17¢

Care Delivery Receiving 42¢ of Each Dollar:

- Physician compensation: 8¢

- Nursing and clinical staff: 14¢

- Medical equipment and supplies: 7¢

- Pharmaceuticals (at manufacturing and distribution cost, excluding patent monopoly premiums, PBM intermediation, and marketing): 6¢

- Facility operations: 4¢

- Medical research and development: 3¢

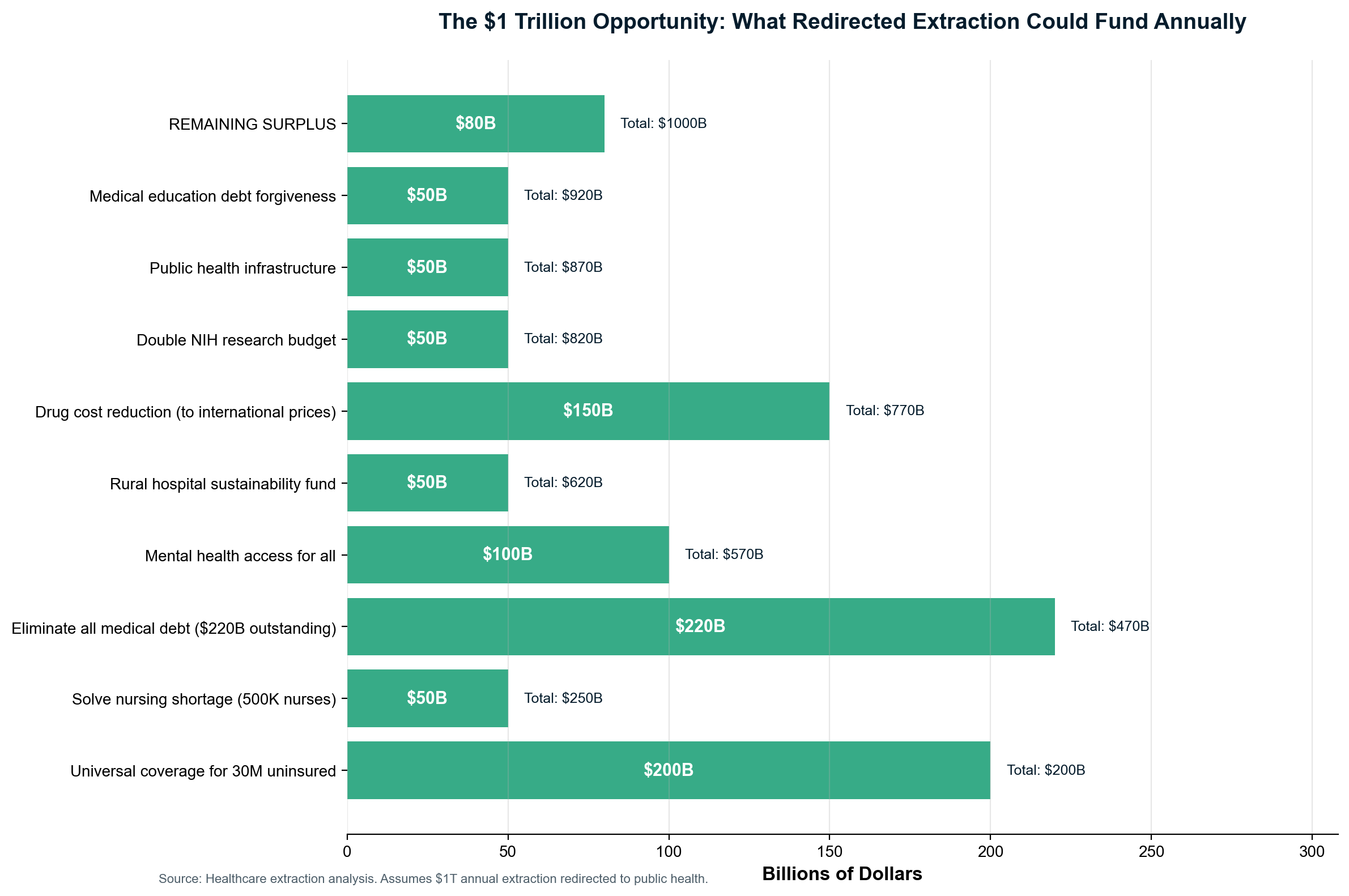

For a typical American family spending $25,000 annually on healthcare, $14,500 goes to extraction layers while only $10,500 funds actual medical care

The flow pattern demonstrates how every healthcare dollar encounters multiple extraction points before reaching care delivery. Insurance companies extract their margin, hospitals add facility fees and supply chain waste, PBMs manipulate drug pricing, administrative systems consume resources for bureaucratic complexity, and stock markets capitalize future extraction into immediate shareholder wealth. The cumulative effect removes $1.8-2.4 trillion annually from America's $5.3 trillion healthcare economy—money that could provide universal coverage with superior outcomes if redirected from extraction to care delivery.

This chapter establishes the foundation for sector-level analysis that follows: American healthcare's fundamental problem is not insufficient funding but systematic extraction that treats essential human services as wealth transfer opportunities for corporate shareholders, private equity investors, and administrative intermediaries who contribute nothing to healing while capturing enormous resources from patients facing medical necessity.

Chapter 2: Sector-Level Cash Flows

The sector-by-sector financial analysis exposes how extraction mechanisms operate within each major healthcare industry segment, revealing sophisticated profit optimization systems disguised as patient care infrastructure. Each sector has developed specialized extraction methods while maintaining plausible appearance of serving patients, but forensic investigation of cash flows proves that profit maximization drives decision-making across every healthcare industry vertical.

Insurance Premium Flow: The Extraction Template

The insurance premium dollar represents the most transparent extraction mechanism due to Medical Loss Ratio reporting that reveals exactly where patient payments go before any care occurs. Every premium dollar follows predetermined extraction pathways regardless of patient health outcomes, creating systematic wealth transfer from medical necessity to shareholder returns.

UnitedHealth Group's 2024 performance demonstrates systematic extraction across market segments. The company generated $400.3 billion in revenue while maintaining strategic MLR compliance that maximized absolute profit extraction:

Market Segment Extraction Rates

- Medicare Advantage: 10% MLR extraction generating $1,655 per enrollee in absolute profits

- Individual ACA market: 15% extraction at $987 per enrollee

- Small group: 12% extraction at $846 per enrollee

- Large group: 15% extraction at $1,200+ per enrollee [19]

The MLR system creates perverse incentives because larger denominators yield higher absolute profits even with fixed percentages. When UnitedHealth doubles medical spending in a market segment, it doubles absolute profit extraction while maintaining regulatory compliance. This explains insurer support for expensive medical interventions while blocking prevention: complex treatments grow revenue bases while prevention reduces them.

The Stock Buyback Wealth Transfer Pipeline

UnitedHealth's $42 billion in stock repurchases between 2018-2024 represents systematic conversion of patient premiums into shareholder cash extraction. [20] Each buyback reduces share count, increasing earnings per share and driving stock appreciation while removing capital that could have reduced premiums or improved care delivery. The mechanism creates wealth concentration where shareholders capture value that patients fund but never access.

Executive compensation alignment ensures extraction efficiency. CEO Andrew Witty's $26.3 million 2024 compensation included $21.5 million (82%) in stock awards, creating direct personal incentives to maximize stock price appreciation through extraction optimization rather than patient care improvement. [21] When denial rates and cost-cutting improve quarterly earnings, executive wealth increases correspondingly through stock appreciation funded by patient premiums.

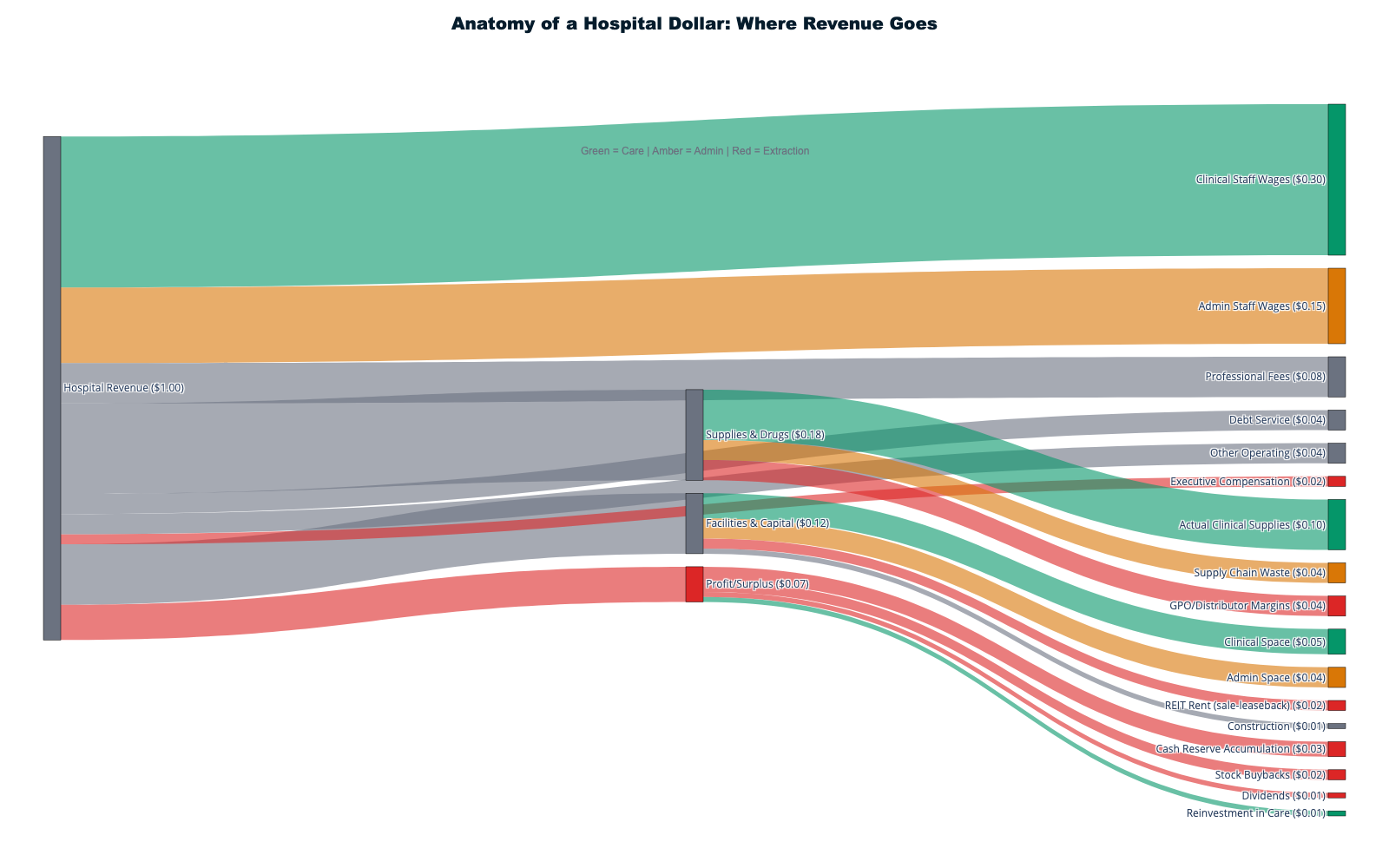

Hospital Revenue Flow: Facility Fee Arbitrage and Supply Chain Extraction

Hospital systems consume $1.634 trillion annually while operating multiple extraction mechanisms that obscure actual care delivery costs versus financial engineering. [1] Private equity involvement demonstrates pure extraction: firms load hospital systems with debt, extract dividends through operational cuts, and exit through sales or bankruptcy when debt service exceeds capacity.

Facility Fee Arbitrage: The Ownership Premium

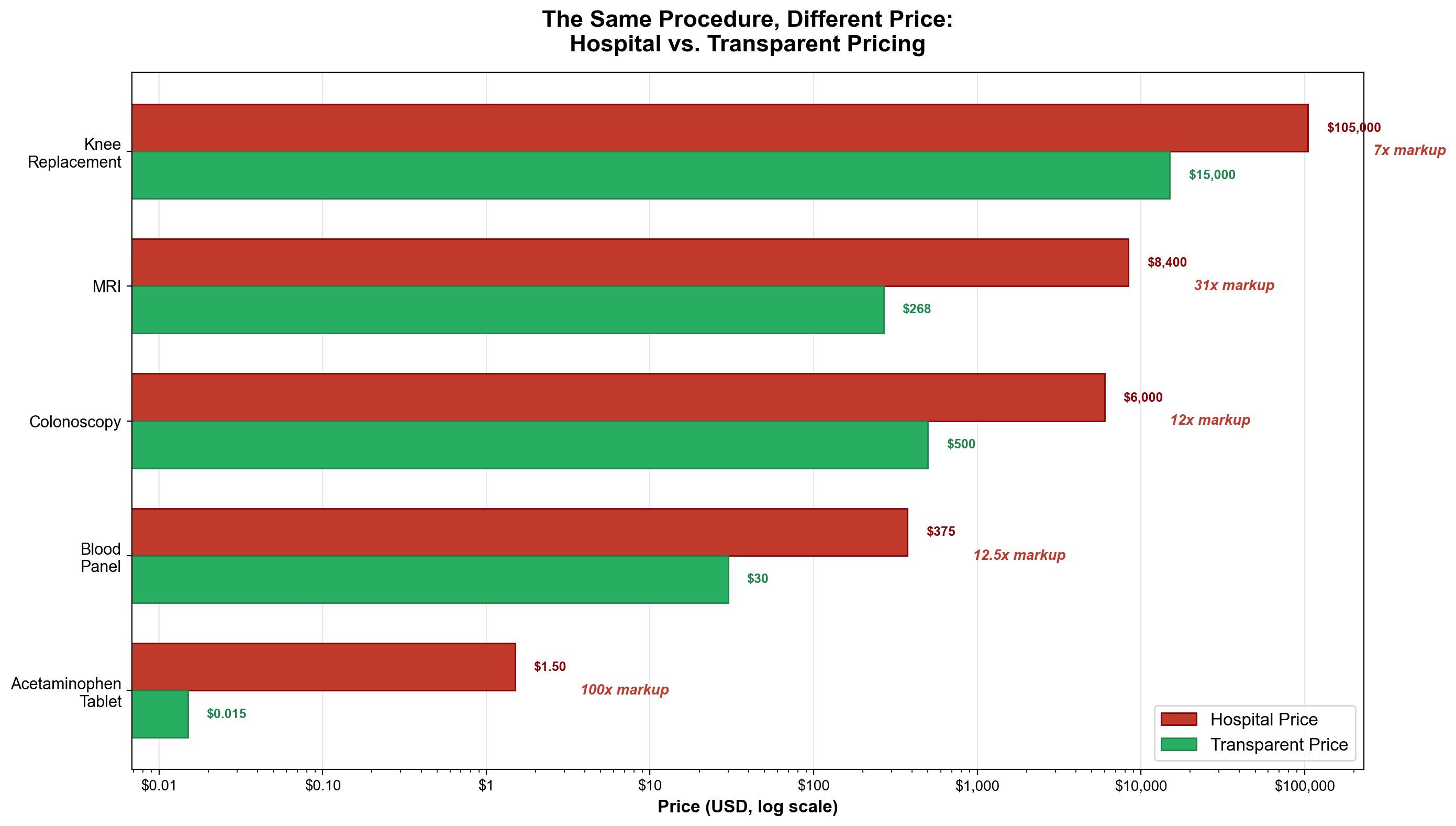

Hospital-owned practices charge systematic markups purely from ownership structure rather than service improvement. The same primary care visit costs $116 at independent physician offices but $217 at hospital-owned facilities—an 87% markup flowing to hospital profits rather than enhanced care. [22] Specialist visits face similar extraction, with hospital-owned providers adding $96 in facility fees to routine pediatric wellness visits that identical services at independent practices provide without additional charges.

Supply Chain Waste as Systematic Extraction

Hospital supply chain "inefficiencies" represent organized wealth transfer to vendor networks rather than operational failures. The documented $12.1 million average waste per hospital totals $76.2 billion annually across 6,300 hospitals—4.7% of total hospital revenue flowing to vendor profits rather than patient care. [23] This waste includes inventory management fees, distribution markups, technology licensing, and consulting services that benefit supplier companies while adding zero clinical value.

HCA Healthcare exemplifies hospital financial engineering through leveraged extraction models. The company generates $70.6 billion in revenue with 8.2% profit margins while maintaining $10 billion stock buyback programs. [24] HCA emerged from KKR's 2006 leveraged buyout and continues prioritizing shareholder returns through debt-financed extraction that constrains clinical investment while maximizing financial performance.

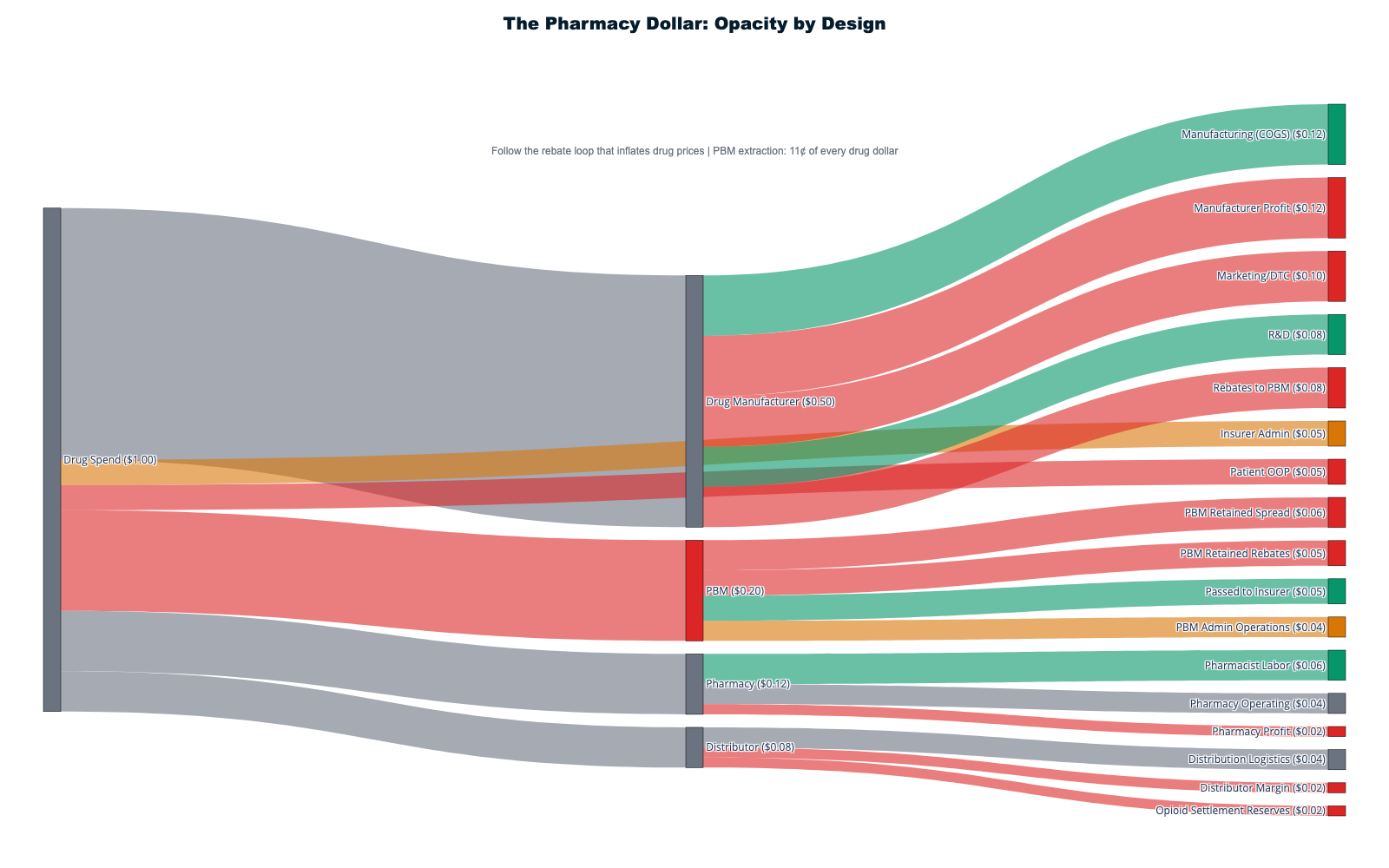

Pharmaceutical Complex: PBM Vertical Integration and Patent Manipulation

The $467 billion prescription drug market operates through the most sophisticated extraction mechanisms in healthcare, combining vertical integration, market manipulation, and regulatory capture to inflate costs while capturing enormous profits at multiple transaction points. [1]

The Vertical Integration Extraction Model

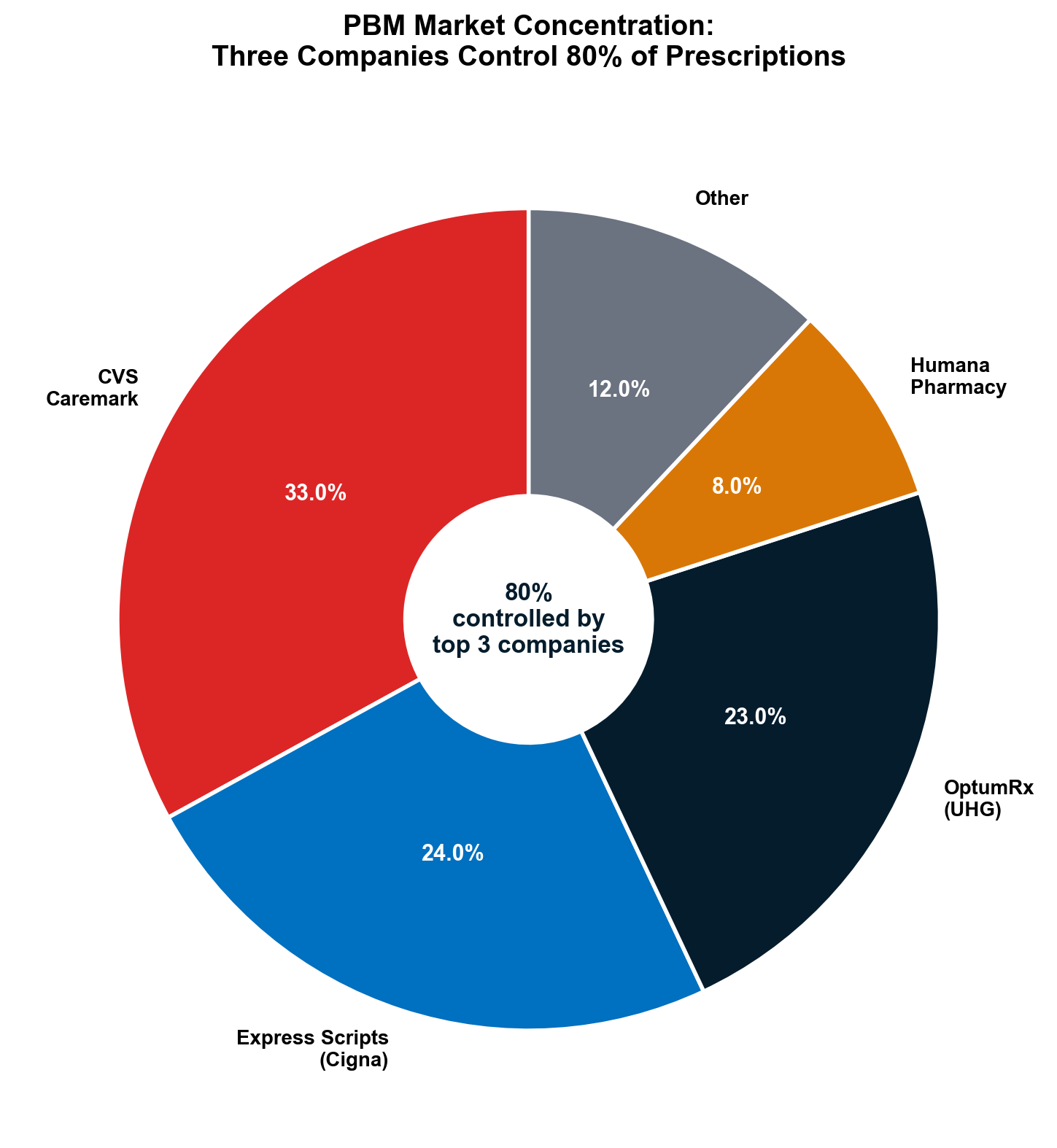

Pharmacy Benefit Managers control 80% of prescription claims while owning pharmacy chains, insurance companies, and data analytics firms. [25] CVS-Aetna's $69 billion vertical integration merger exemplifies systematic extraction: CVS operates the pharmacy, Aetna provides insurance coverage, and CVS Caremark serves as PBM—enabling profit capture at every transaction level while eliminating external competition.

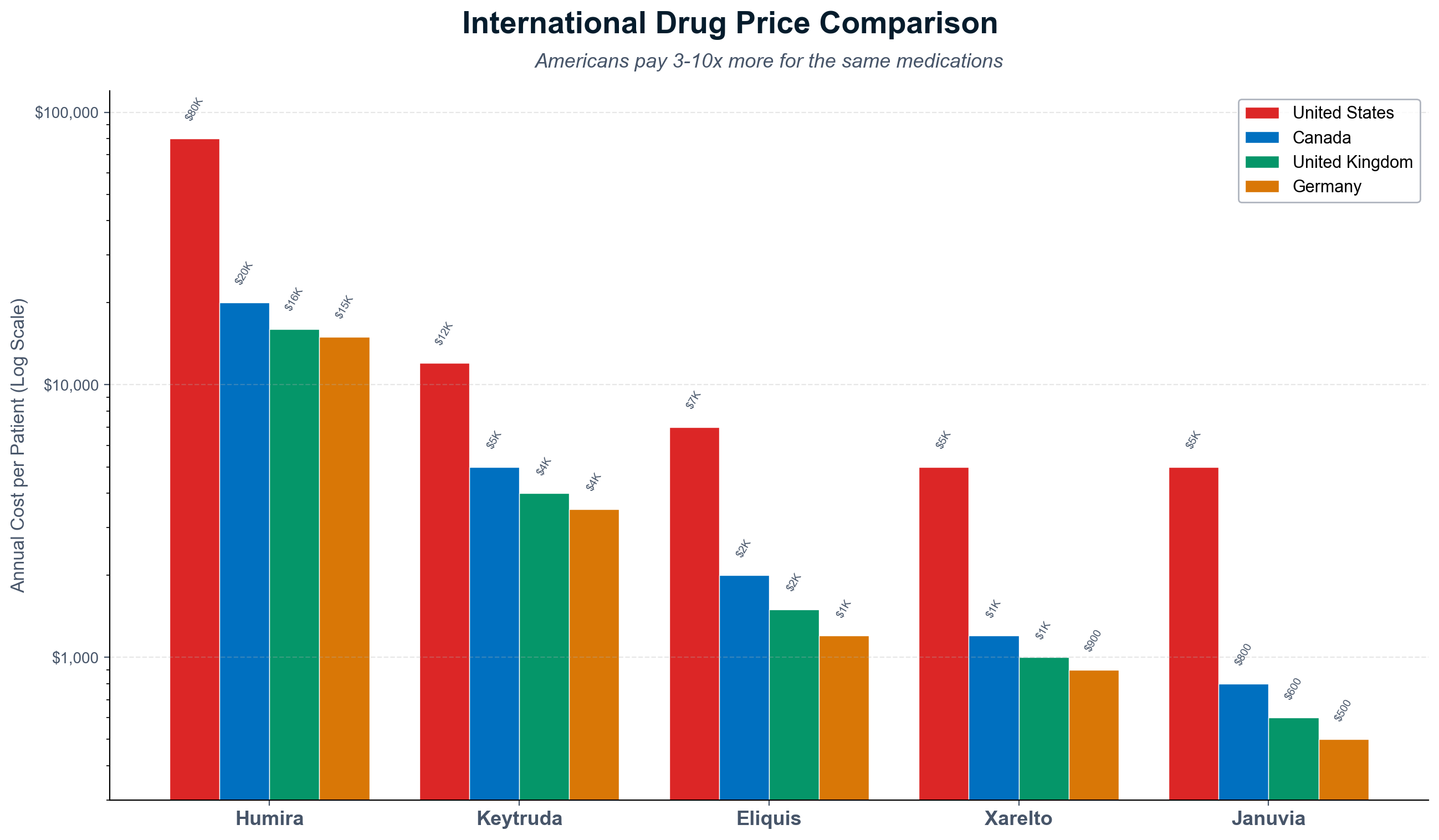

The insulin price inflation from $21 to $274+ per vial demonstrates integrated extraction mechanisms. PBMs created "rebate walls" blocking lower-cost insulin to maintain their "addiction to rebates," forcing diabetic patients to pay inflated prices while PBMs collected billions in hidden rebates that patients never received. [26] The 1,200% price increase occurred through PBM market manipulation rather than manufacturing cost increases or medical improvements.

Patent Evergreening: Artificial Monopoly Extension

Pharmaceutical companies extend drug monopolies an average of six years beyond original 20-year protection through secondary patent abuse. 70% of top-selling drugs use patents on formulation changes, delivery mechanisms, and minor modifications to block generic competition. [27] Humira maintained 21 years of exclusivity through 130+ secondary patents, generating over $200 billion in monopoly profits that would have faced generic competition under normal patent expiration.

This patent manipulation affects the entire $467 billion pharmaceutical market by establishing precedent for monopoly extension across all major medications. The system socializes research costs through government funding while privatizing profits through artificial monopoly protection that prevents competitive pricing.

Administrative Ecosystem: The $1 Trillion Shadow Economy

Healthcare administration has evolved into America's largest artificial industry, employing 12-15 million workers consuming over $1 trillion annually in wages to navigate complexity that exists purely for extraction purposes rather than clinical necessity. [28] This shadow economy demonstrates how extraction creates employment in economically destructive activities while presenting job creation as economic benefit.

Revenue Cycle Management Industrial Complex

The RCM industry employs 208,000+ workers to monetize healthcare's administrative complexity, generating over $40 billion annually by charging healthcare providers percentage fees for navigating billing dysfunction that these same companies help perpetuate. [29] R1 RCM exemplifies international extraction through 30,000+ workers across India and the Philippines earning $15,000-25,000 annually compared to $55,000+ for equivalent US positions—creating arbitrage opportunities that fund corporate profits while maintaining patient cost burdens.

Technology Infrastructure Designed for Extraction

Health IT companies employ 85,500+ workers developing systems that prioritize billing optimization over clinical efficiency. Epic Systems, Oracle Health, and athenahealth generate $8.1 billion annually in wages for workers building administrative infrastructure unnecessary under simplified payment systems. [30] These companies represent massive technological talent misallocation toward economically destructive purposes rather than clinical advancement.

Prior Authorization: The Denial Industry

Companies like eviCore exist purely to deny medically necessary care through bureaucratic obstruction, employing 30,500+ workers whose primary function involves preventing patients from receiving appropriate treatment. [31] This industry generates $1.8 billion annually in wages for systematic care denial that produces zero clinical benefits while forcing physicians to spend 14+ hours weekly justifying medically obvious decisions.

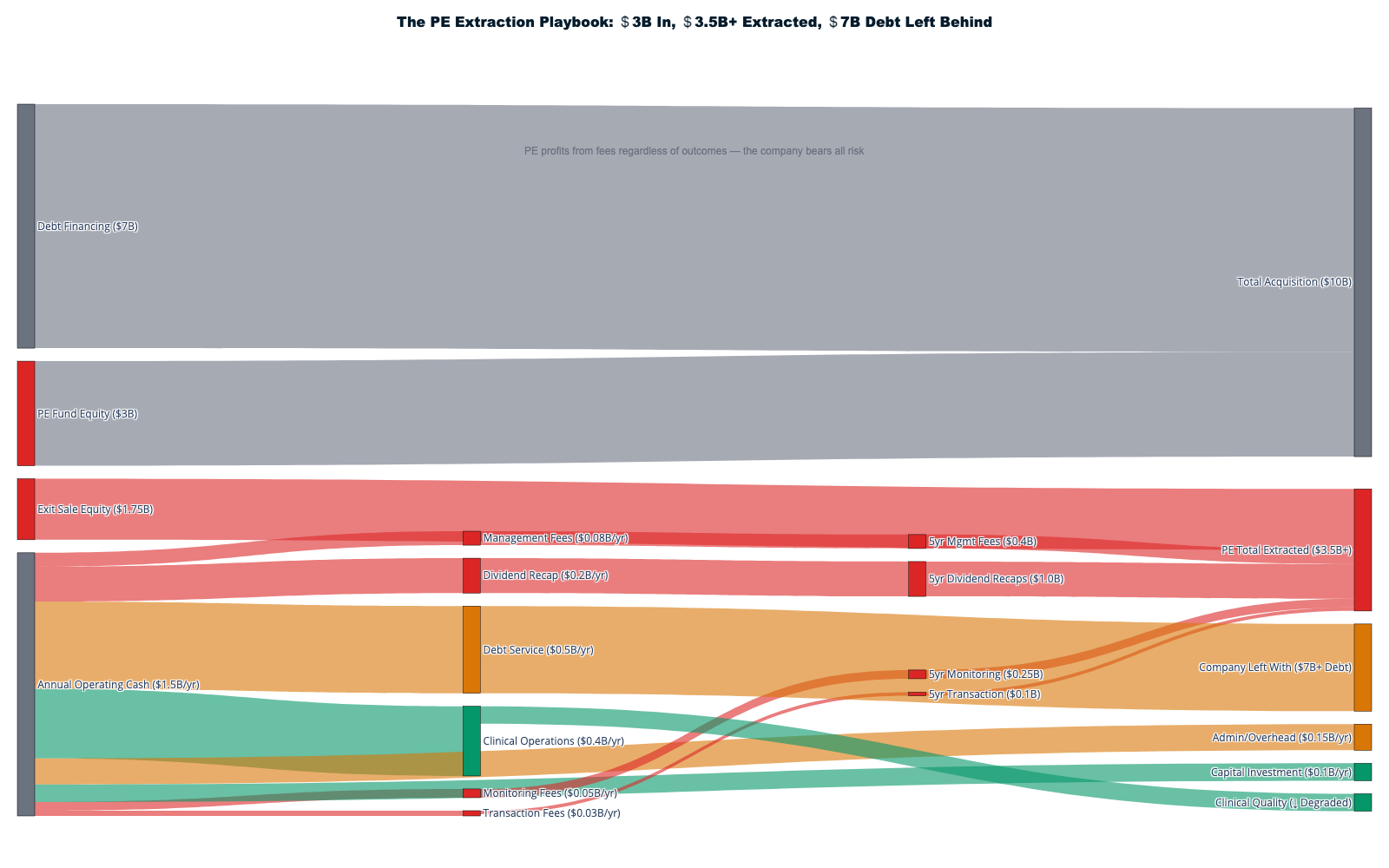

Private Equity Healthcare Extraction

Private equity firms have systematically acquired healthcare companies to optimize extraction through financial engineering that prioritizes shareholder returns over patient outcomes. The PE model creates value through debt loading, cost-cutting, and market positioning that maximizes valuation multiples at exit rather than care delivery improvement.

The Leveraged Extraction Model

KKR's 2006 HCA Healthcare buyout established the template: acquire healthcare companies for $33 billion, load with debt, extract cash through operational cuts and financial engineering, optimize metrics for public market exit. [32] The model treats healthcare facilities as financial assets designed for stock market optimization rather than community health improvement.

Emergency physician staffing demonstrates extraction through artificial scarcity. Envision Healthcare faced bankruptcy after KKR loaded the company with $7.2 billion in acquisition debt requiring $400-500 million annual debt service from $8 billion revenue. [33] The company cut physician staffing, increased patient volumes, and maximized billing complexity to service debt payments while clinical care quality declined. When debt service exceeded operational capacity, KKR walked away while communities lost physician coverage.

International Comparison: Peer Country Efficiency

Single-payer and regulated multi-payer systems achieve superior health outcomes while avoiding American-style extraction through structural design that prioritizes care delivery over wealth accumulation.

Administrative Efficiency Models

- Canada: 2% administrative overhead achieving universal coverage

- United Kingdom: NHS operates at 2% administrative costs with superior outcomes

- Germany: 4% administrative overhead with insurance-based universal system

- United States: 7.5-8% administrative overhead with partial coverage [34]

The $186+ billion annual administrative differential represents pure extraction that could fund universal coverage while improving population health outcomes. Peer countries prove that healthcare intermediation, pharmaceutical pricing, and administrative coordination can operate efficiently when designed for patient service rather than profit maximization.

What Peer Countries Don't Have

- Private insurance stock market wealth creation

- Pharmacy benefit manager intermediation

- Hospital facility fee arbitrage

- Patent evergreening protection

- Prior authorization denial industries

- Revenue cycle management complexity

Each extraction mechanism represents deliberate policy choice rather than economic necessity, demonstrating that American healthcare dysfunction serves corporate profits while peer countries prioritize population health through rational system design.

The sector-level analysis reveals systematic extraction optimization across every healthcare industry segment, with cumulative mechanisms removing 58% of healthcare spending from care delivery. Each sector maintains sophisticated profit maximization while preserving appearance of patient service, creating the most expensive healthcare system globally while achieving outcomes inferior to countries spending half as much per capita through rational organization prioritizing healing over wealth extraction.

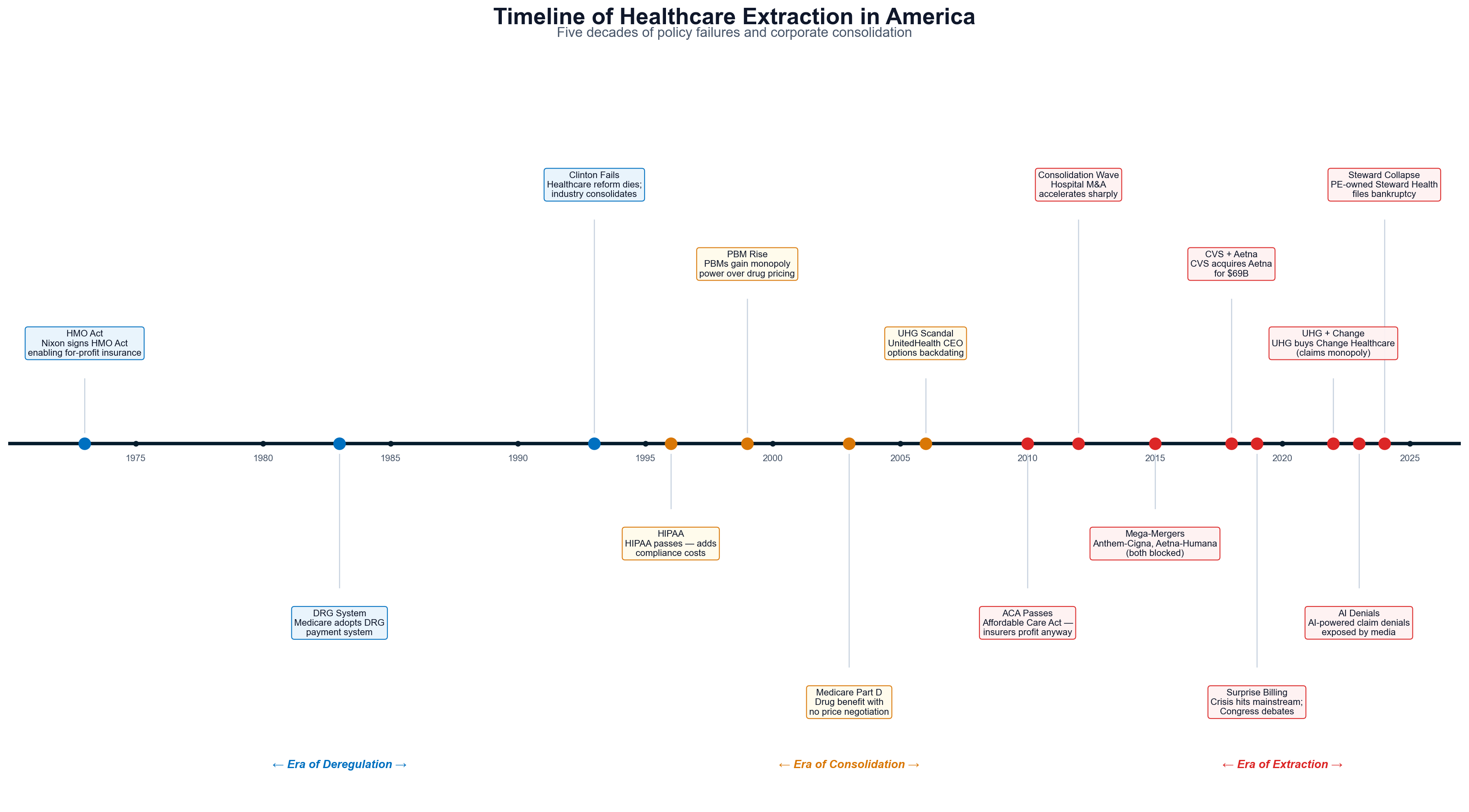

Chapter 3: The Extraction Timeline — How We Got Here (1947-Present)

The transformation of American healthcare from patient-centered service into systematic wealth extraction required 75+ years of legislative, regulatory, and judicial decisions that consistently prioritized corporate profits over patient welfare. This timeline reveals that every major extraction mechanism was enabled by specific policy choices rather than natural market evolution. The chapters that follow (4-14) examine each mechanism in forensic detail; this chapter provides the chronological roadmap showing how they were constructed.

Foundation Era (1943-1972): Establishing Corporate Control

The foundation for healthcare extraction was laid through seemingly technical policy decisions that shifted control from patients and providers to employers and intermediaries. The single most consequential decision was not a law but an administrative ruling.

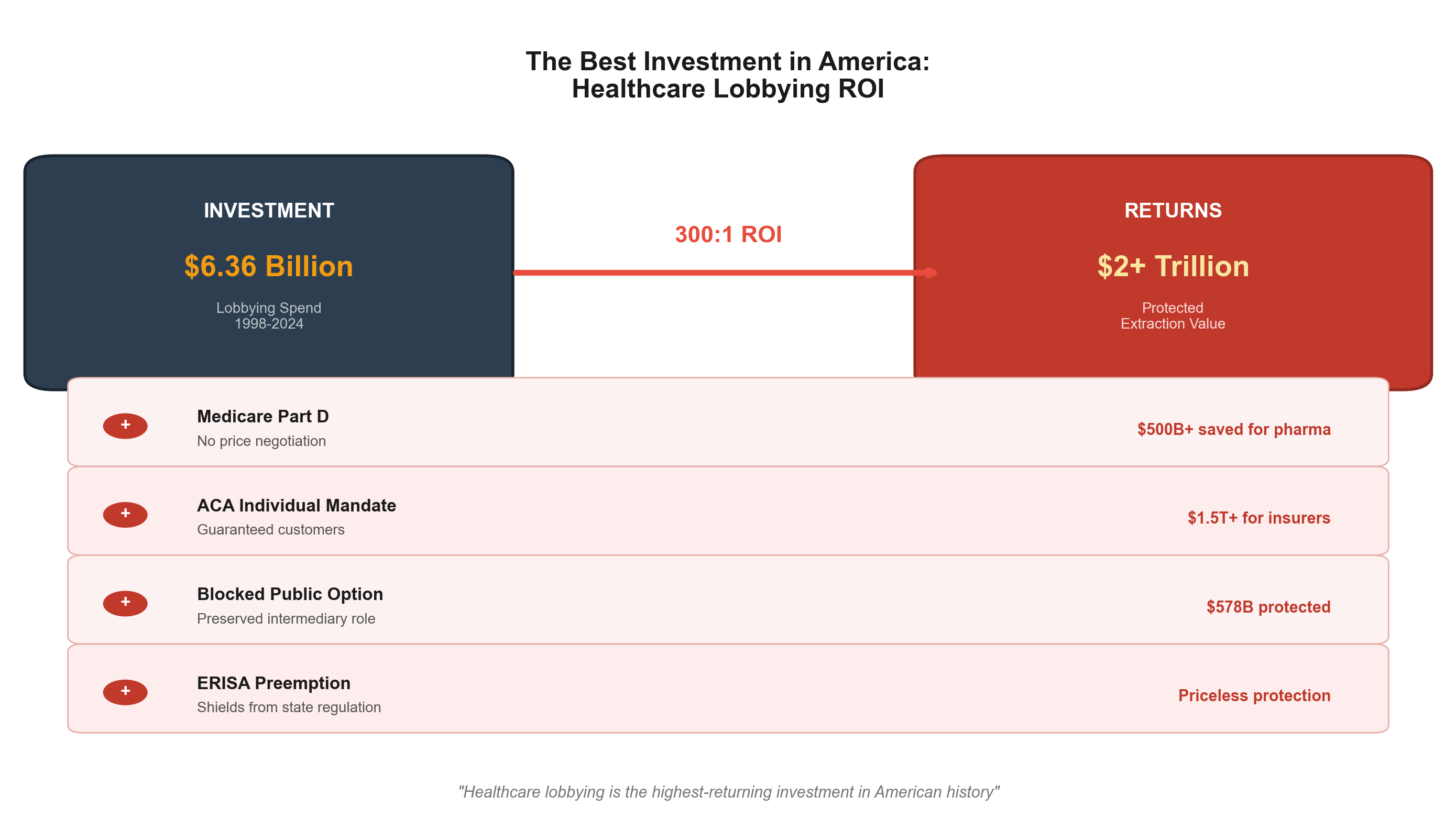

IRS Tax Exemption Ruling (1943, codified as IRC §106 in 1954): During World War II, with wages frozen under price controls, the IRS ruled that employer-paid health benefits were not taxable employee income — making employer-provided insurance uniquely tax-advantaged compared to individually purchased coverage. This administrative decision, later permanently codified in Internal Revenue Code §106, was the critical mechanism that locked in the private insurance model: it made employer-sponsored coverage $3,000-5,000 cheaper per family than equivalent individual policies (in today's dollars), ensuring that health insurance would be distributed through employers rather than through government programs or individual markets. The tax exclusion is now worth over $400 billion annually in forgone federal revenue — the largest single tax expenditure in the federal budget — and remains the structural foundation of America's employer-based insurance system. [37] [229]

The Truman Defeat (1945-1950): President Truman's 1945 proposal for national health insurance — a comprehensive plan that would have provided universal coverage through a single government-administered system — was defeated by the American Medical Association's unprecedented lobbying campaign. The AMA assessed its members an extra $25 each, hired the political consulting firm Whitaker and Baxter, and spent $1.5 million on lobbying efforts — the most expensive lobbying campaign in American history at that time. [230] The campaign successfully branded Truman's proposal as "socialized medicine," ensuring that private insurance would become the dominant model rather than a government program. This defeat represented the last serious attempt at universal coverage for two decades and cemented the employer-based private insurance system as the American default.

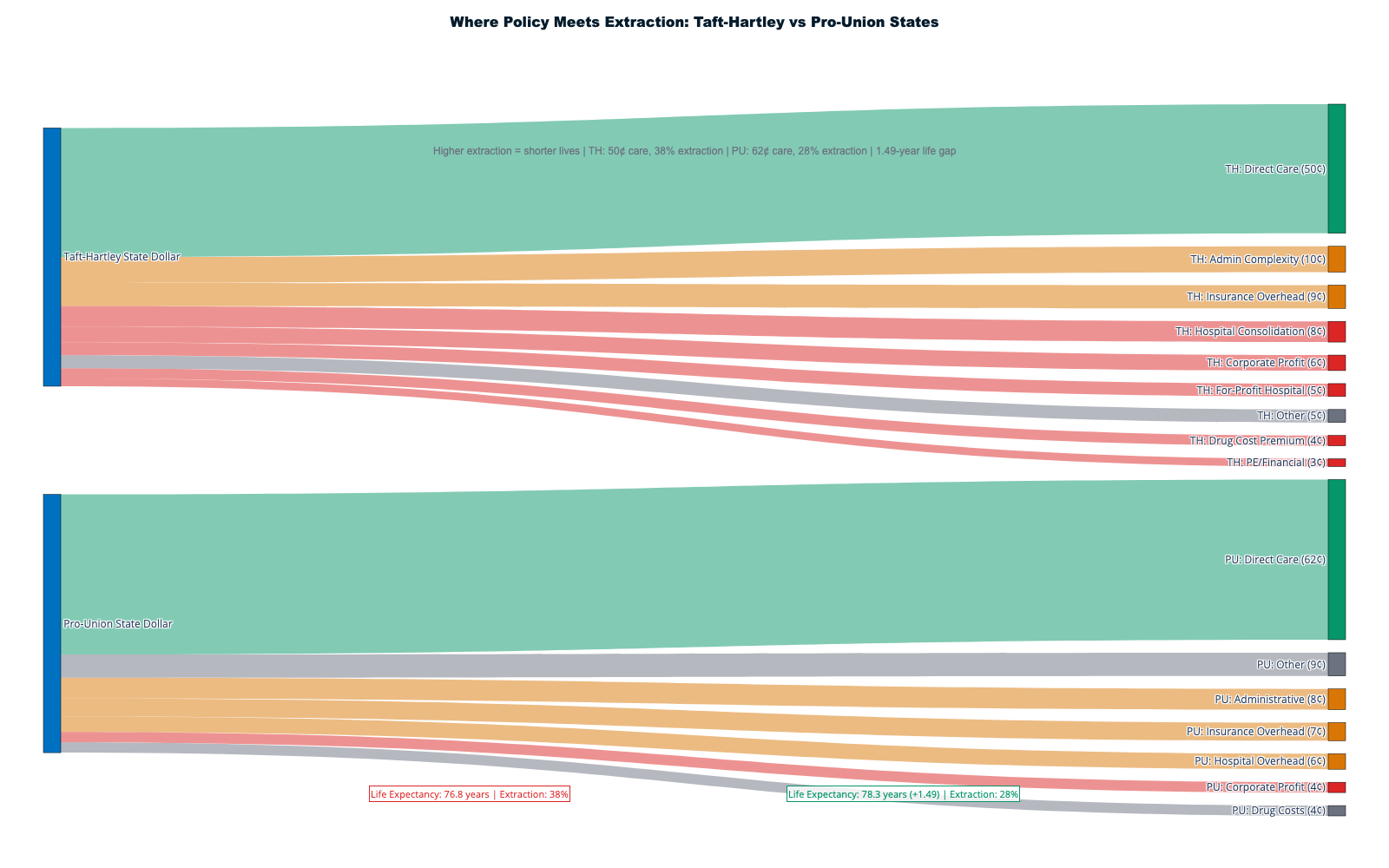

Taft-Hartley Act (1947): Severely restricted union collective bargaining while exempting employer-provided health benefits, shifting healthcare from worker right to employer privilege. Combined with the 1943 tax ruling, Taft-Hartley channeled healthcare through the employer-insurance nexus rather than collective worker power or government provision. Union members today pay 28% lower premiums, suggesting Taft-Hartley costs non-union workers $3,000-4,000 annually. [35] [36]

Medicare/Medicaid Creation (1965): Provided massive new revenue streams while embedding extraction from inception. "Reasonable cost" reimbursement gave providers virtual blank checks. Initial spending of $4.5 billion in 1966 grew 5,930% to $2.7 trillion by 2024. [38]

Market Mechanisms Era (1973-1992): Corporate Management Expansion

This period introduced for-profit corporate management to healthcare delivery while creating regulatory gaps that enabled extraction without accountability.

HMO Act (1973): Provided federal funding and regulatory exemptions for health maintenance organizations. By the late 1990s, 80% were for-profit with only 68% of premiums reaching medical care. [39] (See Chapter 7 for detailed insurance financial engineering analysis.)

ERISA Preemption (1974): Created regulatory gaps protecting self-insured plans covering 93.6 million workers from state oversight, enabling systematic extraction with minimal patient remedy. [40] (See Chapter 14 for ERISA's role in regulatory capture.)

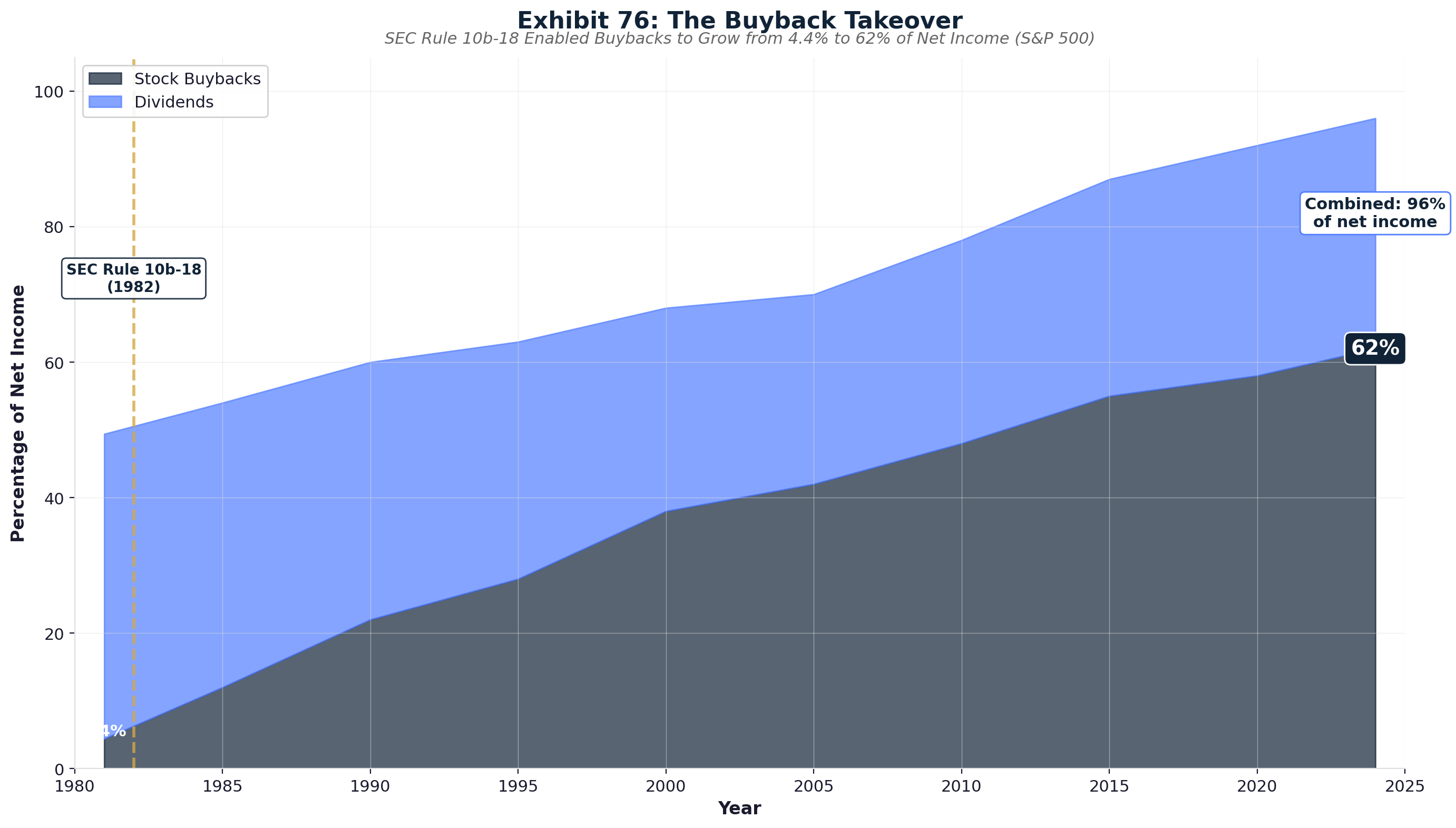

SEC Rule 10b-18 (1982): Legalized stock buybacks, enabling corporations to manipulate stock prices through open-market repurchases. Healthcare companies now distribute 96% of net income to shareholders, compared to 4.4% in 1981. (See Chapter 8 for the full stock market extraction pipeline.)

Residency Cap (1997): The Balanced Budget Act capped Medicare-funded residency slots at 1996 levels, artificially restricting physician supply for 28+ years. [41] (See Chapter 5 for how physician scarcity drives hospital consolidation.)

Financial Engineering Era (2003-2009): Wall Street Integration

This period embedded Wall Street profit motives directly into healthcare delivery through legislative capture and private equity expansion.

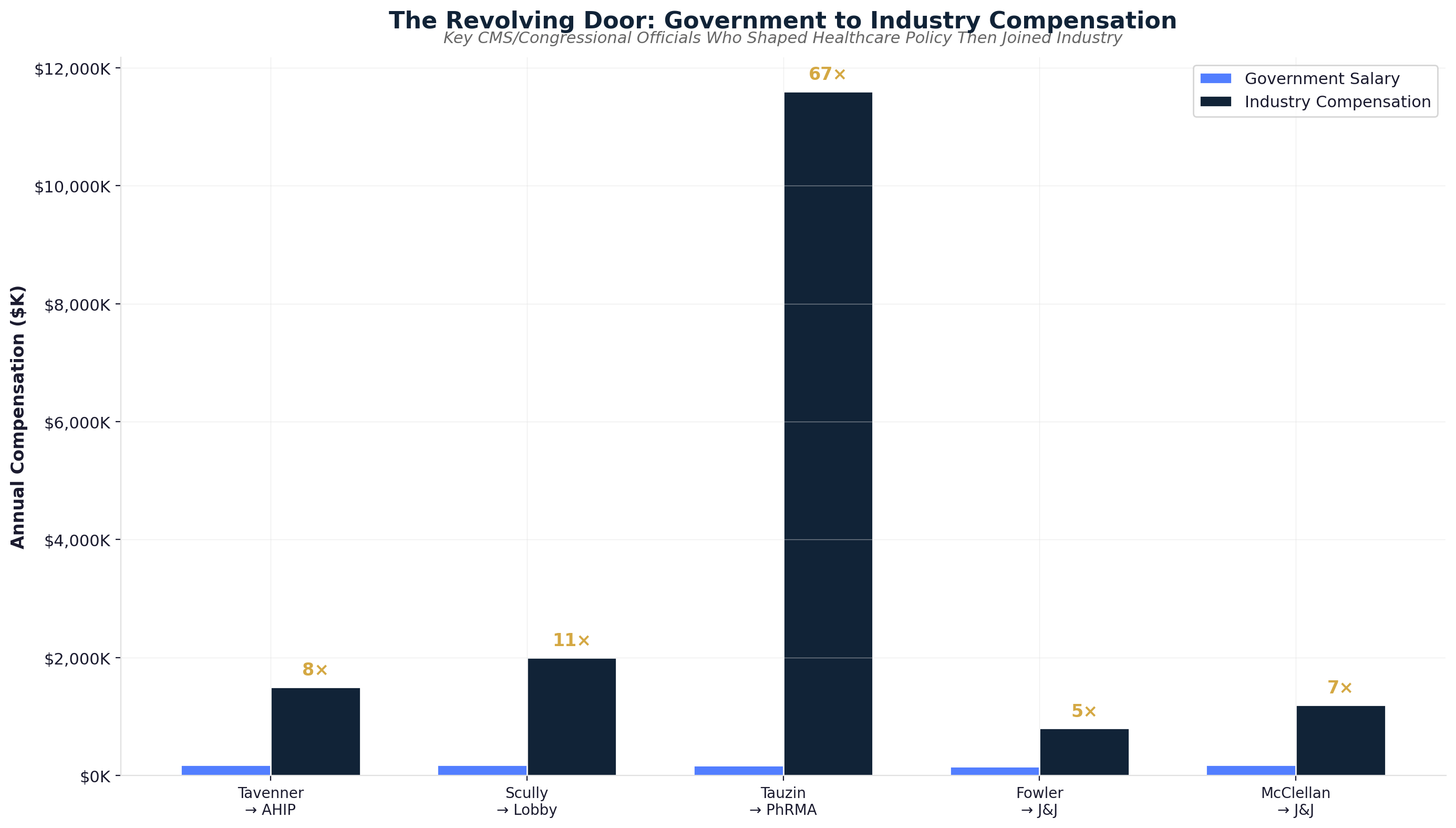

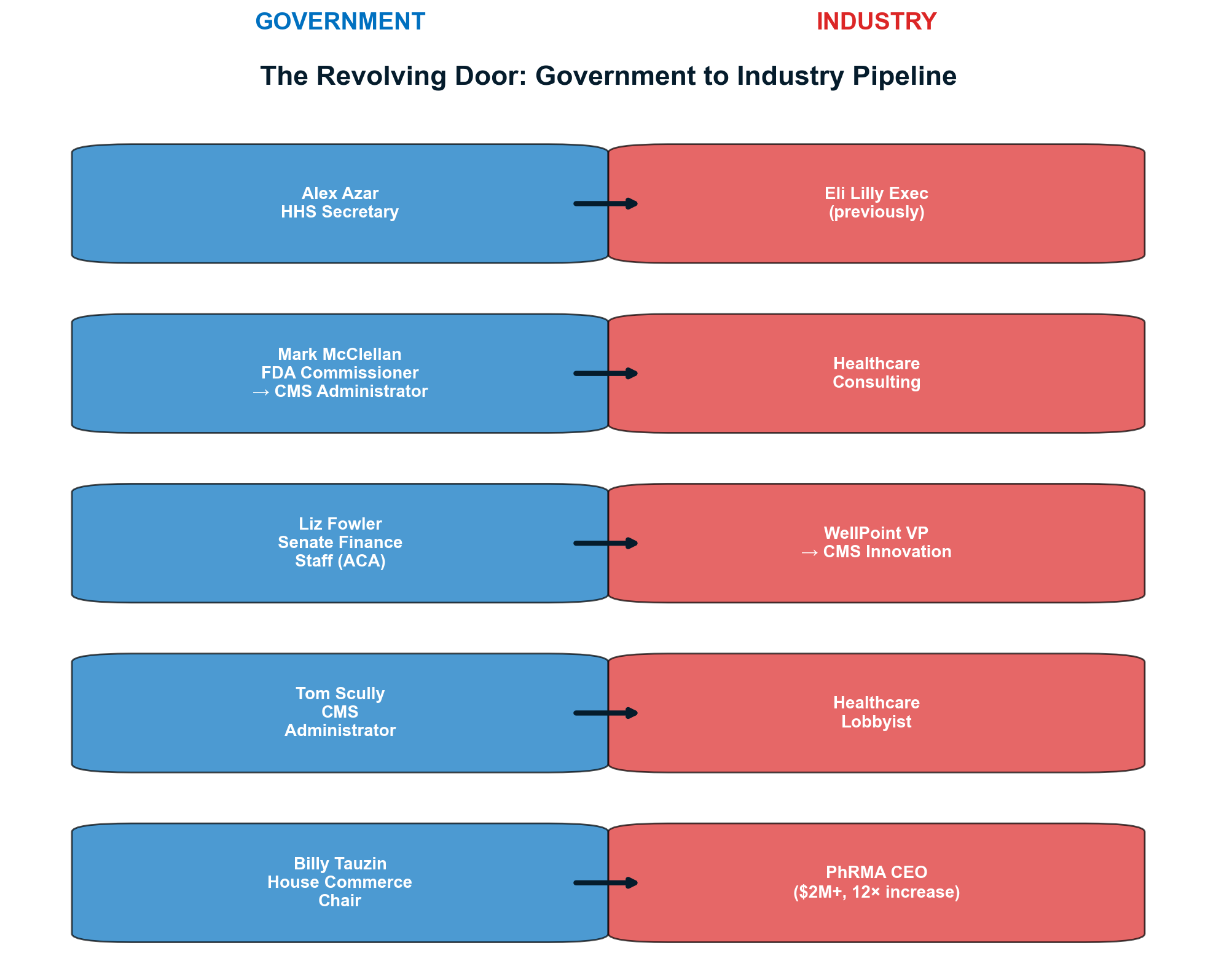

Medicare Modernization Act (2003): The Medicare Part D prescription drug benefit included explicit prohibition on government price negotiation — the most successful pharmaceutical industry lobbying victory in history. [42] The revolving door was immediate: Congressman Billy Tauzin became PhRMA president at $11.6 million annually; CMS Administrator Thomas Scully joined five affected companies; 15+ officials involved joined pharmaceutical positions. (See Chapter 9 for pharmaceutical extraction mechanisms and Chapter 14 for the full revolving door analysis.)

HCA Leveraged Buyout (2006): KKR, Bain Capital, and Merrill Lynch's $33 billion HCA acquisition established the PE healthcare extraction model: acquire, load with debt, cut costs, extract dividends, exit before consequences emerge. [44] (See Chapter 10 for the complete private equity playbook and Chapter 5 for HCA's ongoing extraction.)

ACA Era (2010-Present): Extraction Through "Reform"

The Affordable Care Act period demonstrates how well-intentioned reform became extraction expansion through industry influence.

Individual Mandate (2010-2017): Required Americans to purchase private insurance, creating guaranteed revenue streams. Combined with Medicaid expansion ($126B annually) and marketplace subsidies ($92B in FY2023), government guaranteed $218 billion in annual revenue to private insurers. [45] Health insurer stocks increased 1,032% from ACA enactment through 2024, compared to 251% S&P 500 growth. [46] (See Chapter 7 for MLR gaming and Chapter 8 for the stock market amplification effect.)

Essential Health Benefits: Required insurance processing for routine transactions like $4 prescriptions and $150 office visits, creating 7.2 billion annual claims generating $86-108 billion in administrative overhead on predictable needs. [47] The pharmaceutical industry's $150 million pro-ACA campaign secured continued protection from price negotiation. [48]

Peak Extraction Era (2017-Present): Consolidation and Resistance

Vertical Integration Mega-Mergers: CVS-Aetna ($69B), Cigna-Express Scripts ($67B), and UnitedHealth-Change Healthcare ($13B) consolidated pharmacy, PBM, insurance, and claims processing under single ownership, eliminating competitive pressure. [49] (See Chapter 4 for the full vertical integration analysis.)

Public Awakening (2024): The December 4, 2024 assassination of UnitedHealthcare CEO Brian Thompson crystallized decades of public anger, triggering unprecedented discourse about extraction mechanisms. [50] Regulatory investigations revealed systematic fraud across Medicare Advantage, PBM manipulation, and hospital pricing. [51]

Timeline Analysis: Systematic Policy Construction

The 75-year timeline reveals acceleration through each phase: Foundation era (1947-1972, 25 years), Market mechanisms (1973-1992, 20 years), Financial engineering (1993-2009, 16 years), Peak extraction (2010-present, 14+ years). Each phase built upon previous extraction mechanisms while shortening implementation timelines.

The crisis response pattern is consistent: every healthcare "crisis" produces "reforms" that strengthen extraction. Medicare cost crisis → DRG gaming; drug cost crisis → Part D profit protection; access crisis → ACA industry subsidies. What was systematically blocked tells an equally important story: single-payer proposals (1948, 1965, 1973, 1994, 2009, 2016), government pharmaceutical manufacturing, Medicare negotiation authority (until 2022, limited scope), and public option insurance.

The evidence demands a clear conclusion: current healthcare dysfunction represents systematic policy choice rather than economic inevitability. Every extraction mechanism was enabled by specific government decisions that could be reversed through different political choices. The detailed analyses in Chapters 4-14 document precisely how each mechanism operates and what reforms could dismantle it.

Chapters 4-8: How American Healthcare Systematically Extracts Wealth from Patient Care

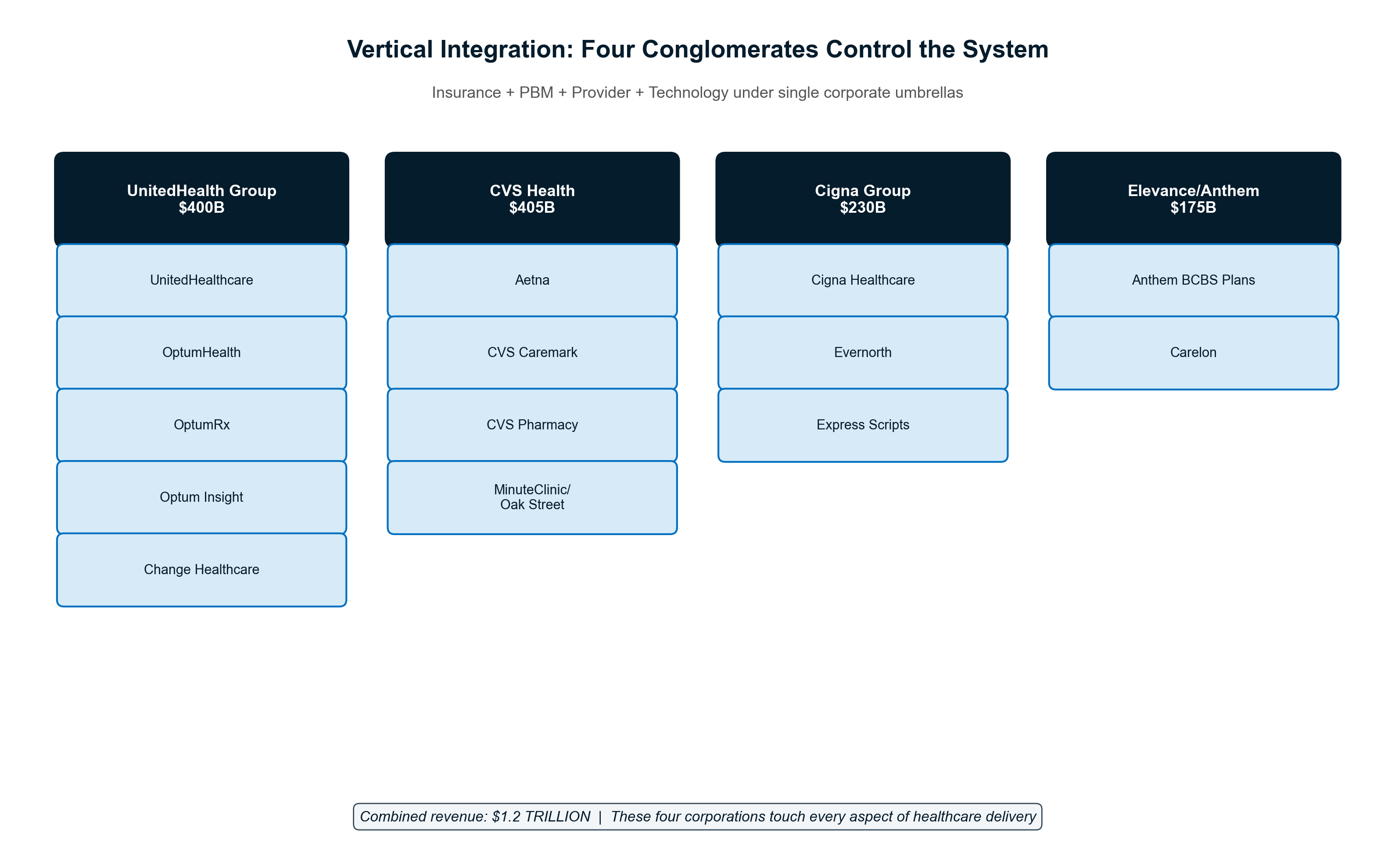

Chapter 4: Vertical Integration — The Conglomerate Machine

Modern healthcare extraction reaches its apotheosis through vertical integration, where massive conglomerates control every touchpoint with patients to extract maximum value while obscuring costs through intercompany transfers. UnitedHealth Group exemplifies this model: a $400.3 billion empire that demonstrates how owning the entire healthcare value chain enables systematic wealth extraction from patients and taxpayers at unprecedented scale.

The UnitedHealth Octopus: Eight Tentacles, One Extraction Purpose

UnitedHealth Group has constructed the most comprehensive vertical integration in American healthcare history, operating simultaneously as insurer, provider, pharmacy benefit manager, data processor, and claims administrator. The company's 2024 revenue of $400.3 billion—an 8% increase from $371.6 billion in 2023—flows through multiple extraction layers before any dollar reaches actual patient care [1]. This integration creates artificial internal markets where the company profits multiple times from the same patient interaction while eliminating competitive pressures that would reduce extraction opportunities.

The corporate structure reveals the extraction strategy with mathematical precision. UnitedHealthcare collects $281.4 billion in premium revenue while Optum generates $226.6 billion across its three divisions—Optum Health (provider services), OptumRx (pharmacy benefits), and Optum Insight (data analytics) [1]. When these divisions serve the same patients, every transaction becomes an optimization opportunity for total enterprise profit rather than competitive market dynamics.

UnitedHealthcare pays Optum Health facilities for medical services delivered to UnitedHealthcare members, with pricing controlled internally rather than by market competition. OptumRx fills prescriptions for UnitedHealthcare patients using formularies designed to maximize overall UnitedHealth profitability rather than patient cost minimization. Optum Insight monetizes the medical data generated across all these interactions, creating a fourth profit stream from the same patient encounters. The Change Healthcare acquisition—completed for $13 billion despite Department of Justice opposition—added claims processing for competitors, providing unprecedented market intelligence that enables extraction optimization [2].

This closed-loop system enables what economists call "transfer pricing"—the manipulation of internal transactions to optimize overall extraction. When UnitedHealthcare denies coverage for expensive specialty care, Optum Health providers offer alternative services that generate revenue for the same enterprise. When OptumRx excludes lower-cost medications from formularies, patients pay higher prices that benefit the broader UnitedHealth ecosystem through manufacturer rebates and pharmacy margins. These coordinated decisions appear independent but function as systematic extraction optimization across the integrated enterprise.

CVS Health: The Pharmacy-Insurance Death Star

CVS Health represents the second major extraction archetype, combining the nation's largest pharmacy chain with Aetna insurance serving 69 million members to profit from both ends of prescription transactions while controlling patient access through formulary manipulation. The $69 billion Aetna acquisition created a closed-loop system where patients with Aetna insurance find their prescription benefits systematically steered toward CVS pharmacies through preferential copays and network restrictions [3].

The pharmacy-insurance integration demonstrates extraction through artificial scarcity creation. Patients with Aetna coverage face substantially higher copays at competing pharmacies, creating economic coercion that drives traffic to CVS locations. CVS Specialty maintains exclusive contracts for expensive chronic disease medications, forcing patients requiring life-sustaining drugs to use CVS-owned pharmacies regardless of convenience, service quality, or competitive pricing. This captive customer base generates 30-40% profit margins on specialty pharmaceuticals compared to 2-3% margins on generic drug dispensing [4].

MinuteClinic and Oak Street Health complete CVS's integration strategy by providing care delivery that generates additional extraction opportunities. Patients receive primary care from CVS-employed providers who write prescriptions filled at CVS pharmacies, with Aetna processing insurance claims for both services. Every patient touchpoint generates revenue for the same corporate entity while competitors are systematically excluded from this closed-loop economy. The company's recent announcement of a $10 billion share buyback program demonstrates how patient care revenue flows directly to shareholders rather than care improvement or access expansion [5].

The Intercompany Shell Game: Looting Through Legal Arbitrage

Vertical integration's most sophisticated extraction mechanism operates through intercompany pricing manipulation that exploits regulatory gaps in Medical Loss Ratio calculations. When UnitedHealthcare pays Optum Health $300 for services that Medicare prices at $150, only $150 may count toward MLR compliance, but the transaction still extracts $150 in excess value from the premium pool while maintaining technical regulatory compliance [6].

This shell game creates systematic incentives for cost inflation throughout integrated systems. OptumRx negotiated $12.8 billion in manufacturer rebates during 2024, ostensibly to control drug costs for UnitedHealthcare members [7]. However, these rebates often benefit the broader UnitedHealth enterprise rather than reducing patient costs. The company's recent commitment to phase out rebate retention by 2028—moving to 100% pass-through—acknowledges the extent to which current structures serve corporate profits rather than patient interests.

The Change Healthcare acquisition amplifies extraction opportunities through information asymmetry that would be illegal in other industries. By processing claims for competitors while operating its own insurance and provider networks, UnitedHealth gains unprecedented insight into market pricing, utilization patterns, and competitive strategies. This competitive intelligence enables the company to optimize its own operations while systematically disadvantaging competitors who must rely on UnitedHealth's infrastructure [2].

Market Concentration: The Oligopoly Enabler

Vertical integration succeeds as extraction strategy because it operates within highly concentrated markets that eliminate competitive pressures. The top three PBMs—Express Scripts (Cigna), CVS Caremark, and OptumRx—control 80% of prescription claims with a Herfindahl-Hirschman Index of 1,972, far above the 1,800 threshold economists consider problematic for competition [8]. This concentration enables coordinated extraction strategies that would be impossible in competitive markets.

Health insurance markets demonstrate similar concentration patterns. UnitedHealthcare serves as the largest Medicare Advantage plan with 33 million enrollees, while maintaining denial rates of 12.8%—nearly double the industry average of 6.4% and far exceeding competitors like Humana (5.8%) and Elevance (4.2%) [9]. The company's scale enables more aggressive extraction strategies while providing sufficient market power to withstand regulatory pressure and competitive challenges.

Provider market concentration amplifies integration benefits by reducing negotiating power of independent physicians and hospitals. When UnitedHealth acquires physician practices through Optum Health, these providers lose independence to negotiate rates with competing insurers. The integrated model forces providers to accept UnitedHealth's pricing terms across all lines of business, creating systematic extraction opportunities unavailable to non-integrated competitors.

Legislative Architecture: The Regulatory Capture Foundation

The current extraction system depends on legislative frameworks that explicitly enable vertical integration while preventing effective oversight. The Employee Retirement Income Security Act (ERISA) preempts state insurance regulation for employer-sponsored plans covering 152 million Americans, allowing national insurers to avoid state-level consumer protections while operating across all markets [10]. This federal preemption creates regulatory arbitrage opportunities that vertically integrated companies exploit systematically.

Certificate of Need laws in 34 states create artificial barriers to entry that protect integrated systems from competition. When UnitedHealth seeks to expand Optum Health facilities in CON states, independent competitors cannot establish competing services because regulatory approval favors established players with resources to navigate complex bureaucratic procedures. These laws function as incumbent protection mechanisms that enable extraction through reduced competition [11].

The Medicare Modernization Act's prohibition on direct government drug price negotiation—only recently modified for ten medications—created the PBM intermediary market that integrated companies now dominate. By preventing Medicare from negotiating directly with pharmaceutical manufacturers, Congress created a multi-billion-dollar extraction opportunity that companies like UnitedHealth capture through OptumRx operations [12].

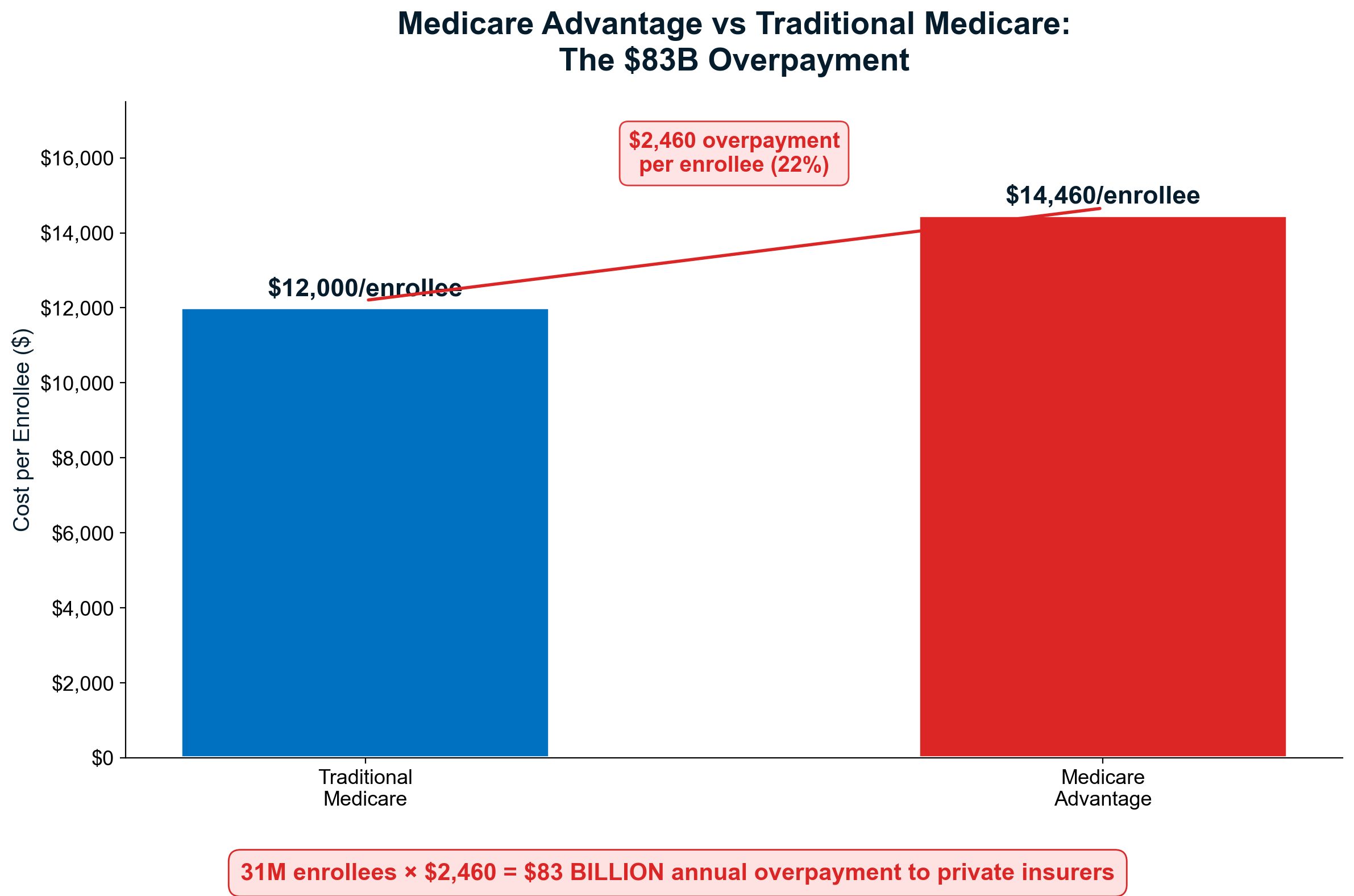

Medicare Advantage overpayments exemplify how regulation enables extraction from taxpayers. UnitedHealth's MA plans received an estimated $22 billion in federal overpayments during 2024 while maintaining the highest denial rates in the industry [13]. The company's integrated structure allows it to deny care at the insurance level while profiting from alternative services delivered through Optum Health providers, creating dual extraction opportunities from single patient encounters funded by taxpayer subsidies.

The Extraction Multiplication Effect

Vertical integration functions as an extraction multiplier that enables companies to profit 3-5 times from the same patient interaction through coordinated pricing across business lines. A diabetic patient covered by UnitedHealthcare generates insurance margin when coverage is approved, provider facility fees when care is delivered at Optum Health facilities, pharmacy markups when prescriptions are filled through OptumRx preferred networks, and data monetization when medical information is processed through Optum Insight analytics.

This multiplication effect explains why healthcare stocks have dramatically outperformed broader markets since ACA implementation. Health insurer stocks increased 1,032% from 2010-2024 compared to 251% S&P 500 growth—a 4:1 outperformance that reflects the market's recognition of integrated extraction capacity rather than care delivery excellence [14]. UnitedHealth's market capitalization expanded from $39 billion in 2010 to $265 billion in 2026, representing $226 billion in shareholder wealth creation funded entirely by patient premiums and taxpayer subsidies.

Vertical integration in healthcare represents extraction capitalism's maturation, where controlling market infrastructure becomes more profitable than delivering superior outcomes. Until policymakers address ERISA preemption, eliminate CON laws, and break up integrated oligopolies, vertical integration will continue expanding as healthcare's dominant extraction mechanism—prioritizing shareholder returns over patient welfare with mathematical precision and systemic brutality.

Chapter 5: Hospital Consolidation & the For-Profit Machine

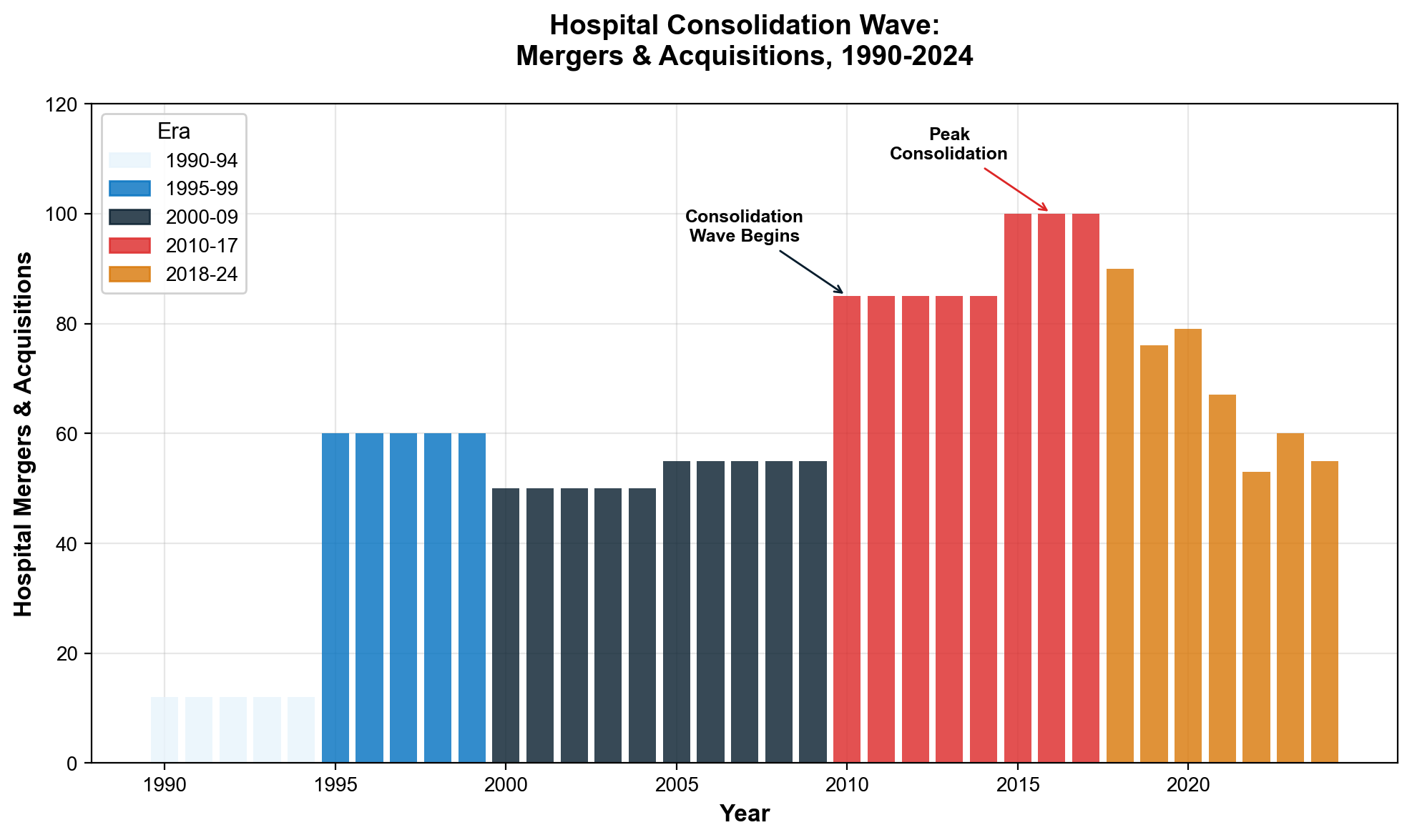

Hospital consolidation has transformed American healthcare delivery through systematic merger activity that prioritizes extraction over patient care, creating regional monopolies that generate billions annually through facility fees, price arbitrage, and market manipulation. Since 1990, 1,573 documented hospital mergers have fundamentally altered competitive dynamics while demonstrating how asset accumulation and financial engineering extract wealth from communities that funded these institutions through tax exemptions and public subsidies.

The Merger Tsunami: 1,573 Deals, Unlimited Extraction

Hospital consolidation accelerated following healthcare deregulation, with mergers doubling from 12 annually in the mid-1980s to 24 per year by the early 1990s—establishing the template for systematic market concentration that continues today [15]. Between 1998 and 2017, healthcare systems completed 1,573 hospital mergers that reshaped metropolitan markets nationwide, while 428 additional mergers occurred between 2018-2023, including 72 transactions in 2024 alone [16].

The pace reveals coordinated industry strategy rather than organic market evolution. Consolidation reached critical mass by 2016, when 90% of metropolitan statistical areas qualified as highly concentrated hospital markets. This concentration increased further between 2017-2021, with highly concentrated metro areas rising from 71% to 77% despite existing monopolistic conditions [17]. Hospital systems deliberately pursued market dominance to enable extraction opportunities impossible under competitive conditions.

Market concentration enables systematic price extraction through reduced competition and enhanced insurer bargaining power. The share of community hospitals operating within larger health systems increased from 53% in 2005 to 68% in 2022, representing wholesale transformation of hospital ownership from community-controlled institutions to corporate profit centers [18]. This ownership shift fundamentally altered hospitals' mission from community service to shareholder returns, with predictable consequences for pricing and access.

HCA Healthcare: Private Equity's Extraction Template

HCA Healthcare exemplifies the private equity approach to hospital extraction, demonstrating how leveraged buyouts and financial engineering transform healthcare delivery into profit maximization engines. The company's 2006 leveraged buyout—valued at $33.2 billion with only $21 billion in cash—established the template for extraction-focused hospital ownership that prioritizes debt service over patient care [19].

The transaction structure revealed systematic extraction planning from day one. A consortium led by KKR, Bain Capital, and Merrill Lynch Private Equity acquired HCA through massive leverage, with Frist family members contributing $1.12 billion and Cerberus providing $246 million representing just 4% equity stake. The remaining 96% of the transaction was financed through debt assumption and new borrowing, immediately saddling the hospital chain with enormous interest obligations that drove all subsequent operational decisions [20].

Financial engineering results became apparent within three years as HCA systematically reduced expenses and staffing relative to competitors while achieving substantially higher cash-flow margins through market manipulation. The company decreased capital investment significantly from 2006-2009, deferring infrastructure maintenance and equipment upgrades to service debt obligations rather than maintain clinical quality. These decisions generated short-term cash flow for debt service while degrading long-term hospital capacity and patient care quality [21].

Current HCA performance demonstrates the long-term extraction model's success from a shareholder perspective. The company reported $70.6 billion in revenue for 2024 with 8.2% profit margins while announcing a massive $10 billion share buyback program [22]. This buyback—representing one-seventh of annual revenue—demonstrates how patient care dollars flow directly to shareholders rather than reinvestment in healthcare delivery capacity, medical equipment, or community health improvement.

HCA's Senate Pipeline: The Frist Family Connection

HCA's political connections represent one of the most direct pipelines between healthcare extraction and legislative power. The company was co-founded in 1968 by Dr. Thomas Frist Sr. and his son Thomas Frist Jr. The family's other son — Senator Bill Frist (R-TN) — served as U.S. Senate Majority Leader from 2003 to 2007. His tenure coincided with passage of the Medicare Modernization Act of 2003 (Medicare Part D), which prohibited government drug price negotiation — the single most valuable legislative gift to the healthcare industry in modern history. The Frist family fortune of approximately $1.8 billion is overwhelmingly derived from HCA stock, creating structural alignment between legislative influence and the company's financial interests. [193] In an unguarded moment, Senator Frist told the Boston Globe that conversations with his doctor father about the family calling were like "benign versions of the Godfather and Michael Corleone."

The human cost of HCA's financial engineering appears in systematic understaffing, delayed care, and community hospital closures that eliminate access for vulnerable populations. The company's focus on high-margin procedures and wealthy patient populations while avoiding charity care obligations reveals how private equity transforms healthcare from public service to wealth extraction mechanism.

The Non-Profit Shell Game: Tax Exemption for Executive Enrichment

Non-profit hospitals represent healthcare extraction's most sophisticated and cynical mechanism, combining federal tax exemptions worth billions annually with executive compensation and cash accumulation strategies that rival for-profit enterprises. Major non-profit health systems maintain CEO compensation exceeding $5-10 million annually while accumulating massive cash reserves and investment portfolios, generating returns while claiming financial distress to justify price increases and service cuts [23].

The community benefit accounting fraud enables systematic extraction under tax-exempt cover. Non-profit hospitals receive federal, state, and local tax exemptions theoretically in exchange for providing "community benefit" equal to exemption value. However, community benefit calculations include bad debt written off as "charity care," administrative costs of charity programs, medical education expenses often federally funded, and research costs—allowing systems to claim community benefits that far exceed actual charitable care delivery [24].

Cash reserve analysis exposes the profit accumulation disguised as financial necessity. Large non-profit health systems maintain billions in cash reserves and investment portfolios while simultaneously claiming financial constraints necessitating price increases, service cuts, and staff reductions. Cash-to-debt ratios at major non-profits often exceed for-profit competitors, proving that "non-profit" status functions primarily as tax optimization rather than commitment to affordable care [25].

Mayo Clinic exemplifies non-profit wealth accumulation while maintaining tax-exempt status. The system reported $17.6 billion in revenue and $2.3 billion in operating margin while maintaining massive cash reserves and paying CEO salaries exceeding $10 million annually [26]. These financial metrics match for-profit enterprises while benefiting from tax exemptions unavailable to explicitly profit-seeking businesses, demonstrating systematic gaming of non-profit regulations.

Real estate holdings create additional extraction vectors through sale-leaseback arrangements and related-party transactions. Non-profit hospitals accumulate valuable real estate through tax-exempt property acquisition, then engage in sale-leaseback deals with affiliated entities or REITs that extract value while creating long-term lease obligations burdening future operations. These transactions monetize tax-exempt asset accumulation while maintaining operational control [27].

Facility Fee Arbitrage: 87% Markup for Identical Services

Facility fee extraction represents hospital profiteering in its purest form, enabling 67-87% price increases for identical medical services based solely on ownership structure rather than care quality or resource utilization differences. Health Cost Institute analysis reveals systematic price arbitrage that extracts billions annually through billing manipulation rather than medical value creation [28].

Primary care visit pricing demonstrates the arbitrage opportunity with mathematical precision. A routine primary care office visit costs an average of $116 at independent physician practices versus $217 at hospital outpatient departments—an 87% price increase driven entirely by a $101 facility fee component added for identical services [29]. The facility fee represents pure extraction since no additional medical resources, equipment, or expertise justify the price differential.

Pediatric wellness visits demonstrate similar extraction patterns with $144 costs at independent practices versus $240 at hospital-owned locations, representing a 67% markup with a $96 facility fee for identical preventive care [30]. These price differentials exist despite identical examination procedures, equipment utilization, and clinical outcomes, proving extraction based purely on billing location rather than medical value.

Laboratory testing reveals even more extreme extraction ratios, with hospital outpatient labs charging 3.5 times more than independent facilities for identical tests using equivalent equipment and procedures [31]. This pricing manipulation generates substantial revenue from routine diagnostic testing while providing no superior accuracy, convenience, or medical value compared to independent laboratories.

The aggregate revenue impact demonstrates systematic profiteering scale. Health Cost Institute data shows facility fees generated $77 million in total spending for just primary care and pediatric wellness visits in 2022, with 24 of 43 analyzed states maintaining average facility fees above $100 [32]. When extrapolated across all hospital-owned outpatient services, facility fee extraction likely exceeds $10-15 billion annually in pure markup for identical medical services.

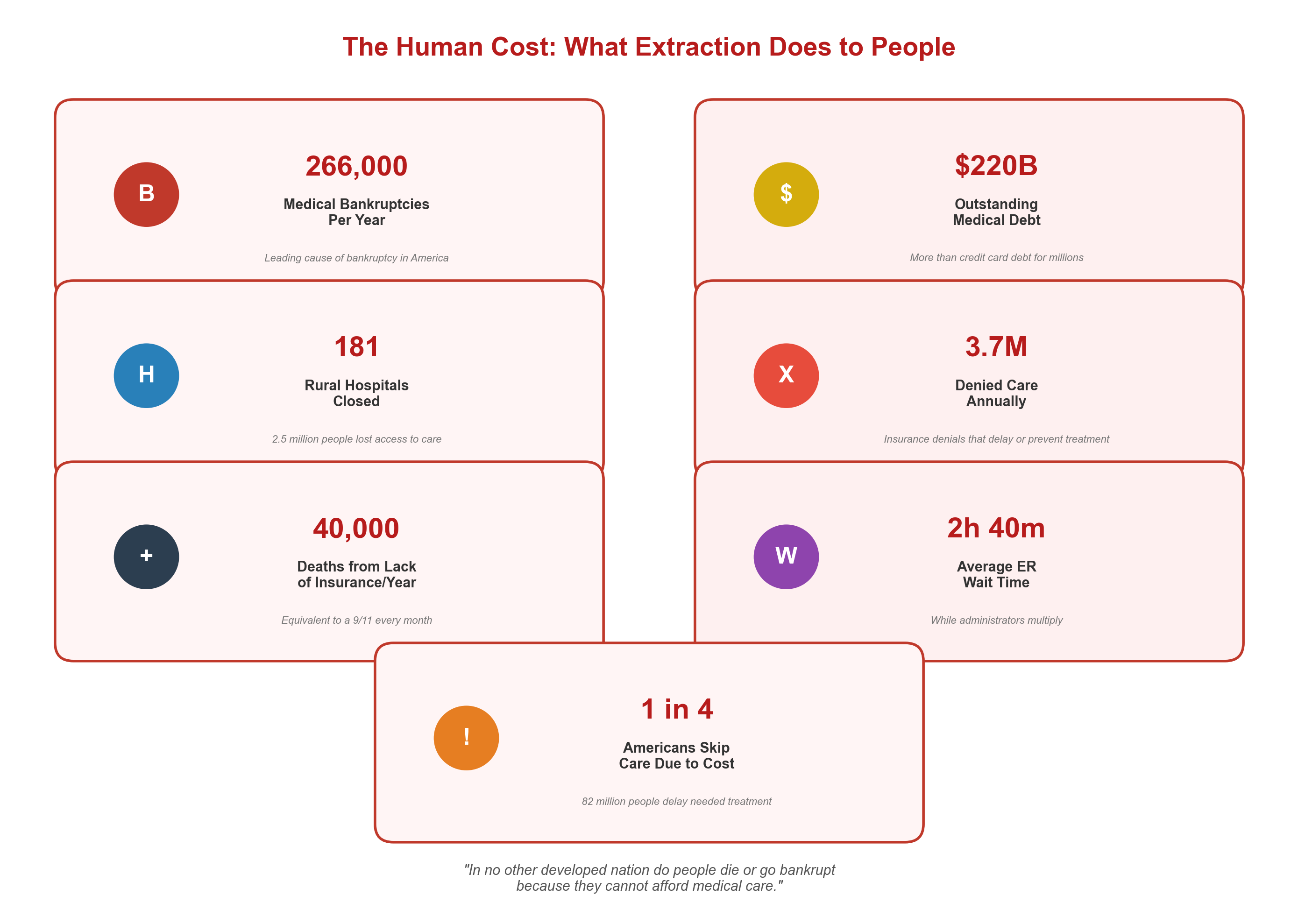

Rural Hospital Closures: 181 Hospitals, 2.5 Million Americans

Hospital consolidation's most devastating impact appears in rural communities where merger activity systematically eliminates healthcare access for entire regions. Rural hospitals' economics make them particularly vulnerable to acquisition by systems that prioritize profitable urban operations over community healthcare infrastructure, leading to systematic service elimination and facility closure [33].

Rural hospital closure statistics reveal consolidation's human cost with brutal clarity. Since 2010, 181 rural hospitals have closed permanently, eliminating hospital access for approximately 2.5 million Americans who must now travel 30+ miles for emergency care, obstetrics, and inpatient services [34]. Service line elimination often precedes full closure, with rural hospitals systematically cutting obstetrics, behavioral health, and emergency services that require staffing investment but generate lower margins than urban procedures.

The consolidation closure paradox demonstrates extraction priorities over community service. Research shows financially strong rural hospitals face higher closure risk after joining larger systems, indicating that acquisitions serve asset extraction rather than rural healthcare strengthening [35]. Systems acquire profitable rural facilities to extract value through real estate transactions, service line elimination, and cash flow redirection to urban operations rather than maintaining rural healthcare infrastructure.